Against the Current, No. 73, March/April 1998

-

The IMF's Imperial "Reform"

— The Editors -

Random Shots: The NASA Seniors Tour

— R.F. Kampfer -

"I Don't Want To Wait Twenty-six Years for Justice" Roisin McAliskey in Limbo

— Stuart Ross -

Political Prisoner Dita Sari

— Emily Citkowski -

The Jericho `98 March: Amnesty and Freedom for All Political Prisoners

— Steve Bloom - For International Women's Day

-

The Struggles of Women in Brazil

— Dianne Feeley interviews Tatau Gadinho -

Poverty & Oregon's Welfare Reform

— Johanna Brenner -

Activists Speak Out: The Poverty of Welfare Reform

— Interview with Theresa el-Amin -

Activists Speak Out: The Poverty of Welfare Reform

— Interview with Amy Hanauer -

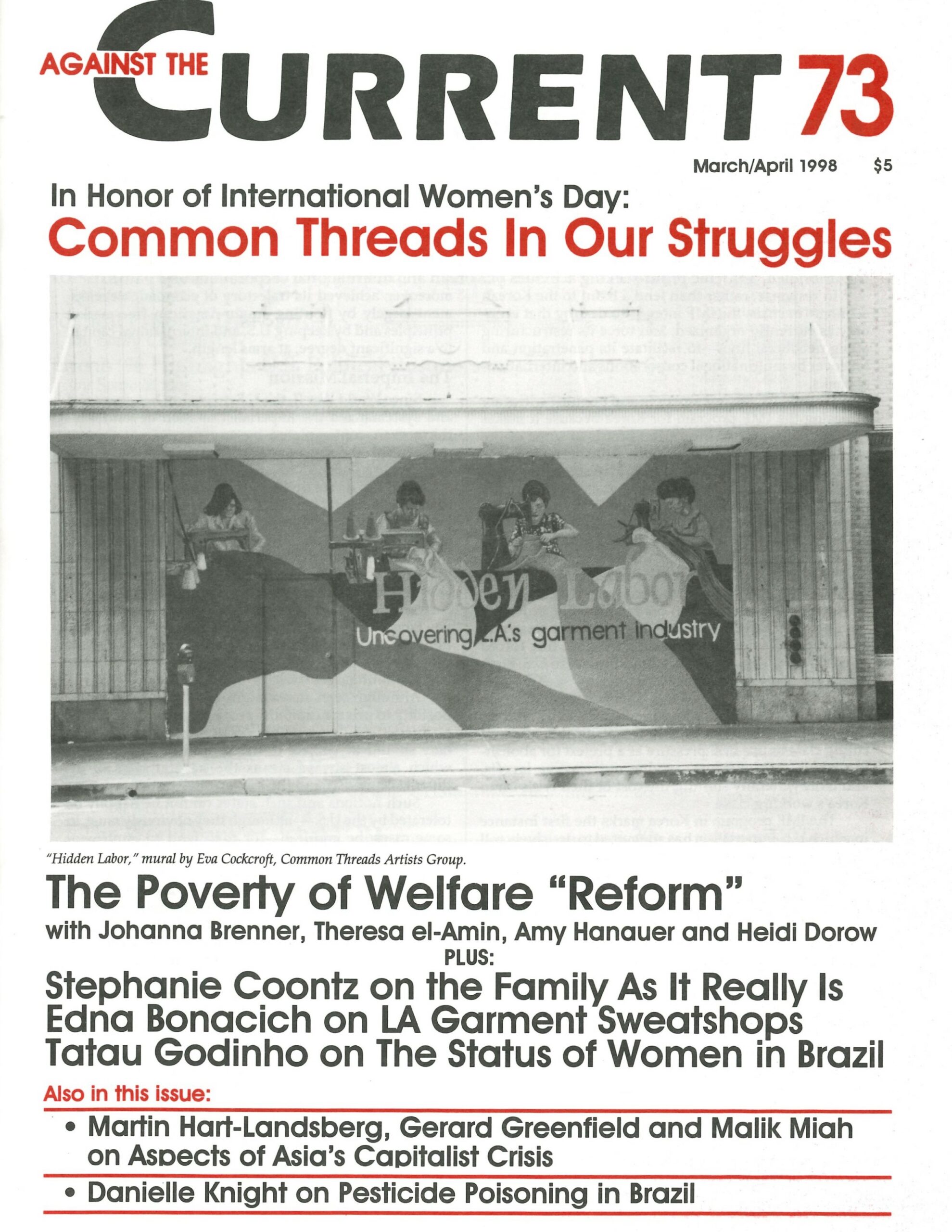

LA Sweatshops: Common Threads In Struggle

— Edna Bonacich -

Activists Speak Out: The Poverty of Welfare Reform

— interview with Heidi Dorow -

The Family As It Really Is

— Stephanie Coontz -

The Rebel Girl: We Shoot, We Score — At Last!

— Catherine Sameh - Asia's Capitalist Boom and Bust

-

Causes and Consequences: Inside The Asian Crisis

— Martin Hart-Landsberg -

Suharto's Days Are Numbered: Protests, Riots Rise as Clinton and IMF Back Dictator's Regime

— Malik Miah -

The World Bank's The State In A Changing World: The Global Politics of TQM

— Gerard Greenfield -

Transnational Capital and the State in China: Partners in Exploitation

— Gerard Greenfield - Reviews

-

The Destiny of A Revolution

— Donald Filtzer

Martin Hart-Landsberg

THE SO-CALLED ”MIRACLE economies” of Thailand, Malaysia, Indonesia and South Korea are in crisis. Their currencies and stock markets have lost between 30-50% of their value over the past seven months; many of their banks are insolvent; their central banks are hard pressed to come up with the foreign exchange needed to cover international debts.

Predictions for 1998 include a drastic slowing of growth and increase in unemployment and poverty.

What makes this crisis so important is that of these four economies, the three Southeast Asian countries (SEA-3) were promoted as models of successful capitalist development by both the International Monetary Fund and World Bank. On the other hand, officials and economists associated with these two institutions always were ambivalent about the economic success of South Korea, which had relied heavily on state direction of both domestic and international activity.

This strategy, of course, was in direct conflict with IMF and World Bank pronouncements on the benefits of free-market capitalism. Thailand, Malaysia and Indonesia, on the other hand, were less state directed and more open to international market forces, especially foreign direct investment (FDI), and thus closer to the IMF/World Bank conventional wisdom.

What is happening now, then, is more than the collapse of several Asian economies, it is the unraveling of a development model that these two major capitalist institutions had widely touted as demonstrating the virtues of export-led, free-market capitalism.

Despite having been a strong supporter of SEA-3 economic policies right up to the moment the crisis could no longer be denied, the IMF now puts itself forward as critic and savior, lecturing the SEA-3 and South Korea on the need for appropriate free-market policies and using the promise of much-needed foreign exchange to force their governments to accept these policies.

But IMF policies will solve nothing. They will, of course, ensure that foreign creditors get paid. But they will leave these economies far weaker and working people far worse off. To understand why this is true, we need to go beyond the headlines blaming current problems on ”crony capitalism” and ”corruption,” to examine the true roots of the crisis.

Origins of the Crisis

Times were bad for Thailand, Malaysia, and Indonesia in the first half of the 1980s. Like many Latin American and African countries, their natural resource-based exports were losing value and they were struggling to overcome serious debt crises.

Hoping to avoid default, the governments of Thailand and Indonesia agreed to implement IMF structural adjustment programs. These programs, designed to promote international capitalist interests, called for reducing the standard of living and power of workers as well as privatizing and deregulating economic activity in order to encourage exports, foreign direct investment (FDI), and a renewal of existing foreign loans.

The government of Malaysia sought to avoid IMF involvement by ”voluntarily” imposing its own structural adjustment program. However, in contrast to most Latin Americans and Africans, working people in the SEA-3 were saved from the pain of structural adjustment thanks to international developments involving Japan’s export-driven growth strategy and the United States.

In response to U.S. government demands that Japan reduce its large and growing trade surplus, the Japanese government in September 1985 agreed to revalue the Japanese yen relative to the dollar. The rise in the yen threatened the profitability of Japanese exporters who, aided by their government, launched a massive effort to relocate production overseas.

While a majority of Japanese FDI initially went to the United States and Europe, a considerable amount also went to Asia, in particular the SEA-3. From 1985-1990, these countries received a minimum of $15 billion of Japanese FDI. This investment, in turn, threatened South Korean and Taiwanese producers, causing them to follow with their own FDI in Southeast Asia.

This massive inflow of investment enabled Thailand, Malaysia, and Indonesia to (temporarily) overcome their economic problems and escape the IMF and its structural adjustment policies.

But the production of these exports was largely under foreign control. For example, in Malaysia at the end of the 1980s foreign-controlled companies accounted for approximately 99% of the exports of electronics, over 90% of the exports of machinery and electrical appliances, over 80% of the exports of rubber products, and 75% of the exports of textile and apparel.

It was largely Japanese producers that owned these companies; in 1992, the Japanese share of the total stock of manufacturing FDI was 73% in Malaysia and 68% in Thailand. By 1994, approximately 7% of all Thai production workers were employed by Japanese firms. The Matsushita electrical company alone accounted for some 4-5% of Malaysia’s GDP.

From the perspective of the United States—the destination of a majority of SEA-3 manufactured exports—these three countries appeared to be real success stories. After all, they were growing rapidly by selling internationally competitive products. But while this growth did produce lower poverty rates and a growing middle class, it came at high cost for the great majority of SEA-3 working people.

The most important reason was that the SEA-3 were involved in a process of dependent industrialization. As a result, although each ran surpluses in their trade with the United States, each ran far bigger deficits in their trade with Japan.

In 1992, for example, Thailand ran a $2.9 billion trade surplus with the United States and a $8.3 billion trade deficit with Japan. Malaysia ran a $4.2 billion trade surplus with the U.S. and a $5.8 billion trade deficit with Japan. And the faster these countries grew, the larger were their overall trade deficits.

Malaysia’s current account deficit as a percent of GDP grew from 4.8% in 1993 to 8.5% in 1995. Thailand’s grew from 5.9% to 8.1% over the same time period. By comparison, the U.S. figure was only around 2%.

Faced with major trade deficits, SEA-3 governments remained under constant pressure to generate more foreign exchange; failure meant the collapse of their economies. Thus, they smashed worker attempts at unionization, brought in migrant workers to keep wages low, and continued the high speed exploitation of natural resources.

As one indicator of the insanity and brutality of this race for foreign exchange, the Thai government aggressively promoted a sex industry to earn foreign exchange, saddling the country with a major AIDS crisis.

Most of the gains generated by the workings of these “miracle economies” went to political and corporate elites. For example, by 1994, according to the Thailand Development Research Institute, Thailand had joined the ranks of the top five countries in the world in terms of wealth inequality.

The SEA-3 countries succeeded in covering their growing trade deficits from 1986-1990 in large part because each year brought with it new Japanese FDI. But, beginning in the early 1990s, Japanese FDI in Thailand and Malaysia began to decline. In the case of Thailand, this investment fell from $2.4 billion in 1990 to $578 million in 1993.

It was not that Japan was giving up on Asia. Rather, Japanese corporations were shifting their focus to China and Vietnam, countries with even lower wages and bigger domestic markets. In fact, beginning in 1994, Asia passed Europe to become the second largest destination for Japanese FDI.

That year, Japanese FDI was $17.8 billion in the United States, $9.7 billion in Asia, and $6.2 billion in Europe. Even more impressive is the fact that Japanese manufacturing FDI in Asia surpassed that in the U.S. In 1994, Japanese manufacturing FDI was $5.2 billion in Asia, compared with $4.8 billion in the U.S.

Left short of foreign exchange as a result of this shift in Japanese priorities, the Thai and Malaysian governments aggressively pursued other sources of foreign exchange. Their timing was good: Recession and low interest rates in the developed capitalist world generated substantial interest on the part of investment houses and international banks in the “emerging” markets of Southeast Asia.

Leaving nothing to chance, Thailand and Malaysia (as well as Indonesia and the Philippines) courted these investors by dropping their foreign exchange controls, opening their stock and bond markets to foreign investors, pegging their currencies to the dollar, raising interest rates, and creating new opportunities for foreign banks to make dollar denominated loans to local businesses. Thailand offers a good illustration of the results: Net portfolio investment (involving the purchase of Thai stocks and bonds, especially by U.S. mutual and pension funds) rose from an average of only $646 million in the period 1985-89 to $5.5 billion in 1993 and even higher in the following years.

Considerably more money was raised through the Bangkok International Banking Facility, established in 1993, which enabled Thai finance companies and banks to borrow approximately $50 billion over a three year period from foreign (primarily Japanese) banks in Bangkok. Thus the rapid growth rates of the past were sustained, but at a cost, as the country’s foreign debt soared from $21 billion in 1989 to $89 billion in 1996.

It is worth emphasizing that the IMF and World Bank had no complaints about these developments (which also encouraged and rewarded cronyism and corruption); they confidently concluded that as long as the financial transactions were being made by private as opposed to public agents, market forces would ensure the appropriate level of debt and efficient use of funds

The borrowed money did not go into productive investments. Thai finance companies and banks relent a large percentage of the money to property developers. By late 1995, as might be expected given the unbalanced nature of wealth in Thailand, there was a glut of both commercial and residential units.

By the beginning of 1997 almost half of all loans made to property developers were non-performing. Thai finance companies and banks began to default on their foreign loans. Although not as far advanced, a similar process with similar results was underway in Malaysia, Indonesia, and the Philippines.

Foreign investors now wanted out of Thailand. Adding to their concern was growing uncertainty over whether the Thai central bank had sufficient dollars to cover investor withdrawals at the pegged exchange rate. This concern was fueled by the fact that Thailand’s export offensive was losing steam; its export growth rate fell from 26% in 1995 to less than 1% in 1996.

As foreign investors raced to unload their stocks and bonds (driving down the respective markets) and call in their dollar loans, it became clear that central bank reserves would not be up to the task. Speculators soon joined in the run on the Thai currency, the baht. The government jacked up interest rates and ran through its reserves, but it could not slow the rush for dollars.

Finally, on July 2, 1997, the Thai government abandoned its pegged exchange rate; the baht fell by 18% on that day alone. That fall, in turn, stimulated more selling and speculation, pushing domestic stock and bond markets and the baht down further.

As Thailand was being tested, investors and speculators turned their attention to other countries in the region. Indonesia, Malaysia, and the Philippines had also engaged in substantial foreign borrowing, recorded large and growing current account deficits, established dollar-linked exchange rates and allowed their finance companies and banks to commit a high percentage of loans to glutted property markets.

Not surprisingly, investors and speculators began pulling money out of these countries as well. Stock and bond markets fell and before July was over the Filipino peso, the Malaysian ringgit, and the Indonesian rupiah were all headed downward.

In order to avert a complete economic meltdown, Thailand (in August) and Indonesia (in October) were forced to ask the IMF for assistance and, in return, accept an IMF structural adjustment program. Malaysia, as it had done before, designed its own structural adjustment program.

South Korea’s crisis has a somewhat different history, though events in Southeast Asia appear to have triggered it. In contrast to the SEA-3, South Korea went through an extended period of domestic industrialization, with FDI playing a limited although important role.

This was a forced march, directed by military dictatorship, but it did raise living standards. This achievement was in large part the result of a growth strategy built on state direction of economic activity; repression of labor; Japanese willingness to sell technology, components, and machinery to South Korea’s large conglomerates (chaebol); and U.S. willingness to provide political and financial support and a market for South Korean exports.

This growth strategy began to unravel beginning in the late 1980s—as a result of the country’s export success. South Korea ran its very first and only trade surpluses during the years 1986-1989. This export success threatened Japanese producers, leading them to begin withholding key inputs from the South Korean chaebol.

The surpluses also provoked the U.S. government to demand that South Korea revalue its currency and open its markets to U.S. goods and firms. South Korean trade gains also gave the chaebol added independence from a weakening state, allowing them to use their profits for speculative rather than productive investments. Finally, this period of economic “success” provided the context for a massive explosion of labor activity, resulting in large wage increases.

This combination of factors quickly began to undermine South Korea’s export drive. The situation was made worse by the growth in export competition from Japanese firms located in the SEA-3. South Korea’s 1996 current account deficit grew to a record $23.7 billion, almost triple the deficit of the previous year. That same year profits of the top thirty chaebol fell by 90%.

The state tried to boost chaebol competitiveness and profits by attacking labor, but failed as workers responded with a general strike in 1996-97. Several of the country’s largest chaebol were finally forced into bankruptcy in 1997, thereby raising questions about the stability of other chaebol and the South Korean banking system.

South Korea had accumulated a foreign debt of over $110 billion dollars, with approximately $70 billion due for repayment in less than a year. As the financial crisis swept through Southeast Asia, foreign investors became increasingly concerned about the credit worthiness of South Korean firms and banks and the adequacy of the central bank’s shrinking foreign exchange holdings.

They began selling stocks and calling in loans; by mid-November, the won (South Korean currency) was in free fall and South Korea was facing a major foreign debt crisis. The South Korean government reluctantly agreed to accept an IMF program in early December.

Lessons of the Crisis

Malaysian Prime Minister Mahathir quickly blamed the crisis on western speculators and called for tougher capital controls. There can be no doubt that speculators played a role in driving down currency rates and that capital controls are useful. But Mahathir’s claim missed the mark, as the above history makes clear.

The roots of the crisis are to be found in the very workings of Asia’s growth strategy. For example, Southeast Asian governments decided, on their own, to drop financial controls and open up financial markets because they needed funds in order to cover widening current account deficits. And these deficits were caused, in large part, by the dependent nature of their export industries (as well as the consumption desires of the wealthy).

These trade problems were intensified by the fact that growing numbers of Asian countries were trying to export the same basic products, including petrochemicals, consumer appliances, passenger cars, and computer chips.

This competition led to currency devaluations by China in 1994 and Japan in 1995, which placed the SEA-3 and South Korea at a disadvantage. Even more importantly, it led to regional overproduction which, in 1996, produced falling export prices and steep declines in export growth rates for Thailand, Malaysia, the Philippines, and South Korea.

In short, the reality is that the export-driven growth strategy of the past can no longer deliver sustainable national growth, with or without capital controls.

As previously noted, the IMF blames the Asian crisis on cronyism and corruption, arguing that free markets and independent public regulatory agencies would have prevented banks from recklessly funneling money to well connected but poorly managed businesses for ill-conceived property developments and investments.

While such cronyism/corruption is a serious problem, the above history makes clear that the crisis was more the immediate result of government-initiated financial and industrial deregulation (which in turn encouraged cronyism/corruption), and that its origins were in Asian structures of production rather than finance.

Even more importantly, IMF structural adjustment policies will do nothing to advance Asian economic development. Asian governments found themselves without enough foreign exchange to enable their corporations and banks to pay foreign creditors.

Seeking to help Asian elites avoid default, the IMF offered an immediate infusion of foreign exchange. In exchange for these funds and the promise of more to come, the governments of Thailand, Indonesia, and South Korea each agreed to an IMF structural adjustment program—designed to ensure that the targeted countries will open themselves more fully to international business as well as give priority to earning the foreign exchange necessary to pay international debts.

Supposedly, acceptance of such a program will encourage international lenders to extend new credits, thereby enabling existing regimes to avoid a prolonged recession/depression and social chaos.

The basic IMF structural adjustment program for Thailand, Indonesia, and South Korea requires their governments to maintain high interest rates in order to attract funds and thus defend currencies; cut spending and growth in order to reduce incomes and thus imports; gut social programs and weaken labor rights and unions in order to lower labor costs and thus promote exports; and privatize, reduce tariffs, and end restrictions on foreign ownership of financial and non-financial businesses in order to attract foreign investment.

As we have seen, the current crisis is the outcome of a foreign-dependent, export strategy. But rather than promote a fundamentally different economic strategy, this IMF program will only make these countries more dependent on exports and foreign corporations than they currently are, and in the process lower wages and undermine working and living conditions for the majority of their citizens.

As a result, this “solution” will also further intensify trade imbalances throughout the world, encouraging reactions that are bound to lead the global economy closer to a crisis of overproduction.

History shows that IMF “neoliberalism” does not work, except in the narrowest sense of defending capitalist interests, and progressives are right to resist it as an answer to Asian problems. However, in their desire to demonstrate the failure of neoliberalism and build resistance to it, progressives all too often end up embracing existing Asian regimes and calling for a strengthening of their state-directed, export-driven growth models.

Unfortunately, this political strategy leads to a dead-end. Although the experience of South Korea does demonstrate that there is an alternative to the free market, that state regulation of economic activity can be effective, Asian state capitalism contained its own contradictions. And even during its period of rapid growth, working people suffered greatly.

In short, it is time for bold thinking about the institutional and structural changes necessary to create a more democratic and domestically centered economy, responsive to popular needs and connected to other economies through negotiated trade agreements.

There can be no question that working people in Asia face hard times. As a result of Japanese capital’s regionalization strategy, workers in Japan are suffering from rising levels of unemployment and downward trends in wages and working conditions. Workers in Thailand, Malaysia, and Indonesia confront rapid increases in unemployment and poverty rates as a result of their incorporation into a regional accumulation model shaped by this Japanese investment.

Workers in South Korea face a similar situation as a result of the dependent nature of their own country’s growth strategy and the pressures imposed by regionalization.

National struggles are slowly taking shape against the crisis and the IMF-led strategy to make working people pay its costs, most forcefully in South Korea. Moreover, the basis for building meaningful regional solidarity also exists.

Therefore, now is not the time to lose confidence in the existence of alternatives to, or in our ability to collectively create something far better than, capitalism. We must push our own thinking beyond state-capitalism and export-driven growth strategies by encouraging, supporting, and learning from the debates and struggles currently taking place in Asia.

Notes

- For a more complete discussion of the causes and consequences of the Japanese-led regionalization process see Martin Hart-Landsberg and Paul Burkett, “Contradictions of Capitalist Industrialization in East Asia: A Critique of `Flying Geese’ Theories of Development,” Economic Geography, forthcoming, 1998.

- Mitchell Bernard and John Ravenhill, “Beyond Product Cycles and Flying Geese: Regionalization, Hierarchy, and the Industrialization of East Asia,” World Politics, Vol.47, No.2, January 1995: 196.

- Chai Siow Yue, “Foreign Direct Investment in ASEAN Economies,” Asian Development Review, Vol. 11, No.1, 1993: 84. Walter Hatch and Kozo Yamamura, Asia in Japan’s Embrace (Cambridge, UK: Cambridge University Press, 1996), 11.

- Satya Sivaraman, “Thailand-Economy: A Tiger Losing Its Stripes,” InterPress Service, Worldwide distribution via the APC networks, August 12, 1997.

- Edith Terry, “An East Asian Paradigm?” Atlantic Economic Journal, Vol.24, No.3, September 1996: 189-90.

- A more complete analysis of developments in Thailand can be found in Walden Bello, “Addicted to Capital: The Ten Year High and Present Day Withdrawal Trauma of Southeast Asia’s Economies,” Focus-On-Trade (a publication of Focus on the Global South, Bangkok, Thailand), No.20, November 1997.

- For a discussion of the forces shaping, and contradictions generated by, the South Korean growth strategy see Martin Hart-Landsberg, Rush to Development: Economic Change and Political Struggle in South Korea (N.Y.: Monthly Review Press, 1993).

- Darren McDermott and Michael Schuman, “South Korea Economy Feels the Pressure,” Wall Street Journal, November 3, 1997, A18.

ATC 73, March-April 1998