Against the Current, No. 108, January/February 2004

-

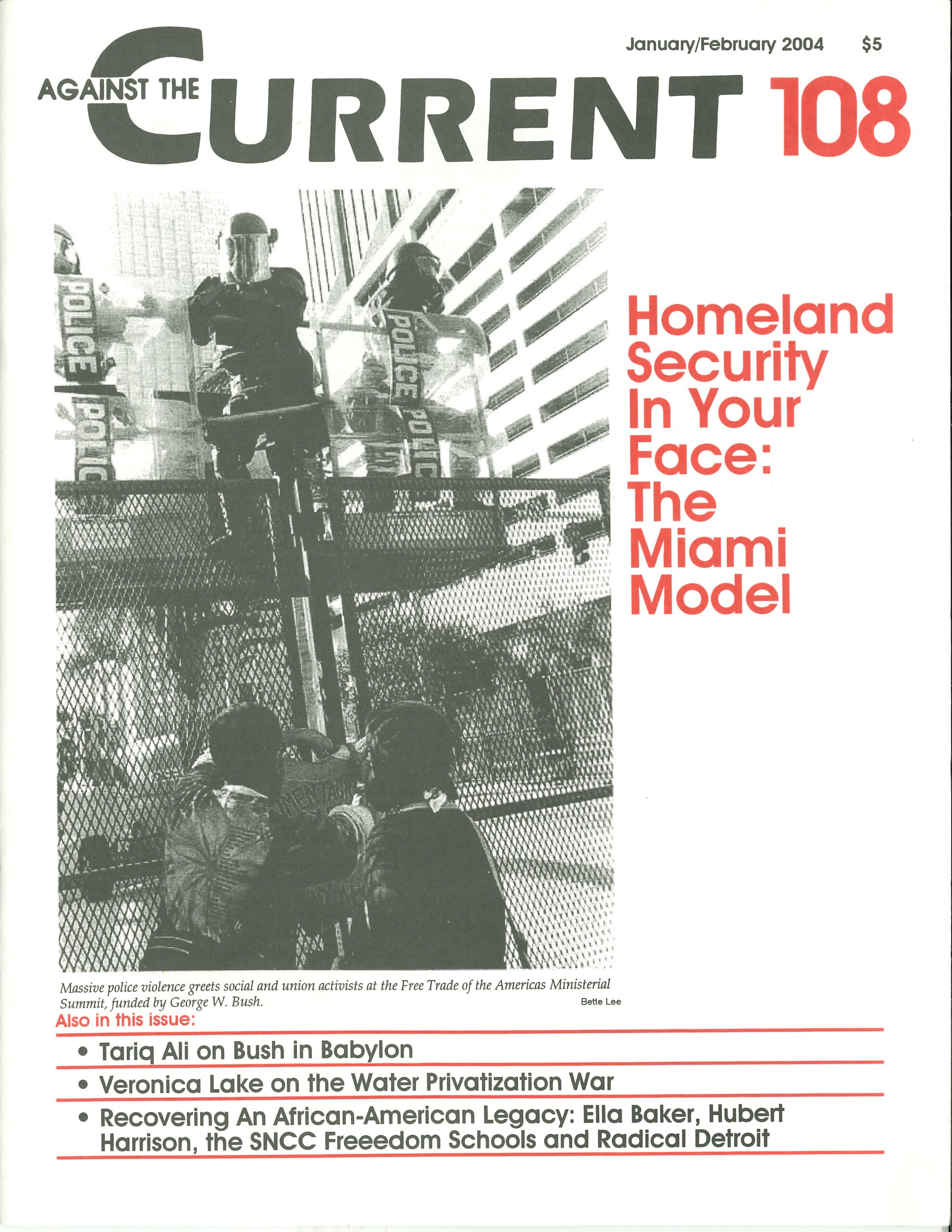

The Miami Model in Your Face

— The Editors -

Black Voters in 2004

— Malik Miah -

Looking at Bush in Babylon

— interview with Tariq Ali -

Eyewitness Chile: After 30 Years

— James Cockcroft -

Iran on the Verge of Revolution?

— Hassan Varash & Hamid Naderi -

Privatizing Water, The New World War

— Veronica Lake -

Matt Gonzalez & San Francisco's Green Earthquake

— Rich Lesnik -

What's Behind the Economic Upturn?

— Loren Goldner -

Amer Jubran: From Exile to Exile

— David Finkel -

On the History of Human Nature

— Jim Morgan -

Random Shots: What Do You Worship?

— R.F. Kampfer - Labor's Battles

-

Unions Confront A Restructured Industry

— Joel Jordan -

University of Minnesota: Dignity vs. Cutbacks

— Corey Mattison -

How Strikers Educated Miami University

— Dan La Botz -

The UAW Contract's Downhill Spiral

— Ron Lare & Judy Wraight - African-American History in Retrospective

-

Sampling New Black Radical Scholarship

— Alan Wald -

The Freedom Schools, An Informal History

— Staughton Lynd -

Whose Detroit? A City's Upheaval

— Nicola Pizzolato -

The Vital Legacy of Hubert Harrison

— Allen Ruff - Reviews

-

Eva Kollisch's Girl in Movement

— Lillian Pollak - In Memoriam

-

Sam Phillips & Sun Records

— George Fish -

Jack Barisonzi, 1933-2003

— Patrick M. Quinn

Loren Goldner

THE DEPARTMENT OF Commerce announced on October 30 that the U.S. economy had grown at a 7.2% annual rate in the third quarter of 2003. Since these statistics are constantly being revised, one wonders what they really mean. (Recall that the “productivity miracle” of the second half of the 1990’s almost disappeared in retrospective downward revisions after the March 2000 dot.com crash).

Whatever the case, it is clear that the Bush administration is pulling all stops in its re-election strategy for 2004. One does not have to believe in a “political business cycle” to recognize that the U.S. government has sufficient tools to pump up the economy going into an election year.

Most notorious in the history of this stratagem was Nixon’s 1971-1972 reflation based on wage-price controls, the “reform” of the Bretton Woods system (amounting to a 32% surcharge on foreign imports and, for that period, massive deficit spending) to assure his 1972 re-election. Afterward, inflation took off, the Bretton Woods system collapsed, and the U.S. and world economy plunged into the deepest downturn to date (1973-1975) since the 1930s.

Of course Nixon — like Bush today — was dealing with long-term trends that pointed far beyond his election strategy; but the aim of the “political business cycle” is to have the shit hit the fan immediately after the election, allowing maximum political flexibility to “Do Something” after consolidating political power.

The Crash and Disappearing Jobs

What is indisputable is that there was a three-year (2000-2003) “bear market” in the U.S. and world stock markets in which trillions of dollars of paper value disappeared, and a “mild recession” which, again, appears mild based on dubious statistics that are constantly being manipulated for political ends.

The official unemployment rate of 6% during the 2001-2003 period does not include the 1% of the U.S. population in prison, nor the people who have entirely dropped out of the labor market, nor people who are working part-time (as little as a few hours per week) who would like to work full-time.

With these parts of the population included, the real rate of unemployment has been estimated at roughly 11%. In reality, 2.7 million jobs have disappeared in the U.S. economy since 2000, and there has been little upturn so far in employment figures.

It is equally clear that from January 2001 onward, Greenspan and the Federal Reserve were looking at the possibility of a full-blown deflationary crash, following the end of the high-tech boom (in which it was discovered, for example, that 98% of the fiber-optic cable laid in the preceding years would never be used).

The Federal funds rate (the rate at which the Fed lends to banks) came down in lockstep fashion, from six to one percent by June 2003. To this must be added the Bush tax cut for the rich (approximately $200 billion per year) and the rapid increase in the Federal deficit (estimated at $375 billion for 2003) from the balanced budget achieved (with some creative accounting) in the last years of Clinton (it is somewhat hilarious to see the Democrats now attacking the Republicans for large-scale deficit spending).

Finally, the post-2002 decline of the dollar (30% against the euro, 10% against the yen) is aimed at making U.S. goods cheaper overseas, which so far has not begun to curb the $500 billion annual U.S. balance-of-payments deficit, but which should in short order result in inflation in the United States by increasing the cost of imported goods.

In the meantime, the U.S. Treasury must borrow $1.5 billion per day to cover this deficit, and is currently taking 40% of world savings. The minimum estimate of $2 trillion of foreign indebtedness ($10 trillion held by foreigners offset by $8 trillion of U.S. assets abroad) means that total U.S. foreign debt is already 20% of GDP, a level typical of a Third World country. Already one percent of U.S. GDP is going to pay off the interest on foreign-held debt.

Debt and Speedup

The current wave of euphoria that the 2000-2003 bear market is over is based on these (and other) paper indicators of an expansion that has not yet altered any of the fundamental crisis trends of earlier years, but is rather based on all the expansion of liquidity mentioned above.

For all the late 1990s hype about the “New Economy” and the high-tech “revolution,” it seems that the health of the U.S. economy still depends on the willingness and ability of Americans to buy houses and cars on credit, exactly like forty years ago.

Third-quarter U.S. corporate profits generally “look good,” but (as “Austrian school” commentators such as Richebacher have pointed out) are generally based on the success of layoffs and downsizing by U.S. corporations, not to mention “pro forma” accounting methods whose efficacy was (once again) revealed in the wake of the March 2000 crash, and the subsequent corporate scandals and collapse of the Arthur Anderson accounting firm.

Further, these profits reflect an intensive speedup of those workers who have managed to hang onto their jobs.

The basic strategy of loosening credit has succeeded in driving the debt of U.S. “consumers” to all-time highs, starting with the ingenious mechanism of mortgage refinancing, putting hundreds of billions of dollars of spending power into the hands of the middle class, based on the ongoing (but currently topping out) nationwide housing bubble.

This bubble, like the dollar bubble, will follow the earlier high-tech bubble into collapse, leaving millions of people with bloated mortgages to pay off.

The hope of Greenspan and Bush was that greater consumer spending would keep the economy alive until corporate spending on capital plant kicked in, the classic pattern of previous emergence from recession since World War II.

However, with U.S. firms operating at 75% of capacity and still working their way out of the indebtedness of the boom years, this capital spending surge has not emerged, not to mention any significant upturn in hiring of workers.

One of the best indicators of a lack of capitalist confidence in the current upturn is the rapid rise of some basic commodity prices (another parallel to the 1971-73 reflation), led by gold, which has increased by 20% in 2003.

The China and Dollar Factor

It is now essential to turn to the international dimensions of the U.S. “recovery,” which are still on the margins of mainstream perception in the U.S. itself. Fifteen years ago, the main imbalance in the international economy appeared to be between the U.S. and Japan: Japanese goods were conquering the U.S. domestic market, and U.S. dollars were accumulating in the Bank of Japan.

Today, the focus is increasingly on the imbalance between the United States and China, as the latter is remaking the international division of labor.

The basic “engine of prosperity” for years has been Asian exports to the United States in exchange for dollar reserves. It is estimated that China, Japan, Taiwan and South Korea alone hold over $1 trillion, and most of that money is recycled into U.S. capital markets (such as U.S. government debt) to make possible even greater credit expansion, and thus consumption, in the United States itself.

Like Europe in the 1950s and 1960s, the Asian industrial powers are allowing the United States to finance its deficits with its own IOUs. Similar trends, though not on the same scale, are still visible today with European and OPEC holders of dollars.

This centrality of the dollar in the world economy is the main enigma to be unraveled to clear the way for understanding future possibilities for accumulation. The dollar has been in “crisis” since around 1958, as the Bretton Woods system began to come unstuck, and it has survived the collapse of that system (1971-73) and three decades of an outright “dollar standard” (in contrast to the former “gold-exchange” standard of 1944-1971).

During this period, U.S. industry has been down-sized, outsourced and hollowed out. With the emergence of China, even maquiladora plants on the U.S.-Mexican border are relocating to Shenzhen.

The Deficit Economy

Foreigners have been subsidizing U.S. deficits for 45 years as the price for access to the huge U.S. domestic market. Counter-trends to an abrupt decline of the dollar to date include foreign direct investment in the United States (in part to circumvent the possible protectionist backlash advocated by some sectors of U.S. industry as well as some sectors of organized labor), and the repatriation of profits from the still-considerable U.S. assets abroad.

But no amount of qualifying the extent of U.S. economic decline since the 1950s can conceal the increasingly fictitious character of the U.S. economy as a whole, propped up by foreigners as “too big to fail.”

One indicator shows this trend better than any other: that of “Tobin’s Q,” the bourgeois concept expressed in the ratio of current value of total capital assets to their cost of replacement today. One study shows this ratio fluctuating around one for the entire 20th century up to 1995, with obvious deviations below one (the depressed, deflationary 1930s) and above one (the inflationary boom years of the 1960s and 1970s).

From 1995 to 2002, Tobin’s Q for U.S. capital assets increased to the staggering level of 2.11. The credit making possible this hugely inflated value of capital assets was largely extended by foreigners.

Such an increase is contemporary with the similar rise of the dollar in the same years, following the cheap dollar of 1985-1995. Foreign investment in dollar assets after 1995 was a “virtuous circle” in which considerable profits (e.g. the stock market mania) were supplemented by a steady rise in the dollar itself.

Beginning in 2000, the virtuous circle turned into a vicious circle, with collapsing stock values interacting with a declining dollar, so that a foreign investor was losing at both ends. By 2002, foreign direct investment in the U.S. had turned negative, and the head of the European Central Bank Wim Duisenberg wondered out loud if the “inevitable” decline of the dollar would be a gradual retreat or a global panic.

The Politics of Crisis

But this is as far as “economics” alone will take us, and it is essential to look at the “politics” in the critique of political economy to understand to what extent the United States will succeed in making the rest of the world pay for its decline and crisis. Success or failure here will in part determine the length of the current U.S. “job-loss” recovery.

The fundamental problem for U.S. capitalism is to globally circulate the mass of fictitious capital* (most immediately embodied in that $2 trillion external debt) that has built up over 45 years of subsidized dollar hegemony, making possible that capital’s valorization by extracting an adequate amount of surplus value. (We are not even considering here the unknown trillions tied up in the global derivative markets and hedge funds.)

This is the key to U.S. foreign policy, which is aimed at breaking down all remaining barriers to such extraction of profit:

* It has accomplished this through the neoliberal policies of the International Monetary Fund and World Bank, bleeding dry four billion people in eighty Third World countries.

* It has accomplished this by the opening of the former Soviet bloc and its vast natural resources to unprecedented looting, provoking (in the Russian case alone) the biggest peacetime demographic contraction in modern history.

* It has accomplished this by the opening of China, whose economy, after twenty years of 8-10% annual growth, is now in danger of “overheating” from its absorption of so many surplus dollars.

* It has accomplished this through NAFTA, the free trade zone with Canada and Mexico, and now intends to extend this zone to all of Latin America.

U.S. policy is now knocking at the doors of the remaining trade blocs, Europe and the Asian industrial powers, which present some obstacle to the kind of neoliberal looting of assets through “shareholder value” which in the United States itself produced the meltdown of the post-2000 period.

The United States gained important advantage through the Asian crisis of 1997-1998, forcing open South Korea and other countries for “reform.” (Current studies estimate that 3.3 million U.S. service jobs will migrate to India by 2015, making that country, along with China, a further source of loot.)

It has also gained a strong foothold throughout Eurasia, with troops from Georgia to Uzbekistan (and Poland and Rumania agreeing to U.S. bases) with a policy aimed at keeping Europe, Russia, India, China and Japan off-balance and thus amenable to the needs of the world’s “sole remaining superpower.”

Unless and until the European Union can develop political and military power to match its economic size, the biggest obstacle to this U.S. strategy of making the rest of the world subsidize its decline is Asia, and ultimately China.

Ever since the 1997-98 crisis, the Asian powers have been taking tentative steps to build a trade bloc similar to the European Union and to NAFTA, which would ultimately imply a customs union, an Asian currency and something like an Asian Monetary Fund independent

of the IMF. (The Japanese have made proposals for the latter, only to be slapped down by the United States.)

It is obvious to everyone that the ultimate stakes in this strategy are the breaking of dependence on access to the U.S. market and from the ongoing accumulation of dollars in exchange for goods. Accordingly (as with Treasury Secretary Robert Rubin in during the Asian meltdown) the U.S. had ridiculed these attempts, just as it has repeatedly managed — through Britain, through NATO and most recently through the Afghan and Iraq wars — to hobble European unification.

Conflict at Home

This brief analysis up to now has said nothing about the other potential obstacle to U.S. capitalist crisis management: the American working class. This is in part because U.S. capital has been so successful, since 1973, in driving down living standards for 80% of the American population, with little open resistance.

One reflection of this success is the falloff in strike activity to almost zero. But it is just possible that this attack on the working class has gone about as far as it can go.

The huge losses sustained by the mutual funds of ordinary working people in the stock market meltdown; the accelerating disappearance of retirement for millions; the exploding cost of private health care; the endless corporate scandals of recent years (Enron, World.com, Tyco, etc.); the growing revulsion at CEO payouts by looted corporations (or the $139 million payout to Richard Grasso, former head of the New York Stock Exchange), all have eroded the right-wing populist base for neo-liberal austerity of the past thirty years.

The Los Angeles supermarket and transit strikes that began in October have witnessed a widespread popular sympathy and support not seen in years.

To restore the U.S. minimum wage ($6.50 per hour) to its purchasing power of thirty years ago would mean increasing it to $18 per hour: even a modest working-class offensive to regain the ground lost in the past three decades could mark the end of the dollar empire.

ATC 108, January-February 2004