Against the Current, No. 88, September/ October 2000

-

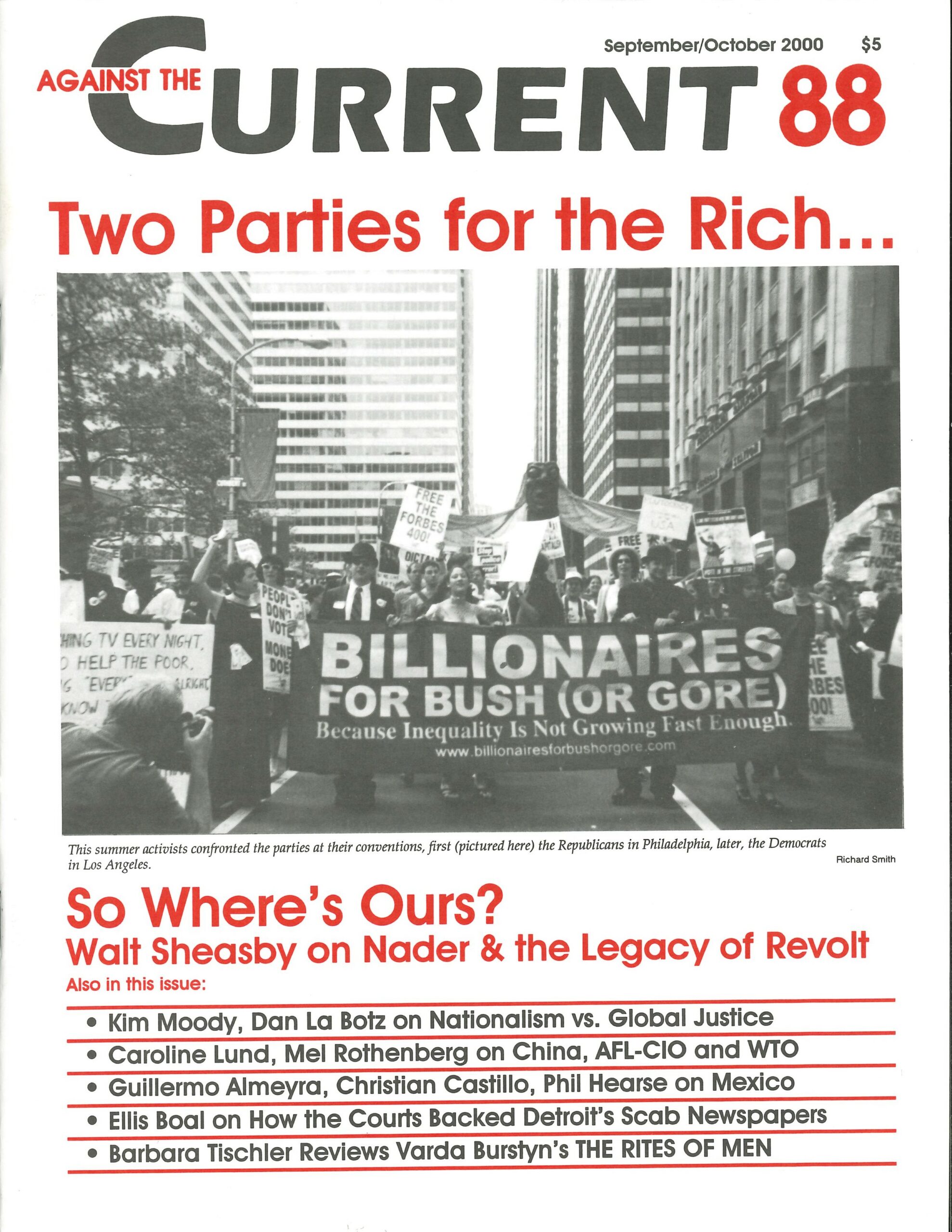

To the Spoilers the Victory?

— The Editors -

Race and Class: The Wealth Gap

— Malik Miah -

Courts Back Detroit Scab Papers

— Ellis Boal -

Why Detroit Needs Justice and CPR

— Charles Simmons -

IPPN Standing Strong in the Storm

— José Manuel Sentmanat -

Ralph Nader and the Legacy of Revolt

— Walt Contreras Sheasby -

Global Capital and Economic Nationalism (Part 2)

— Kim Moody -

The New Movement for Global Justice

— Dan La Botz -

Viewpoint: Transnationals After Seattle

— Loren Goldner -

Rebel Girl: Feminism vs. the Evil Lessers

— Catherine Sameh -

Random Shots: People and Other Animals

— R.F. Kampfer - Mexico's Transition and Struggle

-

From PRI to Foxismo

— Guillermo Almeyra -

The Great Strike at UNAM

— Christian Castillo -

How Ultraleftism Divided UNAM Strike

— Phil Hearse - Viewpoints on Trade, WTO, and China

-

The Protectionist Trap

— Caroline Lund -

Lessons of an Ambiguous Struggle

— Mel Rothenberg - Reviews

-

Varda Burstyn's The Rites of Men

— Barbara L. Tischler -

James D Young's The World of C.L.R. James

— David Camfield - In Memoriam: Tony Cliff 1917-2000

-

Tony Cliff, 1917-2000

— David McNally -

Memories of Tony Cliff

— R.F. Kampfer

Malik Miah

POLITICIANS AND GOVERNMENT officials point to the historic low unemployment level in the Black community as signs of a strong economy and a future where whites and African Americans will finally have an opportunity for an equal share of the American dream.

While it is true that long-term unemployment for the African-American population is in the single digits for the first time, the wealth gap between white and Black families continues to widen. According to government statistics Black households’ wealth average one-twelfth that of white households.

Wealth is not defined by your annual income. It is a reflection of assets accumulated (such as real estate and stocks) over time.

According to a study by economist Edward Wolff, in 1995 the median white household’s net worth, minus net equity in owner-occupied housing, was $61,000, compared with $7,400 in Black households. (Report by Mari Queen in the May issue of Emerge magazine)

What are the origins of the wealth gap? Why have so few Blacks have accumulated real estate and stocks? Two words: HISTORICAL RACISM.

What do I mean by historical racism? It is racism woven into society on every level — the bedrock of a society rooted in slavery and segregation, and thus institutionalized. Because our ancestors were slaves, and often lost whatever assets they acquired because of poverty, discriminatory laws or simple cheating, most Blacks couldn’t accumulate very much wealth.

So our great grandparents, grandparents, and parents could not pass on the family property and wealth to us. Inherited wealth amounted to our physical being (labor power) that we could sell to the boss for the best wage possible. Even that was not possible until the slave system was abolished with crushing of the slave owners in the Civil War.

Unfortunately, African Americans didn’t get our forty acres and a mule either. (The modest reparations German Jews are getting we never got!) Jim Crow segregation made us second-class citizens. Own real estate and stock? Who are you kidding? Survival was our number one concern — as it is for most Blacks today.

It took a massive civil rights movement in the 1950s and `60s to get the right to vote in the South. Congress made it law with the 1965 Voting Rights Act. The door was now open for some modest political representation.

Home ownership was still hard to gain because of redlining by the real estate industry. It took a 1968 congressional act to get the first national fair housing laws adopted. Up until the late 1960s U.S. policies preserved segregation and helped keep African Americans from home ownership by refusing to make Federal Housing Administration (FHA) mortgage financing available. Between 1946 and 1959, less than two percent of all federal mortgage insurance assistance was made available to Blacks.

Only after new legislation was written in the 1960s and `70s were Blacks able to take legal action against discrimination in employment, housing and higher education. In my industry (airlines), few qualified Black pilots and mechanics were hired until the `60s. By the 1970s a civil rights suit filed by Black employees forced United Airlines — the country’s largest carrier — and the unions to open up hiring and to promote more Blacks and women. (The unions were required to modify discriminatory work rules.)

Institutional and historical racism is behind the wealth gap. That’s why the gap actually widens in economic good times. Because Blacks as a group start fifty yards behind whites, it’s impossible to catch up without strong affirmative action.

Individual Initiative?

How did working-class whites sprint so far ahead? It really wasn’t through individual enterprise or family savings but rather government policy, as Stephanie Coontz pointed out in her book, The Way We Never Were.

After World War II the GI Bill, available to forty percent of the male population between the ages of 20-24, permitted a whole generation of working-class whites to expand their education.

Similarly, the FHA policy of requiring down payments of only five to ten percent on the purchase price of a house put the federal government in the business of insuring and regulating private loans for single-home construction. Veterans eligible for Veterans Administration loans only needed a dollar down.

Of course African Americans served as soldiers during World War II, but discrimination meant in practice that most were denied access to these programs. Federal loan policies also benefitted the suburbs at the expense of the urban areas, trapping poorer families in the inner cities.

Federal loan policies functioned to systematize the pervasive but informal racism that had previously dominated local housing markets. These policies also starved public transportation and other vital public services, from schools to libraries and parks.

So while it is true that more Blacks have better-paying jobs today, own our homes and even have some businesses, the discrimination we have suffered because of our skin color means we will always be playing catch up. This is true for Blacks in all economic classes relative to white counterparts.

While a color-blind society is what we’d all like to see, it can’t happen until the wealth gap is overcome. That means affirmative action should not only be protected; it must be strengthened. It would also require the government to pay real reparations to every Black person. Being paid a living wage or owning your own home should be rights, not privileges.

The wealth gap, a reflection of the inequalities in U.S. society, can be permanently closed. But to do so requires ending racism — which will mean a third American revolution.

ATC 88, September-October 2000