Against the Current, No. 80, May/June 1999

-

NATO's Road to War and Ruin

— The Editors -

Waiting to Inhale: Culture Wars or Unfinished Gratification?

— David Roediger -

The Fight for Leonard Peltier

— Hayden Perry -

CPE: Demystifying Economics--Interview with Elissa Braunstein

— Stephanie Luce -

Race and Politics: Indonesia's Ethnic Conflicts

— Malik Miah -

A Profile of East Timor's Jose Ramos-Horta

— Conan Elphicke -

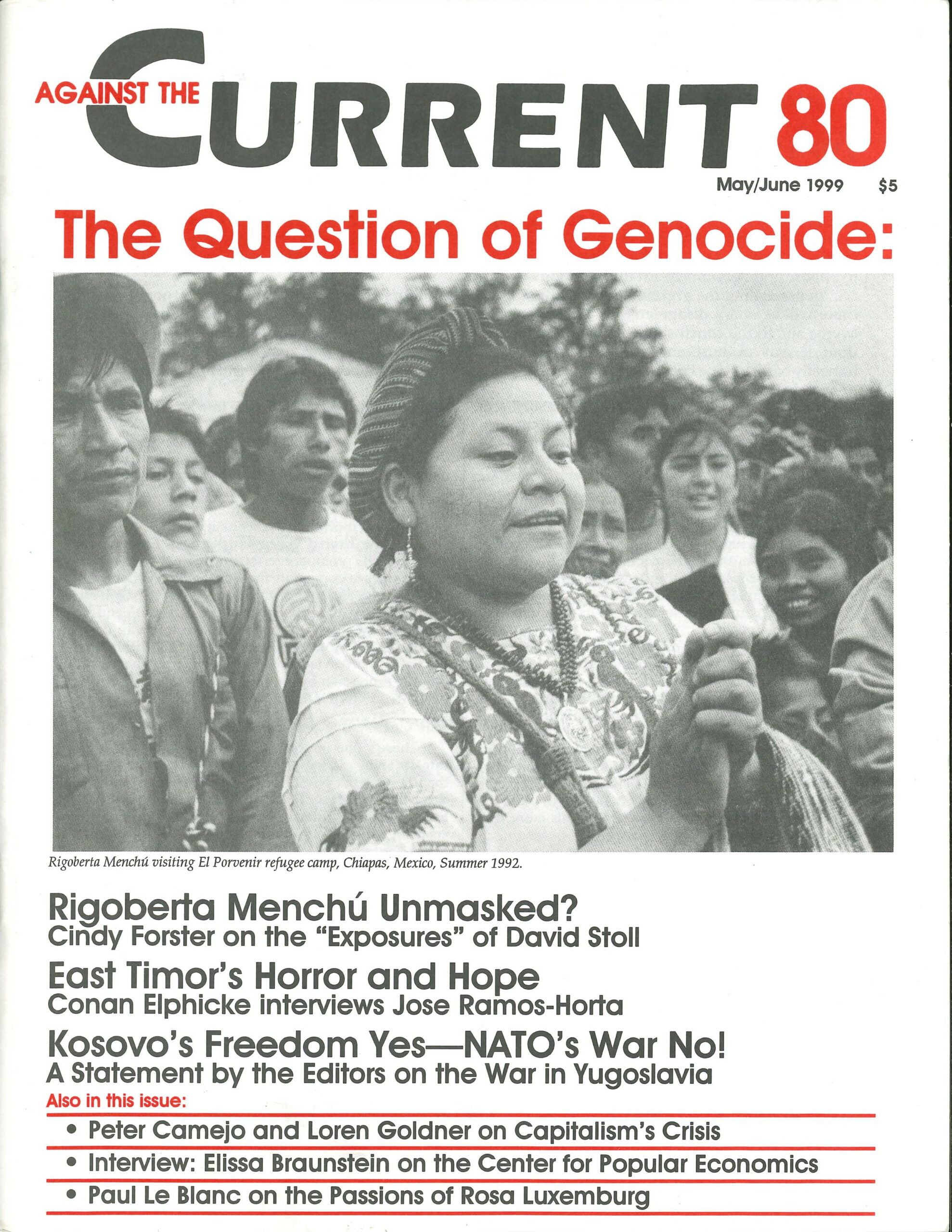

Rigoberta Menchú: A Witness Discredited?

— Cindy Forster -

A Revolutionary Woman in Mind and Spirit: The Passions of Rosa Luxemburg

— Paul Le Blanc -

Random Shots: Weird Sex and Boiled Bacon

— R.F. Kampfer -

The Rebel Girl: A Question of Rape

— Catherine Sameh - Capital's Global Turbulence: A Symposium

-

"Total Capital" Rigor and International Liquidity: A Reply to Robert Brenner

— Loren Goldner -

The Great Bull Market vs. Looming Crisis: On Brenner's Theory of Crisis

— Peter Camejo - Dialogue on Workers in a Lean World

-

On Workers in A Lean World

— Kim Moody -

A Rejoinder

— Ralph Armbruster-Sandoval - Reviews

-

Glaberman and Faber's Working for Wages

— Sheila Cohen -

The Availability of Utopian Thought

— Terry Murphy - Letters to Against the Current

-

Letter and Response on Mumia Abu-Jamal

— Sidney Gendin and Steve Bloom - In Memoriam

-

Comrade and Friend: Bob Strowiss 1919-1999

— Edmund Kovacs

Loren Goldner

It is only in the markets of the world that money acquires to the full extent the character of the commodity whose bodily form is also the immediate social incarnation of human labor in the abstract. Its real mode of existence in this sphere adequately corresponds to its ideal concept. (Karl Marx,

Capital, vol. 1, Part I, Chapter III, Section 3c) (in 1987) . . . the U.S. was still a creditor nation. The returns it earned on its overseas investments helped to offset the impact of its trade deficit, taking pressure off the current account.

These days, the U.S. is a debtor. Rather than investment income coming in, it flows out in the form of debt service. As long as there is no trade surplus to balance the outflow, the debt keeps piling up . . . “It accumulates, and then it compounds, and then it gets really big.

How big is anyone’s guess. But extrapolating from current trends suggests the U.S. will be a basket case by the year 2010 .. . Its foreign liabilities could by then be 50 per cent larger than its foreign assets–the sort of situation found in . . .“semi-bankrupt developing countries.” (Richard Waters, Financial Times, Dec. 7, 1998)

EXCEPT IN SITUATIONS like the near-meltdown of the world financial system in September-October 1998, most people, including most people on the left and far left, do not think much about international liquidity.

Almost a sub-set of a sub-set of the “dismal science” of economics, the subject causes eyes to glaze over quickly in most circles. The apocalyptic mood in world capital markets of last fall already seems like a distant memory, and even most “hedge funds” are paying normal dividends for the fourth quarter of 1998.

It would be vain to predict, with the logic of the broken clock that is right twice a day, when the next global liquidity crisis will occur. It would also be unnecessary. The long-term trends identified by Richard Waters in the above quote are there for all to see.

An occasional columnist for the capitalists’ most class-conscious “newspaper of record,” he has told an important, little-uttered truth about the “Goldilocks economy,” namely that it is an optical illusion in a hall of mirrors.

The United States has long since followed Britain down the road of imperial decline. For more than four decades, it has run chronic balance-of-payments deficits; since 1971, it has compounded this with a chronic balance-of-trade deficit.1

This can go on only as long as foreign holders of surplus dollars are willing to recycle them into U.S. capital markets (including the stock market) to sustain the optical illusion, i.e. as long as they have no alternative except world depression. This recycling enables the United States, once the cutting edge of world industry, to remain the “consumer of last resort” for the world while selling less and less to the world.

“Somewhere along the way,” writes Waters, “foreign investors would have had their fill of dollars,” as they once had their fill of sterling. When that happens, in the absence of a working-class movement capable of taking political and economic power away from the capitalists, the already alarming fall in U.S. living standards (10-20% since 1973, depending on how one measures) will become catastrophic.

This “imperial preference” of the U.S. dollar, first institutionalized by the Bretton Woods system (1944-1971/73) and maintained thereafter on a new, more unstable basis, is what has made it possible for the American capitalist class to defer for decades the day of reckoning on its leveraged buyout of the productive base of the U.S. economy—a process sustained by the decades-long grinding down of American working people, not to mention devastation wrought on working people elsewhere, starting with Latin America and Africa.

This, at bottom, is what “international liquidity” is about and why it should be a central concern of any radical opposition to capitalism, in the United States and abroad, worthy of the name.

Robert Brenner (“The Economics of Global Turbulence,”

But while Brenner touches most parts of the elephant, he does not, like most Marxist attempts to elaborate the current conjuncture, make the dynamic sketched above central enough to his analysis.

There’s wonderful material in Brenner’s account; it saves others, myself included, the trouble of reading a lot of the mainstream literature of the “dismal science,” and has lots of useful statistics.

Brenner basically gets the chronology right. His analysis of the 1965-1973 outbreak of world crisis perfectly encapsulates (though this is not his intent) the period of “New Left” euphoria, largely predicated in the very same years on the “irrelevance” of “economic issues.”

Brenner shows persuasively how each “recovery ”after the end of the postwar boom (71-73, 75-79, 82-90, 92) was more superficial than the preceding one. I agree with Brenner’s attacks on the supply siders and “wage push” theorists—as far as they go.

But one could very nearly get the impression, reading this piece, that for Brenner, unlike for Marx (cf. Capital, vol. III, sections IV and V) finance is purely secondary: a “veil,” as it is treated by mainstream economics, not an autonomous destructive force in its own right.

Brenner does make many points I would make, i.e. 1) the history of the unraveling of Bretton Woods, 2) the great fictitious component of post-1979 investment (LBOs, etc.), 3) the rapid increase in FIRE (finance-insurance-real estate) investments, 4) the increasing disconnect between the stock market and the real economy, 5) the impact of the fluctuations of the dollar on other countries.

But—and this is the major divergence—Brenner doesn’t draw a systematic link between the process of devalorization in manufacture (what I will call “technodepreciation,” to be defined in footnote 2 below) through increased productivity, and the international financial system, as it has evolved to the situation described in the Waters quote above.

What follows is something between a critique of Brenner’s piece, and a series of criticisms. Something about Brenner’s piece reads like a Marxist version of an OECD report, which winds up inadvertently making things sound better than they really are.

Reading it, taking only the case of the United States, I don’t see devastated ex-industrial regions and cities, armies of homeless people, almost 1% of the population in the prison system, and increasing numbers of working-class families squeaking by with 3-4 “MacJobs.” I don’t see the full extent of the hall of mirrors effect described by a very unradical financial journalist.

Value Theory and Crisis

As a general introduction, I register my (mild) consternation at the absence—in a critique of “wage push” theories of the crisis—of a discussion of actual Marxian value theory. I agree, as I said, with Brenner’s attacks on the supply siders and the wage push people. But I don’t think it’s enough—though it’s very important, and rare—to show the source of the crisis of accumulation in the technodepreciation process.2

Our task as Marxists is, after all, to determine the nature of the epoch. An epoch is defined by what preceded it and what will follow it.

To set the stage for an analysis of the post-war boom, Brenner would probably agree that it is possible to see 1914-1945 as one protracted crisis. This crisis broke the logjam that had arisen in 1870-1914 as the United States and Germany arrived at and surpassed Britain’s real economic level, a change not reflected in international economic arrangements until after 1945.

It broke up the empires, particularly those of England and France, which stood in the way of a whole new (U.S.-centered) phase of accumulation, and broke the back of sterling as the international reserve currency, whereby (just as holders of dollars do today), surplus holders of sterling had little alternative to recycling them back into London capital markets and thus subsidizing further British industrial decline.

The “purpose” of the 1914-1945 crisis in accumulation was a vast DEVALORIZATION that re-equilibrated the rate of profit, opening the way to a boom on a whole new scale, but one in which physical destruction of the productive forces (including millions of working class lives in two world wars) took on a new dimension, in contrast to 19th century decennial boom-bust crises of overheating/deflationary bust and depression/resumption of a new cycle, which had been largely “economic” phenomena, however anarchic and painful for working people.

The period 1945-1975 (or more precisely 1938-1975) was “apples” to the “oranges” of pre-1914 accumulation. A far higher productivity of labor made possible the cheapening of mass consumer goods (cars, appliances) and thus increased the content of working-class wages even though wages remained flat or fell as a percent of the total product (the “value” question).

The later phase was centered on a gold-exchange standard3 that in effect already “globalized” international finance in that all central banks began to accumulate dollars as part of their reserves; it realized, in other words, on a global scale what Britain had achieved within the sterling zone in 1890-1914.

Decline of the Nation State

The nation state was already compromised in the Bretton Woods system. U.S. monetary policy became world monetary policy (something that Britain never achieved), as it followed Britain down the road to a rentier economy and then to becoming the “consumer of last resort” described above.

This brings me to another question mark: Brenner’s use of the United States, Japan and Germany as separate economic entities. I know very well that he has massive material on the whipsawing of Japan and Germany by U.S. monetary policy. But why take these three “locomotive” countries in isolation instead of seeing them in a framework of WORLD accumulation? (In a piece titled “The Economics of Global Turbulence,” moreover, almost the entire focus is on “G-7,” i.e. advanced capitalist turbulence.)

It is this tacit, unspoken use of the isolated nation state (which indeed still exists) and neglect of the Third World (i.e. the devastation of much of Africa and Latin America since 1973) that reminds me of an OECD report.

Germany and Japan are the hubs of regional blocs; like the United States, they draw on immigrant labor power from the underdeveloped world (Germany obviously more than Japan, but Japan is getting there), they exploit that labor power abroad (Germany in Eastern Europe, Japan in Southeast Asia) their own currencies became minor reserve currencies after 1973, and the new “euro” may become a major one; they both generate significant international investment that is integrated into their own production process; Germany is at the center of the European Union (EU) and of the process of integrating Eastern Europe into world capitalism.

It is also necessary to say something about the military question, which is still part of the “package” of U.S. relations with Japan and Europe; the United States, after all, still gets a lot of economic leverage with Japan and Korea through its military role in the Far East, and in Europe from its linchpin role in NATO.

A world accumulation perspective would see that the Japanese and German regional blocs labor under the weight of the trillions of dollars the world must still recycle into the “consumer of last resort,” the United States; as long as the dollar retains that status, the idea of an independent Japanese or German capital is a very relative one.4

Profit Rate and the Dollar Bubble

Brenner presents an intricate and original version of the falling rate of profit through the post-World War II period. I do not have the space here, nor have I done the homework, to deal with this fundamental question.

Let’s assume for the sake of argument that Brenner’s version is correct. It may well be, and may well be a breakthrough. My point is elsewhere: Without connecting the rate of profit to the dollar-denominated fictive bubble which must be managed by central banks and valorized globally at all costs, any approximation of such a rate in G-7 countries is dubious.

As Luxemburg says, the rate of profit falls: so what? Does a falling rate of profit mean that the capitalists are going to hand the factory keys over to the working class?

The problem of capitalism are its inability to VALORIZE the total titles to profit, interest and ground rent “through” the total surplus value available on a WORLD scale, at existing rates of exploitation.

The latter, though originating in production, is supplemented by the vast free inputs that come into the system through primitive accumulation: the incorporation of petty producers into the proletariat (i.e. massive immigration from the Third World), the driving down of wages below reproductive levels for labor power (a big part of the story of the United States economy since at least 1957, including the scandal of U.S. schools and health care), the looting of nature, the looting of existing capital plant (e.g. Penn Central up to 1970, LBOs in the 1980s); the non-replacement of infrastructure (requiring $3 trillion or more in the United States after twenty-five years of neglect).

To take one flagrant example, the average jetliner in use by U.S. airlines is over twenty years old! No rate of profit available from current statistics, however critically revised, takes adequate account of these realities if they are not specifically highlighted.

Most Marxist analysis, including Brenner’s, doesn’t adequately distinguish between the “closed system” of vols. 1 and 2 of

It is this problematic which brings finance, and above all international finance, into play, as well as the “free inputs” mentioned above. Most importantly, Marx shows (vol. 2, 394, New York 1967 ed.) that what was a profit for the “merely formal manner of presentation” of vols. 1 and 2 (the single firm) is not decidedly not necessarily a profit for the total social capital.

Without these distinctions, the total profit of “G-7” firms, taken in merely additive fashion, can be highly misleading. In Marx as in Hegel, the totality is not a sum.

Realities of Social Reproduction

Similarly, the social reproduction of labor power, and its erosion in the United States, is not sufficiently emphasized in Brenner’s analysis. The result is, once again, that things wind up sounding better than they actually are.

A simple example: housing costs, which are never discussed, took 15% of an average working class household’s income in 1950; today they take 40-50%. One skilled worker’s paycheck in 1960 supported a family of four; today three and four jobs are often necessary in a family of four.

Brenner provides material on this, but it’s not made central to what has happened. Nor is the lengthening work week. I’m suspicious of any claim about U.S. worker real wages that does not take up these issues. Brenner sees average real wages (including benefits) as flat since ca. 1965; I’d estimate a 10-20% real fall, starting with the setbacks just mentioned.

In talking about G-7 type economies, finally (and above all the United States), Brenner makes no mention of the distinction between productive and unproductive labor. This is a thorny problem, both theoretically and empirically, but Adam Smith’s old formulation that “a man with many workers will soon be rich, a man with many servants will soon be poor” still holds, once one sees most “service” workers as “servants,” starting with civil servants.

Brenner demonstrates very well the further decline of manufacture since 1973, to 15% of hours worked, but does not take up the actual role in accumulation of those “non-manufacture” workers, half or more of whom I would consider unproductive, to mention only the military sector, law enforcement, prison construction and state and corporate bureaucracy, as well as those manufacture workers whose product supports these parasitical sectors.

At bottom, a discussion of value (another remedy for insomnia in most cases) is fundamental in terms of determining the nature of the epoch. My formulation is as follows: the cost of reproducing labor power is the standard of value, the “universal commodity” that makes exchange possible; capital’s fundamental contradiction is its need for living labor power to valorize it and simultaneously its constant tendency, through competition, to expel living labor from production.

Hence the coexistence of robotics and MacJobs, the inability of capitalism to seriously develop most of the world; and (perhaps most importantly) its inability to make gains in productivity gains for society as a whole: This is why the United States work week has increased from thirty-nine to forty-seven hours since 1970, the highest irony for those old enough to remember 1960s “leisure society,” “four-day week” hoopla.

The limits of capitalist accumulation are very elastic, because its ability to recompose for another expansion at a certain point becomes a social and political question. It achieved that recomposition through massive destruction in 1914-1945; it is trying to achieve it again today.

Nevertheless, each epochal crisis represents, for the capitalist world (that part directly in the capital-wage labor relationship, a minority of the world’s population in 1914 and still far from 100% today), a crisis of the OBSOLESCENCE of value (in this “manifold,” after the collapse of the “apples” of 1938-1975 to the “oranges” of 1815-1914, or 1870-1914, or whatever); i.e. value, the contemporary cost of reproducing labor power can no longer be the “standard of exchange.

Labor power becomes too productive to be contained in capitalist social relations. Devalorization has to occur to reequilibrate the system for a new expansion at an acceptable rate of profit. That means ultimately massive destruction of the 1914-1945 type, even if it occurs in dispersed, atomized ways (the Lumpenization of 10-20% of the U.S. population, the boom in prisons, etc.).

Since 1965-1973, capitalism has been postponing any massive, abrupt devalorization of the 1929-1933 variety with credit pyramids and a “slow crash landing,” grinding down “the total social wage” slowly but surely. And that process is hardly over, as the events of August-September 1998 showed.

Perhaps Brenner disagrees. But if he goes to go to the trouble of criticizing other viewpoints from a technodepreciation viewpoint, why not go all the way?

I question Brenner’s statistics, lacking as they do some above-mentioned nuances I consider fundamental. Without any distinction between productive and unproductive labor, and without a serious look at the social reproduction of labor power, and without an awareness of how the vast inflow of foreign capital into the United States stock market, bond market and T-bills skews figures for “American” firms, what can reported figures on “profits” mean, however adjusted?

I understand that the capitalists don’t worry about those things either; they just care about return on investment (ROI). (Nevertheless, Brenner is basically right: any way one measures it, ROI has fallen in manufacture, and he is right to emphasize its centrality.).

Crisis and the “F” Word

Here, in a nutshell, is my theory of crisis, from which the reader can measure my disagreement with Brenner, which may be ultimately more a question of emphasis, but an important one.

Capital, from a Marxian viewpoint, is the M-C-M’ (money-commodity-expanded money) movement. Capitalists “throw” money into investment in the expectation of having “expanded” money later.

But money is not just a veil; total price equals total value only at the beginning and end of a cycle. Along the way there is a constant puffing up of fictitious value which has to be supported by surplus value AND by inputs from outside the “closed system” (capitalists and wage laborers).

These are, as indicated, the looting of non-capitalist classes (petty producers, shopkeepers, peasants), the running down of plant (sunk capital, as Brenner calls it), the non-replacement of infrastructure, the non-reproduction of labor power at current levels of productivity, and the looting of nature (non-replacement of resources and the non-innovation of technology to draw on new resources).

What Brenner rightly emphasizes as technodepreciation through increased labor productivity creates a fictitious increment “f” of fixed assets, indistinguishable to capitalists (and “economists”) and requiring, like all other claims on profit, interest and ground rent, an adequate rate of return.

Over time, this increment “f” becomes a “hot potato” that must be constantly thrown around until it collapses in a general deflation, bringing price back into congruence with current costs of reproduction. Inside the capitalist production process, through technodepreciation, this “hot potato” starts up as the capitalization of plant rendered wholly or partially obsolete by the advance of technology.

Capitalist “net worth” is a multiplier of the cash flow from any given source of profit, interest or rent, and for long periods of time (once again, Penn Central, or Leveraged Buyouts) can have little to do with the “real” price-value relationship.

To keep this growing balloon of hot air afloat, the system issues credit, which temporarily averts a deflation but which just makes the balloon bigger, as it begins to circulate outside the sphere of production.

The “hot potato” in our world is most clearly identifiable as the “dollar overhang,” the trillions of dollars held around the globe, (like the sterling balances of a century ago), which was volatilized by the fall 1998 world liquidity crisis. It is this free floating sum which must periodically be valorized.

This is the “hot potato” which Robert Rubin and Co. have to keep filled with hot air, no matter how many continents have to be destroyed to achieve it. Therefore the international system of loans from New York banks, above all to the Third World and the (soon to be Third World) ex-Soviet bloc and to the “tigers” (above all China) is directly tied to the value of Manhattan real estate (to take one flagrant example, demonstrated in the August-September credit crunch), and is a source of “loot” that helps keep the balloon aloft.

It is the movement of this paper which orders the organization of the “real economy,” up to a point, and not the other way around. Brenner’s analysis details many of the manifestations of this process but does not make it the center piece. That is my fundamental criticism.

Notes

1.“Balance of trade” refers to a country’s total imports and exports of goods and services; the “balance of payments” includes trade but adds all inflows and outflows such as foreign investment and repatriation of profit. The U.S. balance of trade surplus declined through the post-World War II period and turned negative in 1971, the year Bretton Woods collapsed. Into the Reagan era, U.S. investments abroad produced enough surplus to compensate for a negative balance of trade, but massive U.S. borrowing from foreigners, above all Japan, wiped out that surplus too. The total U.S. balance of payments deficit for 1999 will be between $150 and $200 billion, further swelling the total U.S. foreign debt highlighted in the

2.“Technodepreciation” means the lowering of the real (replacement) value of a capital investment by an advance in the productivity of labor in excess of the normal capitalist accounting writeoff of fixed capital over the normal life of a machine.

3.The “gold-exchange standard” superseded the old gold standard in 1944 when the Bretton Woods system defined the U.S. dollar as a “gold equivalent,” i.e. “paper gold” which foreign central banks could hold as a reserve as they held gold. Nixon unilaterally disconnected the dollar from gold in 1971, and by 1973 the dollar simply “floated” against all other currencies. One economist described this as “a shift from `paper gold’ to `paper paper.’

4.To say that the independence of the German and Japanese blocs from U.S. hegemony is very relative is not to say that inter-imperialist rivalry has disappeared. It merely means that the obligation of Germany and Japan to support the dollar or else risk depression and the collapse of their major export market is a tremendous weapon which the U.S. has used against them repeatedly.

ATC 80, May-June 1999