Against the Current, No. 48, January/February 1994

-

Those Giant Sucking Sounds

— The Editors -

Voucher Mania: Will It Spread?

— Joel Jordan -

The Unmaking of Mayor Dinkins

— Andy Pollack -

The Illusion of Middle East Peace

— Nabeel Abraham -

An Information Center for the Russian Workers' Movement

— Alex Chis and Susan Weissman - Defend Human Rights in Russia!

-

On Mythology and Genocide

— Branka Magas -

Behind the Turmoil in Italy

— Jack Ceder -

The Rebel Girl: Having A Bobbitt Sort of Day?

— Catherine Sameh -

Random Shots: The Spirits of the Season

— R.F. Kampfer - Chronic Fatigue Demonstration

-

Working-Class Vanguards in U.S. History

— Paul Le Blanc -

Puerto Rico's Plebiscite

— Rafael Bernabe -

Section 936: A Corporate License to Steal

— Working Group on Section 936 -

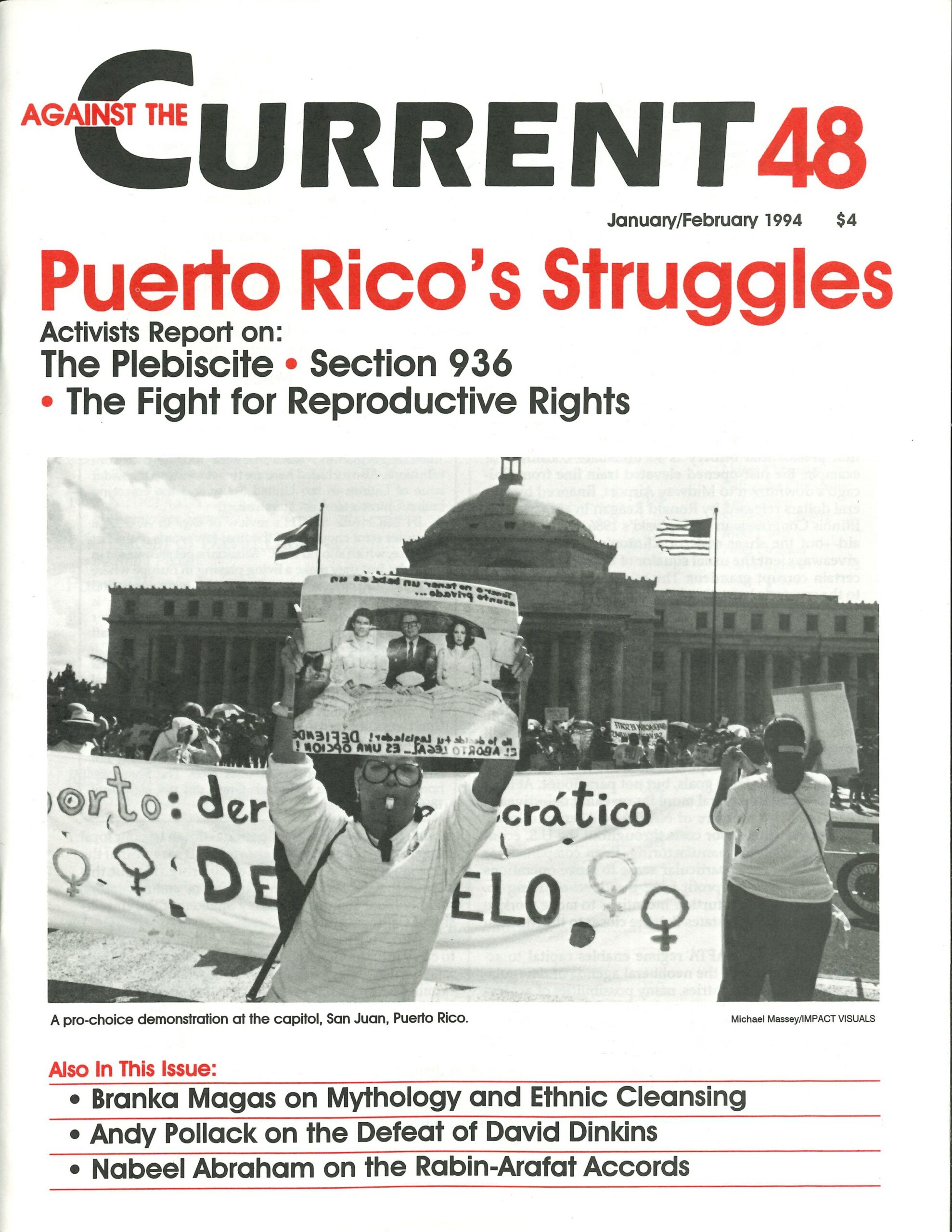

Confronting Anti-Choice Forces in Puerto Rico

— Ruth Arroyo, Rafael Bernabe and Nancy Herzig -

Al Norte

— Ruben Auger - Notes

-

Latinos: One Group or Many?

— Samuel Farber -

Latina Writers Defying Borders

— Norine Gutekanst - Reviews

-

Socialism as Self-Emancipation

— Justin Schwartz - Remembering E.P. Thompson

-

E.P. Thompson: 1924-1973

— Michael Löwy -

E.P. Thompson as Historian, Teacher and Political Activist

— Barbara Winslow

Working Group on Section 936

SINCE PRESIDENT CLINTON’s proposed modifications to Section 936 of the Internal Revenue Code in his 1993 State of the Union address, there has been a great deal of controversy around the future of Puerto Rico’s economy. Specifically, debate has focused on Section 936, which provides tax-incentives for U.S. corporations operating in Puerto Rico. On one side is the U.S. Treasury, which sees the tax benefits to U.S.-owed corporations as excessive, particularly during a period of fiscal restraint. On the other side are the corporations, who want to maintain the high profits they receive from their island operations.

Puerto Rico’s Commonwealth Party (PPD) has always been a strong defender of Section 936. But, this time, the local government was headed by the Statehood Party (PNP), which saw the retention of Section 936 as an obstacle to their goal of statehood. Nonetheless, the lobbying effort on the part of the corporations—and their threat to eliminate their operations on the Island—has been so strong that most island and mainland politicians with an interest in Puerto Rico quickly fell into line, defending the provision.

A number of pro-936 lobbying organizations have argued—through publicity campaigns in the mass media and with politicians in Washington—that Section 936 is vital to the profitability of U.S. corporations operating in Puerto Rico, to the workers who are employed there and to the overall health of the economy. However, a closer analysis reveals that Section 936 has essentially become a tax loophole available to the accountants and planners of U.S.-owed corporations. While it has increased their profits, it has not proven to be an effective job-creating mechanism.

The lobbying campaigns on behalf of Section 936 have been waged from the corporations’ viewpoint. In fact, pro-936 lobbying organizations receive funds from, and represent the particular interests of, some of the most powerful U.S.-based transnationals These include many pharmaceuticals—Johnson & Johnson, Pfizer, Merck, American Home Products, Abbott, Baxter International, Bristol Meyers, Eli Lilly—and transnationals Coca-Cola and Pepsi Co.—as well as several large financial institutions.

In this document we will provide a critical perspective of Section 936 and call into question claims made by lobbying groups about its so-called benefits for Puerto Rican working people. Our goal is to broaden the spectrum of the debate over Section 936 and, more importantly, to stimulate discussion about alternative economic scenarios—from the point of view of the Puerto Rican working classes.

“Operation Bootstrap”

Since 1947, when the economic model “Operation Bootstrap” was launched, Puerto Rico has tried to develop its economy by attracting U.S. capital—mainly through tax exemptions, rent subsidies and low wages. The goal: to develop an industrial system of production for export that would benefit from Puerto Rico’s access to the U.S. market. This strategy was predicated—and continues to be oriented—around the availability of external sources of investment, which does little to ameliorate Puerto Rico’s recurring economic crises. In fact it has accentuated the island’s dependence on the fluctuating, and unreliable, external uses of its productive factors.

Particularly after 1973, the main indicators assessing Puerto Rico’s economic performance have shown signs of stress. The unemployment rate on the island, for example, fluctuates between 14%-24% while rates of participation in the labor market are substantially lower than those in the United States. Other clearly detrimental features include:

1) The gap between the GNP and the GDP has increased steadily over the last two decades, indicating that native capital formation has been thwarted by the penetration of U.S. firms as well as by the substantial quantities of capital that leave the island after moving through the social circuits that characterize the process of production, consumption, and accumulation.

2) Despite the full application of federal minimum wage standards in Puerto Rico, average wages remain the same relative distance from the U.S. per capita wage as they were in 1973. Per capita personal incomes also remain as they had been at the start of Operation Bootstrap (table only available in print edition).

3) By 1990 some 60% of the Puerto Rican population—on the island or on the mainland—was living in or near poverty. Many individuals were partially dependent on federal transfers, which despite cutbacks over the last decade or so, have sometimes surpassed the profits generated by U.S. businesses in Puerto Rico.

4) A 1979 U.S. Dept. of Commerce report characterized Puerto Rico as a “tandem economy,” that is, one effectively absorbed into the U.S. productive apparatus. By the mid-1980s, 85% of production was for export while 45% of food consumption was imported from the United States. Essentially, North American firms effectively monopolized banking, transport, tourism and high-tech manufacturing. U.S. multinationals have also made steady incursions into the growing service sector of the economy.

During the current budget discussions, Section 936 corporations defended their tax breaks by arguing that they were defending the interests of workers in Puerto Rico. The irony of their lobbying effort is that they claimed any modification of the provision would automatically mean that jobs would leave. In fact, they are the very corporations who would make the decision to leave if their super-exploitation of Puerto Rican labor was not protected.

Our critical look at the role of 936 corporations in Puerto Rico is based on a concern over the welfare of Puerto Rico’s masses and informed by these facts:

• Section 936 companies have not created the level and quality of jobs that they promised. Although 936 was conceived to create new manufacturing jobs in Puerto Rico, manufacturing employment remains stagnant. Between 1970-90, while 2,243 plants and 29,847jobs were created, 1,931 plants closed down, eliminating 51,800 jobs. This net loss of more than 20,000 jobs was partly due to the substitution of labor-intensive industry with capital-intensive industry, the latter being generally favored under the present income-based tax credit of Section 936.

• Section 936 companies, especially pharmaceuticals, are strongly anti-union. They have violated the already weak worker health and safety laws for on-the-job protection and transgressed the environmental standards that seek to protect surrounding communities.

These corporations—especially the pharmaceutical companies—pay workers lower wages than what workers in the mainland earn for similar work. They have employed elaborate screening techniques, blacklisting workers and hiring union-busting law firms to ensure that workers are not permitted their right to organize into unions. By 1992 only one of the seventy-two pharmaceutical plants was unionized—and it has been under serious attack with a decertification attempt.

• Section 936 corporations have generated and kept tax-free super-profits at a time of economic difficulties both in the United States and in Puerto Rico. They pay no taxes to the federal government and only minimal taxes (usually less than 5% of their revenue) to the Puerto Rican government.

• Section 936 has resulted in Puerto Rico’s extreme economic dependency on U.S. multinationals. It has not helped to foster an horizontally and vertically integrated national economy.

How Section 936 Works

Section 936, a provision of the U.S. Internal Revenue Code, was passed in 1976, replacing an earlier tax-incentive law. Section 936 exempts U.S.-based companies operating in Puerto Rico and other U.S. possessions from paying federal income taxes on the production of their subsidiaries. Companies are charged a 10% “tollgate-tax” by the Commonwealth on profits repatriated to the United States.

By the time Section 936 was passed, more than one out of five of the Fortune 500 companies already operated subsidiaries in Puerto Rico. Not only are those subsidiaries exempt from federal income tax, but they are also allowed to increase their non-taxable incomes through depositing their profits in special bank certificates. As a result of this provision, known as the qualified possession source investment income (QSPII), a relatively large pool of investment capital is managed by U.S. banks (Citibank and Chase Manhattan) through their offices on the Island.

It has been well documented that U.S. corporations have manipulated their finances to use Section 936 to their advantage in a number of different ways. Through creative accounting, the profits from the parent company are transferred to the 936 subsidiary (as profits in Puerto Rico). Companies also sell their patents to a 936 subsidiary so that royalties on the patents become tax-free. Another method of transfer is through overpricing products “sold” from their Puerto Rico plants to the mainland and underpricing products “sold” to the Puerto Rico plants. There are numerous cases of companies that have been accused and found guilty of using transfer pricing to declare tax-exempt profits, including Eli Lilly, Parke Davis, Pfizer, Abbott Laboratories, G.D. Searle and Timberland.

In sum, Puerto Rico has become a tax haven for U.S. corporations, especially in capital-intensive industries like pharmaceuticals, precision machinery and chemical products. Annually Section 936 corporations make over $10 billion in profits and save $3 billion in taxes. More significantly almost $2 billion of the savings accrue in the capital-intensive pharmaceutical companies.

Increase in Joblessness, Migration, Speedup

Since the implementation of Section 936 joblessness in Puerto Rico has increased, from about 15% to around 20%. This has occurred despite the fact that migration has accelerated. Between 1977-1988, around 25,600 people left the island annually. This is the highest rate of migration since the beginning of Operation Bootstrap.

936 companies often employ temporary and part-time workers through temporary employment agencies. Some, like American Home Products, have abused programs like the Job Thaining Partnership Act by engaging in the shady practice of hiring students at subsidized wages for short periods of time (with no intent to train them for permanent jobs).

U.S.-owned companies relocate production to Puerto Rico, resulting in the loss of mainland jobs. In a study of twenty-five plant relocation cases (sixteen of them pharmaceutical or medical product companies, most located in the Northeast), the Midwest Center for Labor Research found that over 7,000 direct jobs and up to 30,000 indirect jobs were lost as a result of Section 936-related layoffs or plant closures. Two examples of recent runaways are American Home Products from Ellthart, Indiana to Guayama and Acme Boot from Clarksville, Tennessee to Toa Alta.

But the 936 corporations rarely add jobs, in net terms, when they relocate in Puerto Rico. Rather, the island has become a key part in the process whereby capital seeks the conditions that minimize its internal production cost and create large social costs. Once factories relocate, they do not merely reproduce the original operation. Instead the pace of production is increased—through the introduction of new machinery, consolidation of work and new work standards. Accompanying the speedup is a reduction of workers’ salaries and fringe benefits.

936 funds are an integral part of the chain of exploitation. They are used by banks and financial institutions to provide low-cost loans designed to finance the relocation of plants and jobs from the mainland and Puerto Rico to the Caribbean and Latin America. Profits deposited in Puerto Rico by 936 companies finance export-oriented manufacturing—and the subsidized destruction of jobs and the erosion of labor rights—and play an important role in promoting the Caribbean Basin Initiative of Presidents Reagan and Bush.

Privatization in Puerto Rico

The Puerto Rican government collects a relatively insignificant amount of taxes from the 936 companies and subsidizes them in many ways Officials have tried to cope in two ways. First, they have allowed the government to amass a huge debt, around $14.5 billion dollars in 1990, up from only $1.6 billion in 1970. In fact, Puerto Rico has become one of the most indebted countries in the world, with each inhabitant owing close to $3,000. Second, even with increasing demand, there has been a reduction in the quantity and quality of governmental services. At the same time there is a general increase in the proportion of taxes paid by Puerto Rican workers.

In Puerto Rico 936 corporations play an active role in the Strategic Planning Council of the Private Sector. This council pressured the government to undertake massive privatization. So far the Telephone Company, the Highway Authority, the Public Education System, the Housing Authority, the Metropolitan Bus Authority and the public hospitals have been affected. As part of making the different public agencies more attractive for – possible buyers, thousands of public workers have been fired.

Environmental Ill Health

936 companies often ignore health and safety conditions in the workplace. Some of them, like Parke Davis, have been found guilty of exposing workers to highly toxic materials without adequate rotection. Parke-Davis, a subsidiary of Warner Lambert, has also been guilty of violating quality standards by the Federal Drug Administration. In another case, the workers of Ortho Pharma that corporations which makes chemical contraceptiives, were exposed to chemicals that affected their hormonal systems. (Many male workers began to grow large breasts.) The non-union conditions in the pharmaceuticals leads many safety and health conditions to go unreported.

Some Section 936 companies (again, mostly the pharmaceuticals) have caused significant and irreparable damage to the environment, workers and their communities. According to the Environmental Protection Agency (EPA) and independent environmental studies, they have polluted areas of Puerto Rico, further undermining the scarce natural resources of the island and contributing to the decline of local industries, especially fishing and agriculture.

The environmental damage is so great that the Environmental Quality Board office in Puerto Rico estimates that 10% of Puerto Rico’s coastline is unfit for swimming. EPA studies point to those municipalities with greater concentrations of pharmaceuticals (like Barceloneta, Manati, Guayama, Humacao and Carolina) as the regions with the largest toxic waste. The only waste-treatment facility for hazardous waste fluids in Puerto Rico, owned by Safety-Kleen Corp., is inadequate for the island’s large concentration of chemical companies. It has recently been fined by the EPA for violating environmental laws.

Seventy-two percent of all toxic waste in Puerto Rico is the result of dumping by a handful of chemical companies. The 1993 EPA report on toxic waste singles out companies like Schering,Du Pont (Manati); Abbott, Upjohn, Viskase, Merck. Sharp and Dohme, Pfizer, Sterling (Barceloneta); Phillips (Guayanta); and Squibb (Humacao). In 1991, the EPA identified Phillips, Chevron, American Home Products, Revlon, General Electric, Becton Dickinson, Upjohn, Motorola, Harman Automotive, Teledyne Packaging, the U.S. Defense Department and the Puerto Rico Industrial Development Corporation Co. as responsible for twelve of the island’s most hazardous waste sites. EPA estimates that the cleanup of each site will cost $20 million—a total of $240 million.

Profits and Taxation

Section 936 corporations have generated tax-free super-profits. U.S. corporations (virtually all of them 936 companies) attribute one-fifth of all their foreign direct investment profits to their Puerto Rican operations.

Excessive profits have been obtained by high-tech, capital intensive companies (like those in pharmaceuticals, scientific instruments, electronics, and electrical machinery). For instance, only seventy-seven of the 500 companies benefiting from this tax incentive are pharmaceuticals, yet that single industry obtains half of the total 936 tax savings. The financial and political clout of pharmaceuticals in Puerto Rico is disproportionate, especially given the relatively few jobs they create.

Most of the $3 billion dollars of annual tax savings are captured by a handful of companies. In 1989, for example, $1.123 billion in federal taxes were avoided by just 13 companies. The leading tax savers were: Johnson & Johnson ($147 million), Coca-Cola ($143 million), Pfizer ($106 million), Merck ($105 million), Digital ($88 million), American Home Products ($80 million), Abbot ($79 million), Baxter International ($75 million), Bristol Meyers ($64 million), Eli Lilly ($53 million), Pepsi Co. ($52 million), Schering-Plough ($49 million), Upjohn ($49 million) and Warner Lambert ($39 million).

Section 936 companies contribute little to the treasury of the Puerto Rican government Tollgate taxes, designed so the Commonwealth can recover up to 10% of the profits that 936 companies repatriate, are often waived or go uncollected. In fact, these taxes represent just 2% of the government revenue (instead of the 12% often quoted by 936 defenders). As a result of so many tax exemptions granted to the 936 companies, sales and income taxes for Puerto Rican households and businesses are among the highest under the U.S. flag.

By virtue of their gross profit margins, the multinational character of their operations and the large proportion of patented products, capital-intensive companies can readily use “transfer pricing” to declare profits in Puerto Rico and thus avoid paying additional income taxes in the United States.

Puerto Rico’s Economic Dependence

Section 936 has accentuated the extreme economic dependency of Puerto Rico’s economy on U.S. transnationals and impeded the formation of a self-reliant and integrated process of economic development to serve the multiple needs of the Puerto Rican population. Section 936 has thwarted the development of native industry by steering the economy towards largely exportoriented, capital-intensive, highly toxic manufacturing production with few linkages to other parts of the Puerto Rican economy.

Section 936 has also subordinated the economy of Puerto Rico to the United States, thus promoting underdevelopment Puerto Rico’s disproportionate reliance on a single instrument of economic stimulus (federal income tax exemption) over which it has no political control is a very fragile and unstable foundation for long-term growth. Since the passage of 936, the island’s dependency on external investment has actually increased, with these companies accounting for two-thirds of manufacturing employment and more than half of exports and national income.

The largest fraction of 936 profits are not reinvested to expand capacity in Puerto Rico but kept in the form of passive (financial) investments. These funds amount to more than $15 billion, compared to less than $5 billion invested in plant and equipment.

About $10 billion of the passive (financial) investment are bank and other financial deposits. More than $5 billion are kept as financial instruments by 936 corporations, the bulk of which are Caribbean Basin-oriented bonds. As a result, they contribute little to the island’s long-term economic development. Financial deposits of 936 profits (“936 funds”) generate excessive profits for the local banking industry, which is dominated by a few U.S. and foreign banks. Less than 10% of the 936 deposits are held by the Economic Development Bank and other public financial agencies indirectly, and even this fraction exists only as a result of recent local regulations.

What Happened To Clinton’s Proposal?

As part of its economic plan, the Clinton administration proposed to reform Section 936. The plan called for substituting the income tax credit with a wage credit over three years, starting in 1994. Wages and salaries up to the current FICA income cap ($57,600) would have qualified for this credit. Under this credit, Section 936 companies would have deducted from their corporate income taxes up to 60% of wages paid on their Puerto Rico companies—a total of more than $1.3 billion annually (half of the current total income credit). In sum, the administration sought to raise from 936 corporation $7.4 billion dollars over a period of five years.

The changeover from the tax credit to the wage credit would be such that in any given year during the three-year transition period companies would choose to receive either credit. Additionally, the corporations would receive an investment credit of 80% of the (depredated) value of all investment in plant, equipment and inventories on their subsidiaries—a significant credit for high tech companies.

The Clinton initiative did not seek to completely eliminate Section 936. While shifting from an income tax to a wage credit would greatly reduce tax savings now enjoyed by a handful of sectors (including pharmaceuticals), the large majority of companies would have obtained substantial tax savings. Tax rates for Section 936 would be substantially lower than in the United States, especially with state and local taxes were factored in.

The Amalgamated Clothing and Textile Workers Union conducted a study of Clinton’s proposal, concluding that the impact would have modestly reduced tax savings of 936 companies in Puerto Rico. On the average, the companies would have ended up with an 18% corporate tax rate (compared to Clinton’s proposed 36% U.S. corporate tax). Such a significant tax differential would have maintained Section 936 as a major incentive. (Recent estimates by the Economic Development Administration and the Economic Development Bank of Puerto Rico indicate that corporate tax rates for 936 companies may have been even lower. According to their own calculations, the average 936 corporate tax rate may have been only 15.4%.)

From the very beginning, the government of Puerto Rico—in conjunction with 936 corporations and business associations—opposed Clinton’s proposal. A powerful lobbying effort fought to retain as much as possible of the 936 income tax credit. With the support of Puerto Rican Congressional representatives and local leadership, that lobbying effort reduced the impact of Clinton’s reform. Now companies will have the option of receiving either a 95% wage credit (with additional tax credits on investment and fringe benefits) or a 60% income-based tax credit This option will raise an estimated $3.5 billion over five years. It also leaves the decision over which plants can qualify to Puerto Rico’s Economic Development Administration—essentially eliminating the runaway plant provision from the original bill. Thus the reforms to Section 936 have been accepted by the 936 companies, the Puerto Rican government and the local press.

The manufacturing sectors, accounting for 70% of 936 jobs, will experience only a small reduction (or no reduction at all!) of their tax savings. In fact the six most labor-intensive industries (apparel, textile, paper, fabricated metal, leather products and rubble, which employed over 55,000 people in 1989) will likely see their taxes unchanged. Four high-tech industries employing over 40,000 people in 1989 (industrial machinery, electrical equipment and electronic products, petroleum and scientific/medical instruments) will see a modest income tax rate increase, from 11.6% to 14.6%.

The most affected industries will see their tax rates increase to no more than ten percentage points below the U.S. corporate tax rate. Food and kindred products, which employed 20,000 people in 1989, could end up paying an income tax rate of 19.8%. But the major beneficiaries of 936 credits in this industry are also those that employ fewer number of workers. Just two companies, Coca Cola and Pepsico—which receive as much as 23% of their total global profits from their Puerto Rico operations—accounted for two-thirds of all tax savings in food processing in 1989. Yet they employed only 4% of all 936 food processing workers—less than 500 jobs. These and a few other food processing companies enjoy average pre-tax operating profit rates in Puerto Rico that are four times higher than the corresponding pre-tax rates in the United States.

In 1991, Coca-Cola obtained $137.4 million in tax savings, about $371,350 in 936 benefits per employee, five times more than the benefits per employee received by the average pharmaceutical company, fifteen times more than those of an average 936 manufacturing company. Yet Coke employed only 371 people in Puerto Rico and paid no local tax.

Section 936 companies in the chemical industry may end up paying an average 26% corporate income tax rate—still ten percentage points less than the proposed U.S. rate. But the sector most impacted will be the pharmaceutical industry, which employs less than 20,000 people and earns more than half of all 936 benefits. Companies in the chemical industry enjoy an average pre-tax operating profit rate seven times higher than in the United States. By virtue of their high volume of net profits ($4.6 billion), U.S. chemical companies in Puerto Rico will continue to save a substantial amount of federal taxes—almost $400 million or more each year.

936 Vs. Development

As we have shown, Section 936 has principally benefitted U.S. multinational corporations, not Puerto Rican workers or their economy. Though recent changes to 936 begin to deal with the most serious shortcomings of federal tax incentives, we believe that it still falls short of what Puerto Rico needs to develop a solvent national economy. Any future reforms of Section 936 and discussion of Puerto Rico’s economy must take into account the following short-term and long-term concerns:

A. Any tax incentive plan should actually stimulate job creation (through wage credits and other mechanisms) and tax passive (financial) income.

B. Federal tax revenue must be redirected into the Puerto Rican economy to rebuild local infrastructure, to invest in plant, equipment and personnel for education, to provide better health care and to solve the social problems that result from Puerto Rico’s fiscal crisis and public divestment The privatization campaign waged against public sector employees must be stopped.

C. Tax incentives should be denied to companies that violate workers’ rights, occupational health, safety and environmental regulations, or that run away from the United States or from Puerto Rico to other parts of the Caribbean Basin. We believe that investment programs and policies should seek to complement production and amplify it across locales, not substitute for it.

D. Puerto Rico must be allowed and encouraged by the United States to break its economic dependency on transnational corporations and to create an integrated economy that combines foreign and local, public and private investment. Puerto Rico needs economic self-determination that places the current and future generations of Puerto Rican people, instead of foreign investors, at the top of the national agenda. This alternative economic model should favor locally-owned cooperatives, and provide incentives for small- and medium-scale local investment. The goal of any policy, in our view, should be to improve the wages and working conditions of all Puerto Rican workers.

E. Puerto Rico’s unions and other grassroots organizations should be given full participation in public policy decision making.

F. The issue of Puerto Rico’s political/economic relationship to the United States must form part of any serious discussion of Puerto Rico’s economic future—given the determinant role played by the colonial model on the island’s process of socio-economic development In addition, both national and international calls for the decolonization of Puerto Rico should be heeded and understood as part of the process of creating economic self-determination for the island (see Committee of Union Organizations’ Presentation at the United Nations of 1992).

January-February 1994