Against the Current, No. 46, September/October 1993

-

Letting Bosnia Die

— The Editors -

Haiti: Democracy for Whom?

— an interview with Cecilia Green -

University of California vs. People's Park

— Nancy Delaney and David Linn -

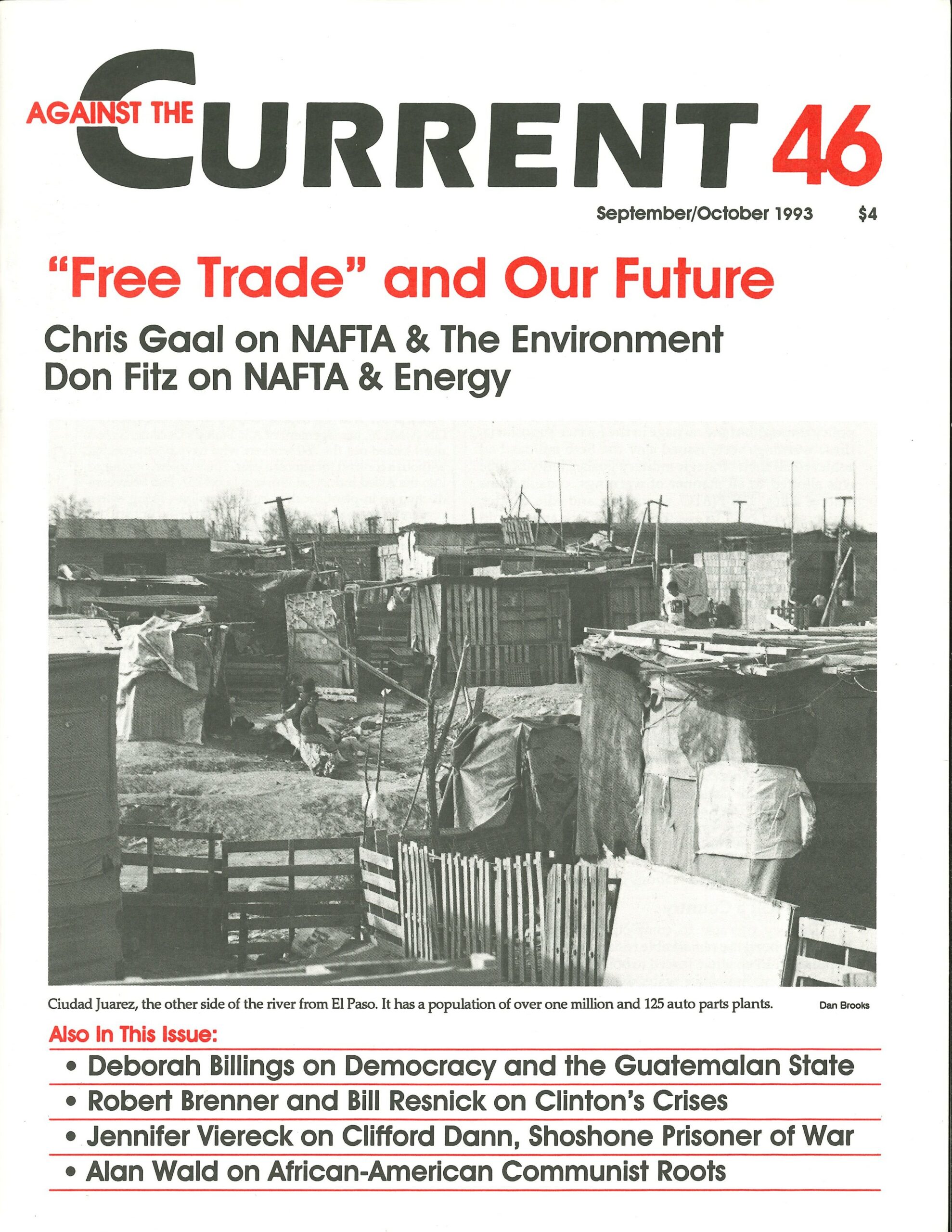

The Environment & Free Trade

— Chris Gaal -

Energy, Especially Oil and NAFTA

— Don Fitz -

Failing to Bring the State Back In

— Robert Brenner -

Stealth Reforms and Its Limits

— Bill Resnick -

Clifford Dann, Shoshone Prisoner of War

— Jennifer Viereck -

Guatemala: Politics and Possibilities

— Deborah Billings - Mexico Oil Workers Protest

-

The Rebel Girl: The Limits of the Law

— Catherine Sameh -

Random Shots: The Wars of the World

— R.F. Kampfer -

A Response on Che, Cuba and Revolution

— Jeanette Habel -

"Dynamic" vs. "Superior"

— Paul Buhle - Reviews

-

African-American Communist Roots

— Alan Wald -

Work: Alienating or Transforming?

— Douglas Wixson -

The Free Press and Thought Control

— Ethan Casey

Bill Resnick

WHO IS BILL Clinton and how should we understand the new administration? Are they basically technocratic neoliberals committed to rationalizing the U.S. economy for an edge in furious international competition? Are they stealth social democrats (as right wingers hysterically tell their troops) pushing public planning and income redistribution with cunning maneuvers? Or are they virtually exhausted of any political commitment, scrambled by years of compromise and dealing, desperately trying to muddle through and get reelected?

Clinton’s early record of cowardice and irresolution suggest the 1atter, it happens to politicians without a real popular base keeping them honest But it’s too easy, probably wrong and not useful to see Clinton’s failures as matters of conviction or character. We do better and learn more taking Clinton as a real reformer who recognizes that the immiseration of maybe a third of America is very costly and threatens social and economic stability. And who more ambitiously, like Roosevelt, wants to save capitalism despite capitalist resistance.

But reform faces enormous constraints. Why could Clinton not carry out his campaign promises even had he wanted to? Why did a mild reformist program become an austerity budget? What are the limits to stealth reform? Can capital be disciplined? Can an international regulatory pattern be imposed? And for folks maintaining quaint commitments to a more just distribution of wealth and meaningful democratization, how should one engage the Clinton program? What can and should be proposed? How could a left intervene in the situation likely to prevail?

Clintonomics has four parts:

I. The Budget. The “bold economic agenda” of his campaign was actually a timid Keynesian stimulus package which under the pressure of the presidency became a relatively humane austerity budget emphasizing deficit cutting. Congressional fulminations and deal making notwithstanding, the deflationary budget being enacted (a little meaner but fundamentally the budget Clinton proposed) has broad elite support But austerity reduces demand for products and workers; it’s recessionary.

II. Domestic Finance and Investment Incentives. Clinton’s campaign to satisfy capital and promote investment is mostly focused on interest rates, which have remained low (though the Federal Reserve keeps making ominous noises). But while high interest rates discourage investment, relatively low rates only generate investment when goods and services are selling, capacity is near exhausted, and there are profits to make. Up to now the net of housing sales (up a bit), consumer credit (up a bit), and capital investment (low and steady) are only enough to maintain a weak economy.

III. International Finance, Dade and Coordinated Reflation. Clinton’s hoping that wheels and deals around a big set of relatively low visibility international issues—trade (NAFTA a minor part)’ coordinated stimulus, interest rates, currency values and monetary and finance arrangements—can boost the U.S. economy sufficiently to get him reelected.

IV. “Industrial Policy.” Clinton’s “industrial policy” (education, training, research, enterprise and technology incubation, conversion, government industry consortia, labor management cooperation) is sold as innovative, visionary, etc. Actually, it’s a bit more money for what the Bush administration had already reluctantly begun, with a central role for high tech and the military. It will be enacted because this newest form of pork and payoffs gives the appearance of meaningful action. But its economic impact will be minimal, amounting to meager public welfare for selected companies and a minor jobs program for scientists, technicians, and associated workers.

This is a rich country and capitalism is in better shape than apocalyptic accounts sometime imply. While current economic arrangements significantly constrain public action, the U.S. president has considerable room to initiate change, perhaps even in the rules of the game that now generate deflationary pressures. Clinton could well preside over an economy adequate to get him reelected (in what promises to be a very messy race). A left must operate in a complex environment of capitalist recomposition and readjustment Excoriation of Clinton’s multiple deceits, betrayals and compromises is not enough. Let’s take Clinton reform seriously, to at least be clear minded on what it would take to win reform, and what could succeed.

I. The Budget—A Consensus for Austerity

For the past ten years elite economic managers and politicians, here and abroad, have urged the United States to reduce the budget deficit by cutting federal programs and raising some taxes. With the deficit demonized and deficit cutting the soul of virtue, austerity has found its agent, a “moderate” Democrat With all his pitiful missteps and humiliations (hairdos, gays, flip-flops, Guinier, Gergen and more), it’s easy to miss that Clinton’s budget moved along quite smartly. The mix of tax rises and program cuts that ultimately exited the Congress closely resembled the austerity budget Clinton proposed.

Clinton’s campaign program emphasized jobs and investment, advocating a major stimulus program to strengthen the economy for subsequent spending cuts. As president, though, Clinton embraced deficit cutting, and proposed an austerity budget, albeit relatively humane. In the end, it appears the poor will have marginal gains—the earned income tax credit, rises in food stamps, child care and greater access to health care. And the rich will likely pay a bit more in taxes. On a macroeconomic level though it cuts federal spending, which amounts to a reduction in public jobs and reduced stimulus to the economy. The employed poor may be somewhat better off but more families will be forced into poverty.

Clinton’s austerity budget was the only game in town and had no significant opposition. The major business lobbies (the Chamber of Commerce, National Association of Manufacturers and Business Roundtable) successfully sought to reduce the corporate tax rise and change the energy tax. But they did not organize against the total package, and were thus basically indicating support Clinton’s vociferous opponents (the last of the free marketeers and supply siders like George Will, The Cato Institute, the National Review, Wall Street Journal editorialists, talk show right wingers), like all losers, are still fulminating about the apostasy of old allies; the Chamber of Commerce, once reliably and noisily Reaganite, has become the whipping boy.

Congress, Republicans included, basically approved the austerity package. There was no alternative plan, but few believe it will do any better than maintain the status quo (slow growth and lots of pain for middle America). In that circumstance, the Republicans had the easy role; they just attacked and waited for their turn in ’94 and ’96. For Democrats in Congress, the whole game was to shift the political costs of continued pain to Clinton, thus to run away from the Clinton plan while passing it, leaving Clinton holding the bag and the target for anger Except for representatives from quite liberal areas, Democrats took potshots at Clinton, fulminated against “tax and spend,’ attacked the deficit, pretended independence and won some pork for the folks back home, then basically voted for the package. If things turn somewhat better, they can take credit; and if Clintonism fails, they can blame Bill.

Kerry, Decondni, Moynihan, and Breaux played that game on national TV; the rest of the “moderates,” Democrat and Republican, are doing their local media. The battles royal in Congress were basically grandstanding and individual maneuvering for minor advantage around a program with broad support The actual votes were close only because a number of Democrats from conservative areas voted no, but would have made deals with the leadership to go yes if it were needed.

Austerity Blues

Of course, austerity is the last thing the U.S. economy needs. Whatever capitalism’s deeper structural crisis, troubles once again are manifesting themselves in the vicious cycle of “under consumption.” As plants close, as wages are forced down, as workers are bludgeoned into concessions, demand drops. As demand drops, companies lay off and cut wage costs. Now, with government also jettisoning workers, demand, investment and private hiring will likely drop further.

In the budget package spending precedes cutting. Should economic troubles worsen separate appropriations for a jobs program could pass the Congress. But the budget does limit room to maneuver, Clinton has set the baseline and Clinton is cutting spending in a recession, risky to say the least.

II. Spurring Investment

Clinton senses trouble. On a July barnstorming trip for his program, he plead: “You can cut all the spending you want, and if people don’t have jobs and they aren’t earning money, we’re still not going to be able to balance the budget” During the campaign Clinton, and the many Keynesians in his company, urged big infrastructure spending as powerful stimulus.

So why did they abandon their campaign program? Why are they cutting spending in a stagnant and troubled economy? Because they have little choice and it’s probably their best gamble. Assume Clinton in fact proposed and the Congress enacted a vast stimulus package—a huge jobs program, dramatically increased taxes on the rich and even bigger deficits. Interest rates would shoot up. Imports would shoot in. The dollar would fall and inflation rise. The controlled drift down of the dollar that Clinton is now encouraging would become a cataclysmic drop as speculators attacked, ultimately weakening the dollar as the international unit of exchange, further depressing its value. Capital would flee, investment go down. And Clinton, like Mitterrand in the1980s, could stop the decline only by adopting neoliberal policies.

With the big stimulus strategy a no-go from the start, the Clintonites made their gamble on low interest rates through deficit cutting as salvation. And they may have come to believe their propaganda: That deficit cutting will spur jobs and investment That public borrowing has absorbed wealth which would have become private job creating investment And, more plausibly, that deficit cutting will lower interest rates and thus spur investment and big ticket consumption.

In public appearances, Clinton and Bentsen reiterate you may pay a bit more in taxes, but you will save more than that in interest rates.” But Clinton’s real sell is directed to the business elite whom he courted in the campaign and continues to make every effort to satisfy.

For good reason, because his presidency, like any politician’s fate, depends on whether they’ll invest and whether they’ll invest here. Clinton knows full well that politicians who fail to deliver a good “business climate” discover that investment stops (capital strike) and wealth flees to more lucrative places (capital flight). The economy then declines, the people get restive, and the government falls. Clinton’s proposal for investment tax credits, his tough talk on trade, his industrial policy gifts to various industries and especially his campaign to lower interest rates are all part of his good business climate and investment strategy.

Interest rates have taken the central role. He’s not merely cultivating Alan Greenspan, head of the Federal Reserve (it controls short term interest rates). He’s also desperately trying to satisfy the bond markets, national and international, which, because they raise rates at the merest whiff of stimulation or inflation, means demonstrating his commitment to austerity.

Thus, Clinton’s early “stimulus package” was a sham consisting mostly of pieces that would have been enacted in separate legislation (a rise in unemployment benefits, vaccination programs, highway building, etc.). Pegged at an insignificant $18 billion, it couldn’t have been better designed to demonstrate to financial markets they had nothing to feat To be sure the cities could have used its summer jobs money, some was appropriated later Essentially, though, the package represented a substitute for a real stimulus. As the New York Times found curious, the Clinton White House hardly even fought for it, letting Republicans filibuster it to death. The legacy of the internationalization of finance and the deregulation of financial markets since 1972 is that national leaders are hard pressed to implement reflationary policies. No nation can unilaterally stimulate, and Clinton never really tried.

Low Interest Rates Are Not Enough

But none of the investment incentives, low interest rates included, will appreciably increase investment Because regardless of interest rates, regardless of marginal incentives, capital will not invest without expectations of making sales, without a growing and stable market And there’s so much excess productive capacity around the world, it would require a real boom to generate appreciable extra investment.

Still, Clinton’s preoccupation with interest rates is not just magical thinking (inventing something to believe in when there seems no real escape from a painful situation). Although low interest rates won’t by themselves generate much additional investment, a steep rise in rates could kill him.

Capitalist politicians and state managers are in a terrible bind. The financial markets will not permit a stimulatory economic policy. And, whenever the economy appears to be improving, financial authorities put on the brakes by raising rates. With global economic arrangements creating such pressures for deflation and recession, merely making the United States more competitive won’t help much, which the Clintonites are coming to recognize.

They thus have two broad goals in international negotiation: First, having been forced to run a deflationary budget, Clinton has to look for stimulus from the outside. Second, he has to broker a deal to revise international economic arrangements so that expansion at home is not subverted by the international money markets. Ultimately, considerable reregulation of finance and banking, national and international, permitting coordinated stimulatory policies, is key to the possibility of economic revival. Bush made some half-hearted efforts in these directions; Clinton is trying harder.

III. International Economic Policy

While it got no headlines, Nicholas Brady, Bush’s Treasury Secretary, proposed an official G-7 examination of global capital flows, their size and movements. This was a warning to international currency traders, for it is the necessary first step in developing regulatory policy (perhaps stiffer margin requirements on banks, taxes on short term turnover, or direct capital controls). More publicly Brady begged and urged the Europeans and Japanese to start stimulating their economies.

Brady got nowhere. His pleas were met: “Sorry, with the U.S. running huge deficits, global stimulation risks inflation.” The implicit idea was that if the United States got its house in order, then not only would international stimulation go on the agenda, but new financial arrangements could be discussed.

At the Tokyo G-7 economic summit in July’93 Clinton tried to call their bluff. With his austerity budget in hand, Clinton pushed hard demanding they keep their implied promise. The final hyped and meaningless declaration had the usual exhortations for coordinated action to boost global growth but offered no specifics. Clinton did, however, get them to agree to come to Washington this fall for a lobs summit”—”to explore the causes of stubbornly high unemployment” and to rally support for “new and different directions.” This is a lot of show; it might be partly real.

Here’s the Clinton Administration’s wish list:

1. They want agreements to coordinate international stimulation. This would primarily involve Germany lowering interest rates and Japan adopting a stimulatory job creating budget It would also include more debt forgiveness for the Third World and considerable lending to Eastern Europe and the states of the ex- Soviet Union.

2. They want deals to coordinate policy to keep interest rates low and stable across the globe, including banking controls internationally coordinated.

3. They want liberalized and fair trade, to expand international markets for U.S. goods, and especially to ameliorate the trade imbalance between the United States and Japan.

4. And they want agreements to tame the international monetary system, which now generates speculative runs against any country fool enough to attempt stimulation. This would require stabilizing exchange rates and controlling purely speculative transactions.

Clinton could generate some movement toward these goals. With the G-7 facing many intertwined issues, there is considerable room for deals and compromises involving trade, monetary policy, reflation, and the international economic order. Washington has been letting the value of the dollar drop, thus supporting U.S. manufacturing and exports. Washington has also been barking and threatening on trade. This all puts pressure on the Europeans and Japanese to come to the table with ideas and agree to some deals.

These will be protracted negotiations—this summer and continuing—with unpredictable outcomes. The signals from Europe and Japan are mixed. While the Bundesbank and other European central bankers, including those in the once social democratic countries, are still advocating “free markets,” tight money, lower taxes and cutbacks in the social wage (the neoliberal deflationary program), the politicians are worried. The central bankers and politicians have fought back against international currency speculators. Having so far lost the major battles, public economic managers may be ready to create an international front to take them on. And with economic performance so poor everywhere, the romance of deregulation, especially of finance, may be fading. On the other hand, all the big interests are pushing for removal of barriers on “service” exports, including financial services, which could interfere with moves towards reregulation of world financial markets.

It’s hardly likely but conceivable that leadership from Washington could galvanize new policy, though never underestimate the power of profiteers to maintain their scams. In any event, Clinton will make the effort, some change is possible, and movement may be visible by the fall “job summit.”

IV. A High Tech Industrial Policy

Like his austerity budget, Clinton’s “industrial policy” is also being enacted with little real opposition, and in nearly all its aspects: education and training, research and development, industrial and technological incubation, government/industry consortia, conversion, labor/management cooperation.

In the early ’80s, when the free marketeers were in their glory, it was sacrilege to discuss the public role in economic development. Conventional wisdom has made an about face; now all agree that the United States has and must improve its “industrial policy” It’s not just that the state is involved in all markets and commercial arrangements, particularly trade; not just that it has deliberately over the years facilitated economic development in myriad ways (education, training, infrastructure, tax preferences, etc.); but also that, mostly through the Pentagon, it has intentionally fostered industries and technologies (aerospace and computers, for example).

The issue now is not whether to have an industrial policy but what kind. Current arrangements are likened to a “brain-damaged octopus” furiously acting but with no rhyme or reason. Clinton technocrats relish the challenge to do it better, to get rational and strategic. Full up with technocratic hubris, they think they can rebuild the U.S. technological, educational, productive and competitive position.

In developing their plans the Clinton brain trust had a choice. Ann Markusen has advocated a “technology policy that de-emphasizes defense and focuses on the environment, public health, and community stability.” She warns against continuation of a narrowly conceived “military/high-tech agenda.” Though Markusen was invited to Clinton’s pre-inaugural economic summit in Little Rock, her program for technology incubation and conversion was ignored.

As in other areas, the Clinton program has considerable continuity with the high technology and competitiveness goals that Bush and the Democratic Congress had already initiated. While Bush himself steadfastly resisted acknowledging an “industrial policy,” the Omnibus Trade and Competitiveness Act (1988) put many billions into industrial and technological incubation (not just the boondoggles like the super-collider).

Clinton is basically proposing to slightly adjust the dollars up and make some other cosmetic changes. Thus, for example, the National Institute of Standards and Technology (Commerce Department) which operates “The Advanced Technology Program” (it gives matching grants to industry led research) would have its budget increased from $381 million to $1.2 billion in 1997, part of this funding 100 manufacturing “extension” centers (there are now seven) to disseminate information and help industry modernize.

Clinton would also change federal research priorities (from 40-50% civilian), link public agencies to central data bases ($784 million over four years), subsidize federal laboratories to make joint agreements with private companies ($180 million for four years), and remove the word “defense” from the Defense Advanced Research Projects Agency, though it would remain part of the Pentagon.

As to K-12 education, Clinton adapted Bush’s program for national standards and has “bipartisan” support And Clinton’s vocational and “school-to-work transition” programming will also sail through, though with little money behind it Clinton’s campaign program, to require industry to spend 1% of its gross on training, or pay it in taxes, has been shelved by industry opposition.

Within policy circles there is virtually no opposition to labor/management cooperation, not particularly from the AFL-CIO, who will agree to nearly anything in return for support of their bill banning permanent replacement workers during strikes (even if amended with compulsory arbitration). And training workers displaced from military closings or industrial restructuring enjoys wide support, even if no jobs are available. Rhetoric about education and training are in fact a substitute for meaningful economic action.

At Best a Minor Jobs Program

There’s now an elite consensus for a more activist government and industrial policy (part of it of course the pigs going to the trough, part recognition of the failures of laissez faire). The Republicans can truthfully say that it’s an extension of what we were already doing in the Bush administration. Congressmen like it for the same reason it appeals to Clinton: because even if the super conducting super collider bit the dust, high tech this and that and technological retraining has a magic ring, like it might really make us more competitive; to the folks back home it seems like they’re doing something. And though it’s not a whole lot of money, still most of it is good pork that can be doled to industries and universities in each Congressional district. Even militant free marketeers who attack the programs will be sure to get some of the money for their districts.

Pork can be nourishing when the work is good at decent pay and the products useful. This pork is mostly gristle. For all the hype, Clinton’s industrial policy amounts to meager public welfare for selected companies and a minor jobs program for scientists, technicians, and associated help. It just isn’t enough money to be a stimulus, it will not “grow the economy,” and the jobs will not go to those who need them most, though any source of jobs is to be supported.

As to its proclaimed goals, more education, research, technology, invention will likely make little real economic difference and much of it could wreak harm. After all, our problems have nothing to do with alleged educational inadequacy, insufficient training, lack of technological innovation or adversarial labor relations. When the Germans and Japanese put state-of-the-art factories in rural Tennessee and Kentucky, not areas reputed for educational excellence, they find workers perfectly ready to make world-class products. And U.S. scientific, technological and cultural workers are unequalled in invention and creativity.

Working-class wages have fallen for the past twenty years despite spectacular technological advance (computers, automated production, amazing chemical, medical, agricultural, metallurgical, and electronic stuff). Why would even faster circuits, higher definition TV, tougher longer lasting sweeter tomatoes, more efficient solar cells, more medical technology make much difference? And since there’s excess capacity in every manufactured product, if every defense plant were converted to make trucks, civilian aircraft or other capital or consumer goods, it would just mean that all sorts of other efficient plants would close down, as General Motors and many others are now doing. As for training, we already have a vast excess of skilled workers; where will all the high paid jobs come from?

Indeed, not only is industrial policy not the answer, much of it will exacerbate problems. When new technique is introduced to excess workers, or to hire people for less, or to ease the move overseas, the fancy new stuff exacerbates the underlying cycle of under consumption, as it has for the past twenty years. More vocational education, longer school days, more rigid curriculum—imitating Japanese and continental methods—if anything will lead to more drop-out and in time undermine the creativity and ingenuity of U.S. workers. And the primary effect of labor/management cooperation is speedup and downsizing, intensifying the vicious cycle of declining wages, demand, and investment.

To be sure, if U.S. business got better at translating invention into products for sale instead of mostly selling patents to others, and if even more fancy stuff were devised here, the United States would be a bit better off in international competition. But Clinton’s version of industrial policy doesn’t address the fundamental economic problem, and is in fact profoundly misleading, drawing attention from the real sources of decline.

In a country and world with a vast surplus of skills, knowledge, technique, productive facilities and capital, increasing the supply of any of the elements can make little difference. The economic challenge is to create a healthy articulation of all the elements in a regime of steady environmentally sustainable growth.

Can Clinton’s Whole Package Work?

Clinton has troubles Certainly, healthy economic revival seems remote. Because the underlying dynamic is unchanged. Because the fundamental causes of slow and unbalanced growth, weak investment but furious paper shuffling, growing income disparities, and social decay will be untouched. International competition will likely accelerate and the need to squeeze out more profit will continue. A glut of goods and an excess of productive capacity will continue to depress investment and employment Capital is highly mobile and organized, while an international labor thrust would require cooperation and coordination by national labor federations, all near moribund. The vicious cycle of declining working class wages, insufficient demand, and weak investment is firmly implanted.

But this is not the 1930s The economy has grown some even in bad years, and this is a very rich country with a vast productive base and extensive entrepreneurial dynamism. Since 1973, in these last twenty lean years (for workers), the economy has grown nearly 50%, and the U.S. was rich then. Even small positive changes in employment and income can make a great difference.

So while Clintonism isn’t likely to achieve the growth rates of the golden period, could the Clinton package, in Clinton’s fourth year, boost growth maybe as little as a half of 1%, sufficient to reelect him? Surely, his aim is to parlay the following pieces of his economic strategy into economic upturn: (1) jawboning (urging and inducing industry and banks into an investment and growth coalition), (2) keeping interest rates low (low rates will not spur huge capital investment but they will make homes more affordable for moderate income families), (3) goosing some the world economy (which could compensate for domestic deficit cuts, if any), (4) forcing advantageous trade arrangements and boosting exports, (5) winning some marginal gains like rationalizing health care costs and other benefits, (6) more productive spending of Pentagon money.

This could generate enough economic activity before any deficit reduction kicks in to produce sufficient growth and forward momentum to get him reelected, especially in a three way race (Clinton, Perot, and Kemp(Bennett/Weld/Dole/Whoever). It’s not a bad bet for Clinton.

Politics for a Left

Crystal balls are notoriously cloudy. The best guess for the next period is continued stagnation/recomposition and trouble for Clinton in ‘%. Nearly anything is possible: Perhaps severe recession, disintegration, early manifestations of economic/ecological collapse. Perhaps the beginnings of a generalized recovery of world capitalism, a new international growth regime, with historians anointing Clinton this generation’s Roosevelt

But whatever the long term trajectory of world capitalism, for the remainder of this century this country will generally continue as now: growing disparities of income; the immiseration and isolation of the lower sectors of the working class; deepening ecological threats and fears; a hunger for community and democracy that advanced capitalism’s consumer culture can pique but not satisfy; and popular distrust of the entire elite, politicians especially.

What can a left do? Always the task is to activate people and build forces by working in the range of popular movements. But activism and enthusiasm easily wane and become cynicism and withdrawal. People drop out when they feel betrayed by reform politicians like Clinton unless they come to recognize the constraints on reform and the combination program/movement needed to win.

Thus a left must demonstrate that simple populism will not bring reform. That Clinton’s was not a failure of nerve, courage or ideas. That winning political office without the popular base that could overcome elite opposition to sweeping economic change inevitably leads to the compromise and maneuvering that’s Clinton’s only strategy. That even the most committed resolute leadership would be helpless without a powerful movement recognizing the need for control of investment and finance. A movement with those understandings might then take action in the face of capital strike, flight, and other resistance.

It would be a great step forward if those on the left disappointed with Clinton knew why even reform is so tough and what it would take.

September-October 1993, ATC 46