Against the Current, No. 14, May/June 1988

-

From Locked Out to Locked In?

— The Editors -

Our Heroes, As We See Them

— Sol Saporta -

Eyewitness to the Palestinian Uprising

— an interview with Marty Rosenbluth -

Latin American Women: "We're All Feminists"

— Joanne Rappaport -

Chile in 2000: The Generals' Blueprint

— James Petras -

Revolutionaries in the 1950s

— Tim Wohlforth -

Victor Serge's Critique of Stalinism, Part II

— Suzi Weissman -

Random Shots: The Bones Break, the Clubs Hold

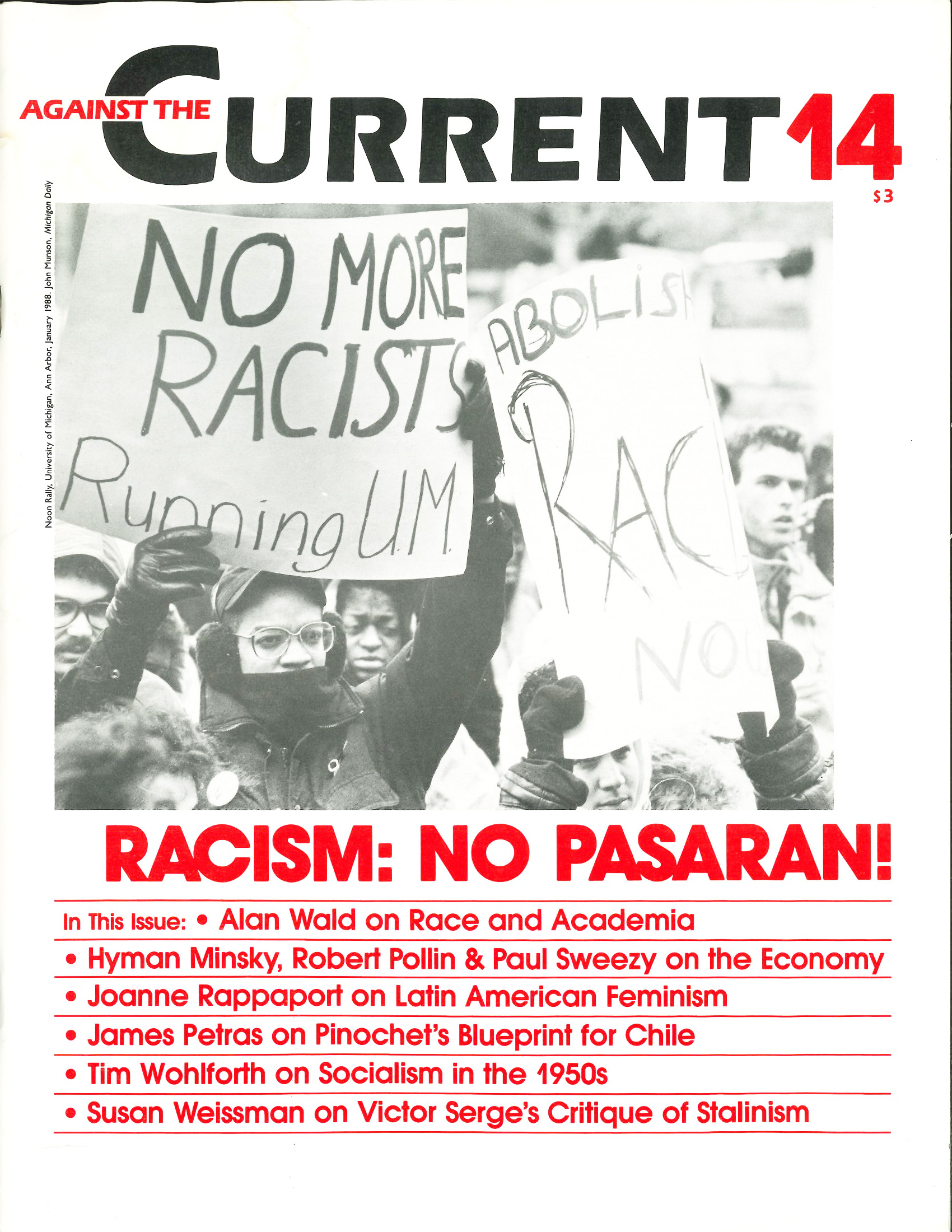

— R.F. Kampfer - Resisting the New Racism

-

Racism and the University

— Alan Wald -

South Africa's Media Scam

— Dianne Feeley - The Economy & the Crash

-

After the Crash: A New Stage?

— Frank Thompson -

Accumulation Leads to Crisis

— Paul Sweezy -

Who's Been on a Binge?

— Robert Pollin -

In a World of Uncertainty

— Hyman P. Minsky - Review

-

What Makes Things Change?

— Tony Smith - Dialogue

-

Against Radical Mythology

— Peter Drucker -

The Power of Radical Religion

— Ken Todd - Letters to the Editors

-

Clarify Palestinian Self-Determination

— Charlie Post -

Market Socialism through Socialist Feminist Analysis

— Ilene Winkler

Robert Pollin

THE QUESTION IS: What does the Wall Street crash mean? I want to begin by considering some alternative perspectives.

Much of the discussion following Oct. 19 has focused on problems within Wall Street itself. This we could call the “Wall Street mess” school of thought. The two types of “messes” to which this approach refers are by now familiar:

First, the emergence of computerdriven, high-tech/no-thought trading practices, which greatly exaggerated the initial stock-market downturn on Oct.19, through automatic sales once a threshold low point was reached.

Second, the erosion of traditional ethical and business values on Wall Street–the ascendance, in other words, of the ruthless red-suspendered yuppies, as portrayed by Michael Douglas in Oliver Stone’s new film, and the decline of the Hal Holbrooks, the old-fashioned Wall Street mavens who understood the imperative of discreet greed and the priority of getting to the golf course by three.

This Wall-Street-mess perspective is consistent with Ronald Reagan’s post-crash pronouncement that “the fundamentals of the economy are sound.” All that is really needed, from this view, is to shutoff the computers and teach the yuppies humility. The invisible hand will take care of the rest.

A leading approach, perhaps the predominant view, is what we may call “the party’s over” school of thought. This approach does recognize serious structural problems in the U.S. economy. These structural problems, as the mantra goes, are the trade deficit, budget deficit and, most fundamentally, the all-embracing “consumption binge.”

Whose Binge?

The consumption binge, in which Americans are said to have borrowed excessively, spent extravagantly and saved little, is the underlying factor here. If Americans had spent less, borrowed less and saved more, the deficits would have been manageable and the financial structure more robust.

On Oct 19, this argument goes, we received a first warning–a “mild heart attack” is the common analogy-and it should be clear that we now have to tighten our belts and mend our ways. A balanced federal budget, a much cheaper dollar and a general call for austerity are the major remedies prescribed.

This argument has broad support among leading journalists and economists, and not only among conservatives such as Martin Feldstein. Indeed, this view seems to be most passionately embraced by analysts within the moderate to liberal range of the spectrum-James Reston, I.F. Stone, Lawrence Summers and the current Nobel laureate Robert Solow.

After his Nobel Prize selection was announced, Solow warned in a Wall Street Journal interview of the inevitable painful times ahead: more taxes, less government spending and stagnant or falling real wages. Stone, long a venerated figure on the left, is even more assertive, writing in The Nation that the United States now needs a strong dose of International Monetary Fund-type austerity, the same medicine that, in his view, was so effective in Latin America.

The merit of the-party’s-over approach is that it does recognize structural problems in the economy. The error here is that it has deeply misperceived the nature of the structural problems; and its solution to the crisis-balanced budgets and austerity-reflect this misperception.

The first basic error of this approach is its undiscriminating rhetoric about “consumption binges.” This ignores the crucial fact that for the majority of Americans, there has been no consumption binge.

Rather, as is well known, average real wages and household incomes have fallen sharply since their peaks in the early 1970s–wages by 14.1% and household incomes by 4.9% between 1973 and 1985. At the same time, the median cost of a new home has risen by 7.4%.

It is true that most U.S. households have increased their dependency on debt financing over this period. But the reason they have done so is not to finance profligate spending, but rather to try to prevent sharp declines in their living standards in the face of rising housing costs and declining real incomes.

In short, the majority of households-roughly all but the top15% of the income distribution-have increased what Martin Wolfson calls “necessitous demand” for credit. This 85% of U.S. households were never invited to any “party,” so why are they now being asked to leave?

A second, related error in the-party’s-over approach is that it ignores the underlying stagnation in the accumulation process within all advanced capitalist countries that leftist economists have been carefully documenting and analyzing for years.

The Long Decline

We can observe the prolonged stagnation through many indicators: for example, the rise in trend unemployment rates and the declines in trend growth rates of industrial production, capacity utilization and the average rate of profitability for nonfinancial corporations. What is the link between these phenomena and the stock-market crash?

To begin with, the decline in corporate profitability since the mid-1960s meant that corporate internal funds were also declining. In order for corporations over this period to maintain competitive levels of expenditure, they were forced to increase their rate of debt financing-the increasing reliance on external funds thus substituting partially for the diminished supply of internal funds. Analognus to households then, corporations turned increasingly to necessitous credit demand as profitability declined.

The long decline in average corporate profitability was also linked with a comparable decline in stock prices. In real terms, the Standard and Poor’s 500 index by 1981 was more than 50% below its average for 1965.

This behavior of stock prices was, in tum, reflected in the movement over this same period of Tobin’s Q ratio-the market value of firms relative to the replacement cost of their physical assets. The Q ratio declined sharply throughout the 1970s, creating a strong incentive by the early 1980s for a shift in investment funds away from productive spending and toward mergers and takeovers.

The objective bases for the bull market of Aug. 1982-0ct. 1987 were thus in place. That is, given the decline in capacity utilization, corporate profit ability and the Q ratio, it made more sense for the smart investor to spend her money shifting ownership in existing assets rather than creating new assets.

This is why we had a bull market in which stock prices soared while the real economy staggered. Remember also that in real terms, this bull market at its peak in Aug. 1987 was still more than 10% below the yearly average for 1965.

World Debt, World Crisis

The-party’s-over school of thought also ignores some basic facts about internationalization of capital. The internationalization of finance brought us the Latin debt crisis. The crisis is now being perpetuated by the unwillingness of the international creditors’ cartel to accept substantial concessions on loans that will never be repaid, just as Allied governments after the Versailles peace were unwilling to accept concessions on German reparations until it was too late.

The intransigence of the creditors’ cartel has added to the U.S. banking system’s vulnerability, while the Latin people continue to experience punishing austerity. The squeeze on Latin America has also meant the collapse of a formerly crucial export market for U.S. products.

It is further important to note that the IMF/World Bank/creditors’ cartel solution to the Latin crisis–that these economies be restructured into the export-led mold-would, if successfully implemented, only worsen trade problems in the United States.

These then are some of the basic facts about the current U.S. economy that have been relentlessly neglected by Wall-Street-mess theorists and the party’s-over school: facts about stagnation, about internationalization and the links between these and the deepening financial fragility that set the stage for the Wall Street crash.

Once these facts are recognized, it becomes apparent that balanced budgets and austerity are not the solution to our problems. There are clearly many negative aspects to budget deficits and they need to be recognized. To a large extent, they are the product of the massive tax rewards Reaganomics has handed to the rich.

They are also, to a large extent, the product of the real consumption binge in the United States during the 1980s-the binge in military spending.

The deficits are regressive distributionally when the debt is repaid, as tax revenues collected from everyone go to pay rich Americans and foreigners who disproportionately own the government bonds. And they intensify competition in credit markets for loanable funds, thus exerting upward pressure on interest rates and adding to financial instability.

AU of these points are true enough But it also must be recognized that, in the present situation, budget deficits are an indispensable demand booster. The deficit now purchases directly about 4% of our gross national product, and bolsters markets further through multiplier effects.

We cannot eliminate that demand booster now without also inflicting even sharper declines on the incomes of most Americans. If incomes were to fall sharply, this would produce even deeper instability in our financial system, as borrowers would be even less able to service their debts than they are at present.

In short, those who call for austerity and balanced budgets should understand that they are effectively advocating a depression as the solution for our present financial crisis. It is incumbent upon the austerity/balanced-budget proponents to strip away the euphemisms and acknowledge this.

Depressions, of course, are the time-honored method of restoring capitalism to financial health, what Joseph Schumpeter used to call the necessary “good cold douche” for unstable capitalism.

But this austerity solution should also sound familiar to those of us who remember the Vietnam War. It is the logic of ”destroying the economy in order to save it” The job of the left now is to oppose this repellant logic and to develop a progressive, anti-austerity program.

Formulating such a program will not be easy, both because the situation is full of pitfalls–the contradictory effects of budget deficits being only the most obvious example–and because any serious left initiative will be vehemently opposed by all the same interests that brought us Reaganomics.

Nevertheless, the outlines of the program we need are clear enough: We need to guarantee basic needs, including work at decent wages; we need redistribution downward; we need to circumscribe speculation; we need democratic control over large-scale investment spending; we need major concessions if not outright cancellation of Third-World debt; and we need to cut the military.

In my view, such policies would discourage both speculation and necessitous credit demand, stabilize the banking system, stimulate demand from below and raise output. Others will disagree on specifics. But in any case, the task now is to develop and disseminate progressive anti-austerity economics as best we can-dearly, forcefully and without cant or dogma.

May-June 1988, ATC 14