Against the Current, No. 12-13, January-April 1988

-

Occupation in Permanent Crisis

— The Editors -

The Washington Legacy: Council Wars in the Windy City

— Alan Jacobson -

"New Period? A Letter to the Editors

— Steve Downs -

Victor Serge's World and Ours

— Susan Weissman - Clear the Names of the Moscow Trial Victims

-

Random Shots: Potato Head Blues

— R.F. Kampfer - After the Crash

-

Notes on the Crash and Crisis

— Robert Brenner -

Why a Crisis of Profitability?

— Mary Malloy -

Another View of the Economy

— Steve Rose - Market Socialism

-

Market Socialism: An Overview

— David Finkel with Samuel Farber -

The Limits of Socialist Planning

— Leslie Evans -

Legacies of Soviet Planning

— Mel Leiman -

A Matter of Priorities

— Milton Fisk - Memorial Essays

-

Raya Dunayevskaya: Thinker, Fighter, Revolutionary

— Richard Greeman -

Van Heijenoort Remembered

— Alexander Buchman - Reviews

-

A Haymarket Memorial

— Michael Löwy -

Body of Opinion

— Linda A. Rabben -

Radicalism in the Forties

— S.A. Longstaff - In Memoriam

-

Raymond Williams, 1921-1988

— The Editors -

Nora Astorga: ¡Presente!

— The Editors

Mary Malloy

IN THE WEEKS following the Oct. 19 stock-market plunge, many were asking whether the- unprecedented one-day fall in stock values was the harbinger of another 1930s-type depression. Almost all economists agree upon the supposed lessons of that decade: economic depressions are preventable- if the correct economic policies are pursued. In other words, bad policies, rather than the logic of capitalist profitability, are the ultimate cause of economic crisis.

For those outside the upper circles of policymaking, the economists’ consensus is not very reassuring because they are sharply divided over what is the ”correct policy.” At the moment, the “right policy” for the White House is allowing the dollar to tumble against Japanese and German currencies in an effort to-promote U.S. exports. Implied in this cure is that restrictive monetary and fiscal policies abroad are to blame for the current U.S. economic distress and may induce a new global recession.

For a growing number of Republicans, business people and Democrats, the White House prescription is at best wrong and at worst dangerous. According to what is becoming the dominant position within capital and its political representatives, the administration’s attempt to use a falling dollar to force down Japanese and German interest rates and increase U.S. exports is “Kamakazeconomics.” They believe that the real problem is- that the American people have been living beyond their means over the last eight years and now the bills are coming due.

According to this view, the market panicked as the costs of financing the huge federal deficit rose sharply. The market is forcefully announcing the failure of Reagan’s “supply-side” revolution and is crying out for a return to “fiscal responsibility,” that is, across-the-board spending cuts and higher taxes for workers and the middle class.

The Congressional opposition promises that short-run austerity will neutralize destabilizing forces and set the stage for long-term economic growth. Like the Reagan analysis, this view finds the problem and the solution in the arena of capitaliststate economic policies.

The lone voice speaking against balancing the budget is that of the Keynesians. They, like the administration, reject the claim that the federal deficits caused the stock-market tumble. They point out that the deficit fell 33 % in the year preceding the stock market crash. Instead, the restrictive monetary policy that sent interest rates soaring last summer caused the crash. Interest rates must be brought and kept down to spur spending and prevent a recession or possible depression.

Keynesians promise that more public and private debt in the short run will make us financially solvent in the long run. Again the problem and the solution is defined in terms of capitalist state policy.

A Crisis of Profitability

Unfortunately for the bourgeoisie, the bourgeois political prescriptions rest on the erroneous theory that capitalist state policies are both the cause and the cure of the current economic malaise.

What the October market crash really showed the world is just how fragile was the state policy-induced “Reagan boom” of 1982-87. This boom seemed to promise a return to the rapid and sustained growth of the 1950s and 1960s. But underlying it lay a long-term stagnation of accumulation, which the entire capitalist world economy entered in the late 1960s and from which it has yet to emerge.

Every capitalist country has seen higher and higher levels of unemployment, even during the recovery phase of the business cycle; sharpening competition among capitals to preserve or expand shares of a shrinking world market for goods and services; and the displacement of investment from the production of goods and services to the speculation in bonds, stocks and currencies.

This global economic crisis has had similar political effects in all capitalist countries in the 1970s and 1980s. On the one hand, every bourgeoisie has launched an employers’ offensive against labor. Among the ways capital has attempted to lower production costs at the expense of workers have been the speed-up of production, increased part-time work, cuts in wages and fringe benefits and two-tier wage and benefit systems.

On the other hand, every capitalist state has imposed austerity, attempting to place the entire costs of unemployment and social welfare on the individual worker and her/his family.

In fact, all of the major economic problems highlighted in the press-trade dislocations, escalating- public and private debt-are symptoms of the global crisis of capitalist profitability. The causes and significance of the stock-market crash lie in the long-term fall” in the average rate of profit.

The high rates of return on investment capital experienced coming out of the Depression and World War II shaped the postwar boom: high levels of investment and employment, rising real wages and productivity, and balanced international trade and government accounts. Neither chance nor state policies created the fundamental conditions for the postwar expansion.

Profits are created in production, in the relationship between capital and labor. Workers create profits when they produce goods and services in excess of the value of their wages. The ratio of profits to the amount of machinery needed to produce that profit determines the rate of profit — the rate of return of capitalist companies.

Paradoxically, the very health of the system — a high rate of profit spurring strong investment and economic growth — creates the conditions that cause a fall in the rate of profit.

The rate of profit falls for two reasons. First, increasing the amount of machinery in production is the best and most successful means of increasing profit per worker-the difference between the worker’s output and his/her wage. However, increasing the amount of machinery in production lowers the total amount of productive labor-the source of profits. Second, competition insures that capitalists mechanize, lowering the number of productive workers. Together these two factors reduce the total amount of profit and slowly but steadily reduces the rate of profit.1

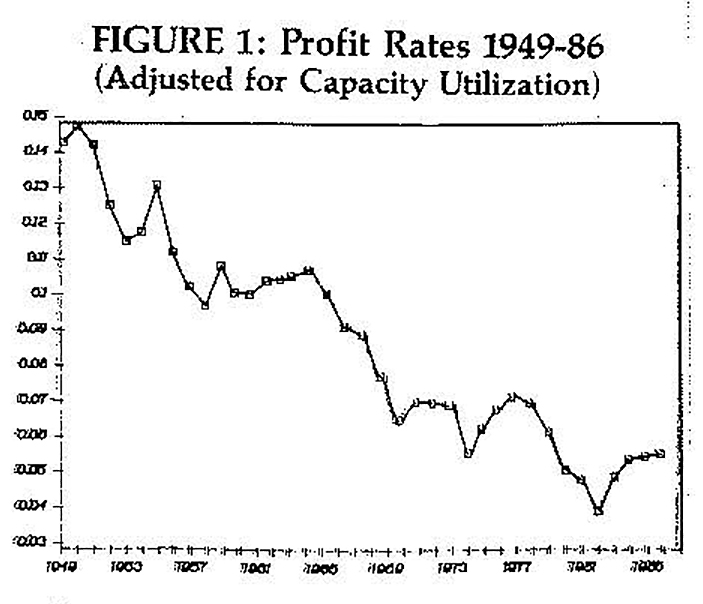

Figure 1 shows the average rate of profit in the United States, adjusted for fluctuations in demand, falling 55 % over the postwar period. In other words, the rate of profit falls in both a period of very strong economic growth (1947-1966) and a period of weak economic growth (1966-1987). This poses the question of what causes a transition from a period of prosperity to a period of stagnation.

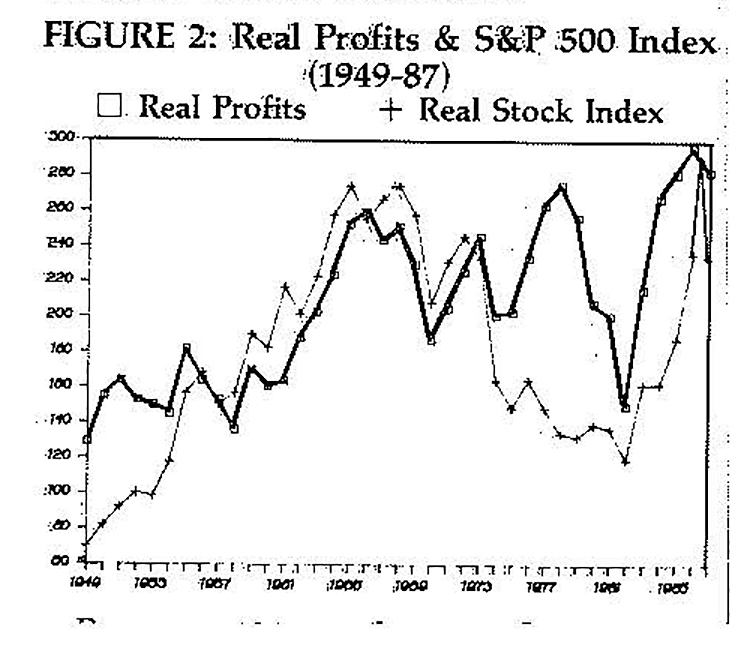

Figure 2 provides the answer. The heavy line charts the movement of total profits in the U.S economy since 1949. From 1949 1968 the total amount of profit grew although the rate of profit was falling. In other words, strong rates of investment compensated for a declining rate of return on that investment.

Between 1966 and 1968, the mass of profit peaks and then flattens out, despite cyclical ups and down. The stagnation of the mass of profit signaled the beginning of a long period of economic stagnation.3

The very health of the capitalist economy in the years prior to 1966 caused the eventual stagnation of total profits. In particular, the exceptionally strong investment and growth during the long business cycle of February 1961 through December 1969 enlarged the amount of machinery in production.

This rapid mechanization accelerated the fall in the rate of profit in the mid-1960s. The total amount of profit could have kept growing only if the rate of investment rose sufficiently to compensate for the fall in the rate of profit.

However, the rate of investment depends primarily on the rate of profit. Thus, the countertendency to a stagnating mass of profit the rate of investment — began to weaken in the late 1960s, ending the post-war boom.

Making Labor Pay

Slow growth, falling real wages, rising unemployment, sharpened international competition and mushrooming government deficits characterized the new phase of capitalist accumulation. Companies decreasing incentive and ability to invest made state policies critical in bolstering the capitalist system.

First, public spending has increasingly supplemented private spending to maintain demand and keep capacity utilization (and with it employment) at acceptable levels. Second, the heightened capitalist competition that came in the wake of the stagnation of the mass of profit forced more and more firms to invest at the moment their internal investment funds were shrinking.

As a result, capitalists had to go into deeper and deeper debt in order to maintain their position vis-a-vis their competitors. Again, the capitalist state played a central role in preventing the collapse of investment through monetary and credit expansion.

Since 1980, the Reagan administration, with complete bipartisan support, has pursued fiscal policies that attempt to take pressure off falling returns and shrinking levels of corporate profits. Accelerated depreciation, reduced corporate income tax rates, and tax credit for research and development promised to reduce costs and spur investment-to bring America back to the golden era of the 1950s and 1960s.

The actual effect of such policies has been to transfer the burden of capitalist debt onto to the backs of middle- and working-class taxpayers. Moreover it appears that such relief for corporations has been shortlived. The ratio of corporate to public debt is again rising, which is not surprising since “Reaganomics” cannot fundamentally alter the conditions of profitability.

Total Profits and Stock Prices

Two interrelated factors generally shape the movement of stock prices. The first is investors’ expectations about corporations’ future profits. The second is the rate of return on stocks compared with bonds and other financial instruments.

Figure 2 shows the effects of both rising and falling total profits on the movement of stock prices. Between 1949 and 1965, stock prices rose, peaking a year before the high point of total profits. Since 1966, stock prices have begun a long-term slide that saw values drop over 56 % between 1965 and the beginning of the bull market in 1982.

By reacting to current, concrete conditions in the bond market (for example, the rate of interest), stock market prices anticipate the future course of corporate profitability. In an expansionary period (1949-66), the upward movement of total corporate profits feeds expectations. A cyclical rise in interest rates may send prices down, but the dips are brief and the recovery in stock prices is robust. Moreover, in normal times such “financial corrections” have little or no effect on production activities because they are merely “early warning signals” of different phases of the business cycle.

Since 1966, however, times have not been normal. The cyclical movements of stock prices and total profits have become sharper-dips have become deeper and the recoveries comparatively less robust. Although profits rose cyclically from their very low levels cluing the 1981-82 recession, their trend has been basically stagnant.

Similarly, investment staged a recovery from its recession low. However, as one analyst put it “climbing off the basement floor is not the same as scaling new heights.” Figure 2 shows that the market had lost over 56% of its value between 1966 and 1982, and only regained its 1966 value in 1987.

What caused the Reagan “bull market”? First, capitalist state monetary and fiscal policy spurred the stock-market boom. The Federal Reserve System eased credit in mid-1982, sharply reducing interest rates from their double-digit high of 1981. Ten-year Treasury securities fell from 14% in 1983 to 7.5% in 1986.

Since 1984 the money supply and credit creation has proceeded rapidly, much faster than the growth of the real economy, generously stoking the fires of stock-price inflation. The “supply-side” promise of increased profits and investment coupled with a growing money supply gave the market much of its upward momentum.

The second factor fueling the “bull market” was the corporate reorganization and restructuring taking place through mergers and acquisitions. Cheap asset prices relative to replacement cost made it more profitable to buy up existing companies than to start new ones.

In addition, the Japanese and German trade surpluses created enormous pools of savings. With declining profitability in Japanese and German production, these funds flowed freely into the purchase of stocks. Finally, supply pressures further inflated stock price as corporate America rushed to buy up its own equity in order to lower its tax burden and repel hostile takeovers in the last two years.

The very expansionary monetary policies that bankrolled the market’s rise could not be sustained in the long run. The 40% fall in the dollar over the last two years required rising interest rates to keep foreigners buying our debt.

Beginning last May, the Federal Reserve began to restrict the money supply. In July and August interest rates on bonds in the United States and. Japan began to rise. This sent a signal to astute money managers, who began their move from stocks into cash-like securities.

It was only a matter of time before all but the die-hard bulls realized that stocks lacked value compared to bonds. In this volatile financial environment, Treasury Secretary Baker’s “talking down the dollar” to force the Germans to cut interest rates was sufficient to spark a massive sell off on Wall Street.

Where Will the Economy Go?

The panic on Wall Street is the latest visible reminder of the enduring crisis of profitability, a crisis which has yet to be resolved. It is also an early warning signal of — but not the cause of — the weakening of the Reagan boom and the beginning of a severe recession.

While most economists rightly point out that a fall in stock prices do not always foretell a recession, such statements do not distinguish between mild corrections and a crash. Since 1885 there have been eleven cases where stock prices fell by 30% or more. In every case the economy entered a recession or depression. From its August high to its October low stock prices fell by over 36%. Finally, the panic exposes the increasing inability of capitalist-state economic policies to prevent the transformation of a severe recession into a full-scale depression.

On the surface, the panic appeared to be the result of a restrictive monetary policy. At a deeper level the crash can be likened to the convulsions of a terminally ill patient as the life-support system is removed. When the convulsions got too violent, the patient was hooked up again-no one wants to be responsible for the death.

Short of another a sharp dive in the stock market, a pronounced qualitative change in business activity, or the bankruptcy of a major bank or Third World country, no new bold policy initiatives will be launched from now until the elections next year.

The White House will continue to bet on a falling dollar as the only means of prolonging the flagging boom through the expansion of exports. Export demand, however, lacks the economic breath of domestic consumer spending, the real locomotive of the Reagan boom.

As long as the Dow hovers around the 1900 level and the economy maintains its acceptable but unexciting levels, Washington will continue its easy money policy. However, four years of these politics laid the groundwork for the panic.

The Federal Reserve is walking a tightrope: it must keep rates high enough to fund the Federal debt, but low enough to encourage domestic borrowing and spending.

Of course, the Federal Reserve could print money and buy the Federal debt. As appealing as this solution may appear, it would be an admission of the fiscal bankruptcy of the capitalist state. In addition, a monetarization of the debt would severely limit the Federal Reserve System’s ability to affect the course of the unavoidable recession.

If the Democrats are elected next November, they will have an opportunity to implement their program of fiscal austerity: higher taxes on the working class and sharp reductions in spending to “balance the budget.” Clearly, these restrictive fiscal and monetary policies will not prevent, but will rather hasten the arrival of the unavoidable cyclical downturn of accumulation. If the Democrats continue to pursue these state policies once the recession begins, they will only accelerate the restriction of demand and deepen the recession.

In sum, neither the causes nor the cure for the current capitalist economic crisis is found in state policy. In fact, all of the capitalist state policies pursued over the last twenty years-either welfare or war fare Keynesianism-have only prolonged the crisis.

Although capitalist state policy has avoided the political and social dangers of an economic collapse, it also has pre&vented the restoration of profitability. A depression, by intensifying attacks on working and living standards and eliminating the least efficient capitalist firms, is the necessary precondition of a new period of capitalist expansion.

While a depression may be economically necessary for a new capitalist prosperity, capital seeks to avoid it because a depression intensifies class and social struggles-struggles whose outcome is not predetermined economically.

Instead, the relative political organization and strength of the contending class and social forces will determine the out come of these struggles, a prospect that poses many challenges to the U.S. left.

Footnotes

1. For a more detailed presentation of this analysis, see A Shaikh, The Current World Economic Crisis (Detroit: Against the Current Pamphlet).

2. Figure 1: Rate of Profit (P/K), where P = Corporate Profits IVA and CCA, Economic Report of the President, 1987 [hereinafter ERP, 19871, Table B84, Column 1, p. 351. K = Fixed, Non-Residential, Non-Agricultural Capital Stock, Office of Business Economics, Department of Commerce. For a detailed explanation of sources and derivation, see Shaikh, Current Crisis.

3. Figure 2: Real Profits, 1949-1986, Nominal Profits deflated by implicit price deflator for total private domestic investment, ERP, 1987,> Table B3, p. 248. Real Profits, 1986-Third Quarter 1987, Survey of Current Business [hereinafter, SCB], October 198Z Real Standard and Poors Composite Stock Index, 1949-1986, ERP, 1987, Table B-91, p. 350. Real Standard and Poors Composite Stock Index, January 1986-December 1987, Daily Close, Data Resources Inc. All deflated by the same index used above, SCB, October 1987.

January-April 1988, AT 12-13