Against the Current, No. 2, March/April 1986

-

A Letter from the Editors

— The Editors -

The Deep Roots of U.S. Economic Decline

— Robert Brenner -

Summit Politics & the Third World

— James Petras -

COSATU: New Trend Emerges in South Africa Freedom Struggle

— Sandy Boyer & Dianne Feeley - COSATU Women's Resolution

-

Out of Africa: Isak Dinesen's Colonial Pastoral

— Christy Brown -

Random Shots: The Little Sect that Time Forgot

— R.F. Kampfer -

Letter re Theories

— Edward Joahn - Labor's War at Home

-

Teachers, Parents Win in Oakland

— Laurie Goldsmith -

Columbia University: Birth of a Union

— Lynn Geron -

The Long Battle of Watsonville

— Frank Bardacke -

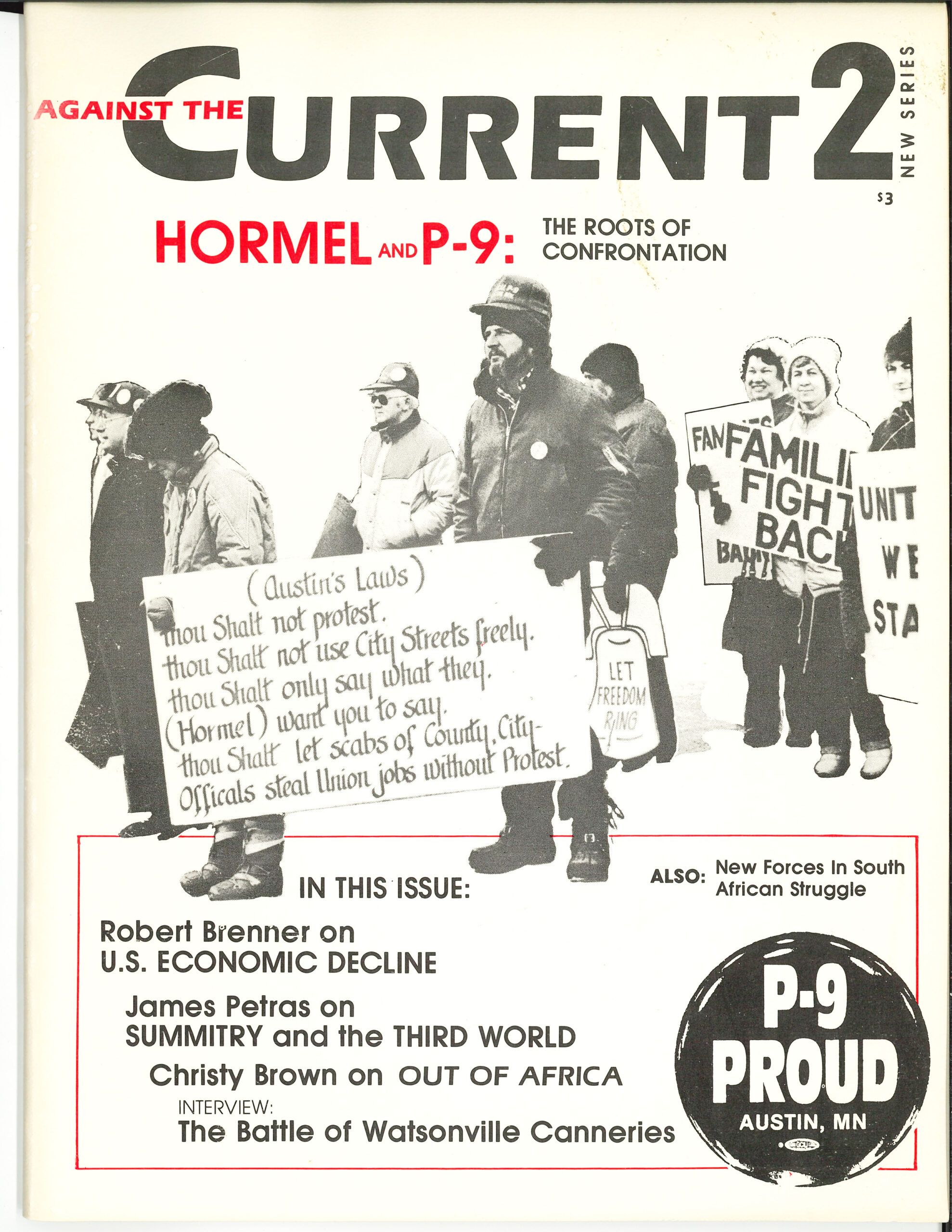

Behind the Hormel Strike: Fifty Years of P-9

— Roger Horowitz - A Striking Family's Story

-

Austin Rally

— Roger Horowitz

Robert Brenner

RONALD REAGAN’s landslide electoral victory gave the appearance of completing an already definitive shift to the right in U.S. politics. But this appearance is in important respects deceiving. There are unquestionably strong pressures within U.S. society pushing wide sections of the population, not only the elites but parts of the working class, toward the right. But the political right has by no means consolidated power.

A little more than a year after his election, Reagan and his administration have already dissipated the political momentum they originally derived from his landslide victory. The administration has been increasingly unable to frame-let alone get passed-a consistent policy on taxes and spending. It has already seen its plans for increasing military expenditures, cutting social spending, and reforming the tax system come under attack, not only by a disorganized Democratic Party opposition, but by large sections of the Republican Party as well. Meanwhile, record federal budget and trade deficits threaten to increase explosively and to swamp the entire economy.

The thesis of this essay is that this crisis of policy, and indeed of U.S. politics more generally, will not soon be resolved. This is because the relative decline of U.S. industry, the increased involvement of U.S. capitalists in finance and in business overseas, and the radically stepped up commitment of capitalism in general to manufacturing in parts of the Third World-in the context of the deepening long-term international capitalist crisis-have made it next to impossible for any U.S. government to frame programs which are not politically and economically self-destructive.

Now it must be emphasized that standing behind U.S. industrial decline and profoundly affecting its course has been the crisis of the entire world economy. For well over a decade the world crisis has meant, just about everywhere, rates of profit, of economic growth and of productivity increase which are in absolute terms substantially lower than were those of the 1950s and 1960s, along with progressively more severe cyclical downturns with ever-increasing levels of unemployment.

The crisis has in consequence drastically reduced the political options of both capitalists and governing parties throughout the world, determining certain political trends which have been common to all the capitalist economies, including the U.S.: above all, the application of an ever more vicious employers’ offensive against the working class, accompanied by the implementation of increasingly thorough programs of austerity by conservative and social democratic governments alike.(0)

But, as I shall argue, the key to the distinctive trajectory of U.S. politics in the later 1970s and 1980s is to be found in the long-term relative decline of both the competitiveness of U.S. manufacturing and the attractiveness of U.S. manufacturing as a field for investment.

It is the declining attractiveness of U.S. manufacturing as a field for investment, the increasing involvement of U.S. capitalists in finance and overseas business (especially lending), and the shift of capitalist manufacturing to parts of the Third World which are peculiarly responsible for what seem to be the decisive features of the present political conjuncture in the U.S.

These are (1) the continuing failure of the U.S. government to adopt any sort of program or plan to encourage or renew U.S. manufacturing, despite the continuing refusal of U.S. capitalists to make sufficient investments in new plant and equipment in U.S. industry to sustain its competitiveness; (2) a big step up in U.S. political-military intervention throughout the world, especially in the newly-developing regions, designed to protect the increased commitment of U.S. capital and capitalism in general in the Third World; and (3) an unprecedented growth in peacetime military spending, originally motivated by the requirement of growing imperial commitments, but also functioning today, in Keynesian fashion through the federal deficit, as the main instrument for maintaining international economic stability in the face of the increasingly severe ups and downs of the business cycle.

For the foreseeable future, any U.S. government, Republican or Democrat, will continue these policies, for they offer the most promising means available for securing the profitability of U.S. capital and the stability of capitalism as a whole — although these policies will only exacerbate the long-term failure of productive investment in U.S. industry and introduce new sources of short-term economic instability, while spelling disaster for the welfare of U.S. working people.

The first part of this essay will offer an account of the long-term relative decline of U.S. manufacturing. I shall try to describe the contours, to analyze the causes, and then to bring out the economic effects of declining competitiveness by tracing the historical course of manufacturing decline through the successive phases of the postwar world economy, from boom to crisis. In the second part, to appear in the next issue of this journal, I shall try to show how declining industrial competitiveness has shaped the recent course of U.S. politics, providing one important key to the contradictions of ruling class policy since the early 1970s, as well as to the colconclude by examining the implications of U.S. industrial decline for the strategy of the left, the opportunities offered and the dangers posed.

I. U.S. Decline in The International Economy

The U.S. emerged from World War II totally dominant within the international economy-the most powerful technologically, the least devastated by war, and possessing the political power to dictate the terms of the postwar international economic order. Nevertheless, from the late 1950s at the latest, the U.S. economy experienced a pattern of relatively slow growth of its productive forces, leading to the long-term erosion of its position of economic dominance. Over time, U.S. manufacturing became progressively less able to compete on the international market, and U.S. industry became relatively less and less attractive as a field for investment.

The key to the decline of manufacturing in the U.S. is the relative failure of investment. Over the entire postwar period, the U.S. economy has devoted a much smaller part of its total annual output to investment in fixed capital than have its competitors-about half as much as Japan, about two-thirds as much as Germany and France. It also has annually increased its fixed capital at a much lower rate than have its main competitors-less than half as fast as have the Japanese, perhaps two-thirds as fast as have the French and Germans. Because the U.S. economy has thus provided its workers with plant and equipment (fixed capital) so much more slowly than have its competitors over such an extended period-well over a quarter of a century-the U.S. economy also has had much lower rates of growth of industrial productivity than its competitors have had.

Over the period 1950-1975, the annual average increase in industrial productivity was 2.8% in the U.S., as compared to 8.3% in Japan, 5.4% in Germany, and 5.0% in France.(1) In view of the fact that the United States’ main competitors were thus increasing their efficiency so much faster than was the U.S., it naturally did not take long for the U.S. to lose its overwhelming advantage in industrial productiveness. As recently as 1970, measured in terms of output per hour of labor, U.S. manufacturing was still about twice as productive as Japanese manufacturing and a third more productive than that of Germany and France. But by the early 1980s, average output per hour in manufacturing in the U.S. actually trailed that in Germany and France, and was only slightly ahead of that in Japan.(2)

Even this rather decisive turnabout in average manufacturing productiveness fails to give the full picture. While perhaps still slightly behind the U.S. in average hourly output for manufacturing as a whole, Japan manufactures a large number of commodities which are traded on the world market and imported into the U.S. at a far higher level of efficiency than does the U.S.

Steel was perhaps the first really critical industry in which the U.S. lost its edge. In 1958, it took 9 hours to make a ton of hot rolled sheet steel in the U.S., 27 hours in Japan. But by 1980, it took 5.3 hours to make a ton of hot rolled sheet steel in the U.S., but only 4.4 hours in Japan.

A similar major reversal took place next in consumer electronics. Whereas in 1965 it took 7.6 work hours to make a television set in the U.S. and 9 hours in Japan, by 1980 it took 2.6 hours to make a television set in the U.S., 0.8 hours in Japan. The same story could be told in the critically important machine tool industry. As recently as 1975, Japanese machine tool producers were only about 60% as productive as those in the U.S. But, by 1985, Japanese machine tool producers were probably 25 % more productive than those in the U.S.

The reversal which has taken place in machine tools typifies the trend in a whole range of products which require complex multi-staged manufacturing processes, such as watches, cameras, large electric motors, trucks, bulldozers, agricultural tractors, buses and subway cars.

Of course, the most significant transformation has taken place in auto, unquestionably the key industry of the postwar world economy. In 1970, it took about 210 hours to make a car in the U.S., about 260 hours in Japan. But by 1981, while it still took around 210 hours to make a car in the U.S., it took only 140 hours in Japan.(3)

Nor does the U.S. retain its former dominance in the so-called high technology industries. The Japanese totally control the production of such high technology consumer electronics goods as VCRs and the new laser disks, which the U.S. does not produce.

Direct data on the relative productiveness of the U.S. and Japanese semiconductor industries is unavailable. But one can get a pretty clear idea of the trend by noting that although only a short time ago the U.S. monopolized semiconductor memory chip production, by 1985 Japanese producers controlled 60% of the market for 64K RAM chips and 85 % of the market for the new 256K RAM chips, forcing most American companies to drop out of the market. This is a particularly ominous development for U.S. producers, because experience with manufacturing memory chips in high volume probably holds the key to the successful development of the socalled super-chip-where, by means of the massive reduction in size of the integrated circuits, whole computers will be able to fit on a single chip.(4)

The Japanese have also taken the lead in the new line of larger, faster, easier-to-use supercomputers, a field previously totally controlled by the U.S. and IBM. This could have a major effect on the world market in computers, since the use of the new supercomputers is not confined, as in the past, to specialized scientific research; they have an extremely wide application in business and government offices. Perhaps most symptomatic of the trend, the Japanese are today contesting the U.S.’s productive leadership in the brand new, science-based field of commercial biotechnology, the products of which are starting to make a major impact on the drug, food processing, and agricultural industries.(5)

Such examples could be multiplied. But the overt manifestations of declining U.S. competitiveness in manufacturing, a direct effect of declining relative productiveness, are so pervasive as to be obvious to all but academically-trained economists: the big decline in the U.S. share of world exports; the radical growth of the share of manufacturing imports in the U.S. market, including especially high technology imports (which now substantially exceed high technology exports); the record, crisis-level trade deficits; the massive flight of capital abroad, especially in the form of loans; the decay of whole industrial regions, with concomitant loss of jobs; and, above all, the precipitate decline in the standard of living of industrial workers and workers in general.

For a scientific sum up, it is perhaps sufficient to quote the conclusions of the recently published survey of U.S. manufacturing, the Data Resources Inc. Report on U.S. Manufacturing Industries: “The decline of position of manufacturing is a major historical development for this country.” “There are so few exceptions to the decline of the international position of U.S. manufacturing industries that one must seek more general causes that act on the entire economy.”(6)

II. The Causes of Industrial Decline

The question, then, is why the growth of productive power in the U.S. has been so much slower than that of its competitors. I would argue that the forces making for the relative decline of the U.S. manufacturing economy have been structural, and would therefore have been quite difficult to avoid under any circumstances.

Economies which have long been in the lead tend, over time, to find themselves at an increasing productive disadvantage against some of those economies which come late. The very process of capital accumulation puts the economic leader at a short-to-medium run disadvantage with respect to certain key costs and market opportunities; at the same time, it endows at least some of the latecomer economies with certain distinct long-term advantages with respect to the development and use of those increasingly powerful productive techniques and economic institutions which emerge in the course of capitalist evolution.

In consequence, over an extended period it becomes systematically easier and more profitable to make additional capital investments in the latest plant and equipment in the latecomer economy than in the leading economy, and the result is a transformation in the balance of international economic productive power.

The short-to-medium run disadvantages of economic leadership include:

i) Existing Fixed Capital as a Barrier to Further Investment. During the immediate postwar period, the U.S. economy underwent a tremendous renewal, with masses of capital pent up during the Depression and World War II finding an outlet in investment in new plant and equipment across the board. By the late 1950s, however, there had been a significant slowdown in expenditures on new plant and equipment.

But this was not really surprising, for the possession of masses of productive power, “fixed” so to speak in already existing investment, tends in itself to discourage further capital investments at a higher level, at least up to a point. Fixed capital is capital already paid for; it is “sunk” capital. Once a firm has purchased fixed capital, it will attempt to use it for as long as possible. As far as that firm is concerned, the use of the fixed capital is “free” and the only relevant cost is that of the additional, circulating capital needed to employ the fixed capital — that is, the raw materials, the depreciation costs (wear and tear), and the labor.

In contrast, if that firm sought to make use of a new technique which was embodied in new fixed capital (e.g. new machines), it would not only have to make an additional investment in fixed capital, it would lose the use of its already existing fixed capital (which it could have used without additional cost). So long, then, as a firm can make the average rate of profit on its circulating capital, it will continue to use the old, fixed capital, even if there are more advanced techniques which would allow it to produce more efficiently, i.e. at a lower cost and rate of profit, if both fixed and circulating capital were taken into account.

All else being equal, this slows down the introduction of new techniques (at least for a time) in older economies, in comparison to newly-developing ones. For example, at the point at which basic oxygen furnaces became available for steel production sometime during the later 1950s, U.S. producers had already equipped themselves with relatively backward open hearth furnaces, which it only made sense to continue to use, especially given the massive investment which had been required. The result was that the U.S. steel industry failed, for a long time, to adopt the new method.

In contrast, the newly-developing Japanese steel industry, not so burdened by already existing steelproducing capacity, was essentially free to invest in the basic oxygen furnaces, and did so assiduously during the 1960s and 1970s.(7)

ii) The Relatively Greater Profitability in New Lines and New Areas of Production. Already possessed by the 1950s of a huge, recently-constructed modern plant in almost every industry, many U.S. capitalists had little desire further to transform their factories, and were more or less obliged to use them in their given technological state. But this was only one source of the technological inertia in the U.S. economy.

As the other side of the same coin, capitalists who were not burdened with existing equipment and who therefore could theoretically have made use of more advanced techniques to produce at lower costs than did those with already-existing equipment and challenge them in their U.S. markets, nevertheless tended not to do this. This is because, all else being equal, capitalists will place their new investments, if at all possible, in new lines of production and new regions and avoid competing in the markets of already entrenched capitalists, for the obvious reason that those who enter first into new regions and initiate the production of new commodities are able to achieve, at least temporarily, higher than average rates of profit, while those who fight for already-filled markets tend to suffer lower than average rates of profit.

At the end of the 1950s and in the early 1960s, capitalists who wished to bring in the latest equipment in the American market would generally have had to come up against the great corporations in the field. But at that point it made little economic sense to put one’s investment funds into a struggle for already-occupied American markets, because there were vast new fields available for investment.

The economists Baran and Sweezy have seen the great U.S. corporations’ domination of the U.S. market in the late 1950s and early 1960s, and the corresponding stagnation of investment in new plant and equipment in manufacturing in this period, as evidence that these firms held a permanent monopoly, that a new stage of “monopoly capital” had emerged. In reality, however, the “monopoly” exerted by the great corporations over the U.S. home market was a very temporary phenomenon, and, more than anything else, was evidence that the really great opportunities for profit lay elsewhere. This was a fact of which the giant U.S. corporations, perhaps more than anyone else, were acutely aware.

iii) Relatively Cheaper Production in the Newer Economies. The greater opportunities which were emerging at this point were to be found, of course, in Europe and Japan, which enjoyed certain definite advantages over the American economy in relative costs of production simply because they were beginning capital accumulation later in time.

First, investors in these regions could make use of the latest technique, borrowed from the U.S., and could do so without having to come up against well entrenched corporations already possessed of the markets.

Second, these regions had vast pools of cheap labor. This was especially true of Japan and Germany, where first fascism and authoritarianism, then military occupations by the United States, dealt a series of devastating blows to the local labor movements. Not only was the labor available in Germany and Japan cheap, it was also skilled; inexpensive labor could thus be employed without the sacrifice of productive technique which is often necessary to make use of cheap labor.

Third, these regions had vast unfilled markets, especially in comparison to the relatively saturated markets of the U.S. Fourth, although the wartime destruction of industry in Germany and Japan can be exaggerated, by the end of World War II, these regions retained little fixed capital which they could use, for what had not been destroyed was very often obsolete. As a result, investors in Japan and Germany essentially had no choice by to make their new investments at the highest level of technique.

Finally, these economies could protect their home markets without fear of retaliation, while the U.S. was more or less obliged to keep its markets free and open, and to tolerate a certain amount of protection by its competitors. The reason for this was that, if the U.S. wished to be able to export to Europe and Japan, it had to let those regions amass the purchasing power (the currency) to buy U.S. products. The only way to do this was by developing the capacity to export their goods to the U.S.

Over a significant period, then, all else being equal, capitalists investing in latecomer economies have better possibilities than those investing in the leading economy. Nevertheless, all of the aforementioned advantages enjoyed by the late developers over the earlier developers are more or less temporary. As capital accumulation takes its course in the later developing areas, new technologies are embodied in fixed capital and ultimately become obsolete; wages rise as demand for labor grows and the labor force is used up; markets are filled; and it ceases to be possible to implement protection without retaliation.

If those had been the only factors operative, we could have expected the U.S.’s leading competitors, over time, to exhaust their advantages and lose their edge. However, the economic latecomers also enjoy certain long-run advantages which tend to be relatively cumulative and permanent:

i) Institutional Innovation and Technical Change. In the course of capitalist evolution, there is not only a continuing advance in productive technique, but a cumulative advance in what might be called the institutionalized forms of property or economic organization. All else being equal, the economic leader tends to be less well placed to adopt the more highly evolved institutionalized forms of property or economic organization, simply because it has developed through and remains more tied to older, less evolved forms than the latecomer.

From the end of World War II, Japanese firms in particular have operated on the basis of a whole series of institutionalized arrangements. Through these they have been able to achieve powerful competitive advantages over their U.S. counterparts, especially with respect to the capacity to mobilize investment funds cheaply and in great quantities, to speedily reallocate capital, to spread or socialize risk, to gain (at least temporary and partial) protection from competition, to dispose of goods which are critical for capital accumulation but which are relatively difficult to provide effectively on a private profit basis, and above all educated manpower.

These institutions have helped to insure a much closer fit in Japan than in the U.S. between the requirements for increasing productiveness and the requirements for maximizing profits throughout the whole postwar period, and especially in the era of crisis and intensified competition since the start of the 1970s.

Most important, there exists in Japan a very close inter relationship between the banks and horizontally integrated industry, supported by the state. The great Japanese “City banks” thus stand at the core of huge, horizontally integrated industrial groups (keiretsu) containing a large number of enterprises, representing an enormous range of industries. The banks both lend money to the firms in their industrial group and own a significant proportion of their shares, becoming in the process quite knowledgeable about their operations and inextricably tied to their fate. Meanwhile, through the Japan Development Bank or the Export-Import Bank, the government often participates, along with the banks, in long-term lending to industry, and in effect guarantees many of the banks’ loans against default.(8)

Because the banks are so intimately tied to industry and because the government tends to back up industry’s loans, the Japanese banks can allow the manufacturers who are their creditors to finance themselves on the basis of debt (loans) rather than equity (stock) to a much greater extent than U.S. banks can allow their manufacturing creditors. Japanese manufacturers can therefore operate with ratios of debt to equity which would be considered too risky for American manufacturers. This has enabled Japanese enterprises to operate at lower rates of profit (on their total assets, loans plus stocks) than their U.S. counterparts, yet still accumulate capital at the same rate-or to operate at the same rate of profit, and accumulate capital more rapidly.

Another way of saying the same thing is that Japanese firms can operate at lower prices than can their U.S. competitors and make the same rate of profit on equity, or operate at the same prices, and make a higher rate of profit on equity.(9)

The great Japanese enterprises can not only rely on loans for financing to a greater extent than can their U.S.counterparts, they have been able to get those loans much more cheaply-at about two-thirds the rate of interest, over average, that U.S. manufacturing firms have had to pay during the 1970s and early 1980s.

This is partly because of their special relationship to the banks, in part because of government policy. But perhaps most important, it is because Japanese politicalfinancial institutions essentially deprive consumers of access to credit and thus oblige consumers to save in order to make large purchases, such as houses. The result is that consumers are not only prevented from competing with industry for credit (as they do, for example, in the U.S.), but also are induced to provide a huge mass of savings, increasing the supply (and thus reducing the cost) of loanable funds which the banks can recycle to industry.(10)

The organization of industry in giant horizontallyintegrated groups, each headed by a great bank, gives Japanese manufacturers a further edge. By virtue of the huge range of diversified holdings they contain, these keiretsu are able first of all to reduce their risk. Beyond that, the great Japanese horizontal groups enjoy a whole series of advantages over their U.S. competitors in adapting to changing economic conditions.(11)

In particular, simply by virtue of the size and superior financial resources of the keiretsu, Japanese enterprises can adopt a much longer run approach to their investments than their U.S. counterparts can afford. This often allows them to maintain their investments in new plant and equipment right through the downturns of the business cycle, when their U.S. competitors are being forced to cut back. They can also make greater in vestments in research and development. By 1983, civilian expenditures on research and development were 2.5 % of the GNP in Japan, in comparison to 1.8% in the U.S.(12)

In addition, Japan’s great, horizontally-integrated industrial groups facilitate the much faster movement of capital from unprofitable to profitable lines of production than is possible in the U.S. Those who are losing as a result of changing economic conditions (changing demand for goods, rise of new technologies) often also turn out to be winning as a result of those same changes, since “sunset” and “sunrise” industries often coexist in the same industrial group. Japanese enterprises can thus more easily cut their losses and allocate their funds where opportunities are better. In the U.S., in contrast, the owners of the older, decreasingly competitive industries often have little choice but to try to make them profitable for as long as possible.

For similar reasons, horizontal integration tends to facilitate government planning, especially by making it easier for the government to grant subsidies or tax breaks to firms carrying out accelerated technical change, rapid capital accumulation or large-scale research and development. This sort of “industrial policy” is difficult to implement in the U.S., since policies which favor one sort of firm or industry must be supported at the expense of others, giving rise to big political problems. In Japan, since the great horizontal groups tend to include both the favored and the discriminated against industries, that problem arises to a much lesser degree.

Thus, while the Japanese government does little direct investing in industry, it has been able, by its strategic use of direct loans as well as subsidies, tax breaks and the like, to help induce Japanese manufacturers to focus their efforts toward the massive development of large-scale mass production in the late 1950s and 1960s, toward the development of so called high-tech manufacturing in the 1970s (memory chips, etc.), and toward the development of science-based industry (biotechnology, new materials, etc.) in the 1980s.(13)

Finally, the Japanese government has stepped in directly where the market works very poorly or not at all. Perhaps most important in this respect, the Japanese state has been able to provide for a level of technical education far superior to that which the American state provides. For example, Japan is annually producing twice as many engineers per capita as does the United States.(14)

ii) The Costs of Hegemony. In addition to the foregoing economic and institutional disadvantages, the U.S. economy has suffered certain critical problems because industrial leadership has brought with it international political-economic hegemony.(15)

As the dominant industrial nation — with what was, for many years, the most efficient productive plant and the most powerful capitalist class — the United States naturally was obliged to provide the main international currency, the dollar. This offered certain real advantages, but it also had drawbacks with respect to the development of the productive forces in the U.S.

Because the dollar has been the main currency used for international transactions, it has tended to be overvalued-worth more than the purely productive power of U.S. industry would warrant. But an overvalued dollar has raised the price of U.S. goods for foreign purchasers and thus made those goods more difficult to ex port. Correlatively, an overvalued dollar has made foreign goods cheaper for American purchasers.

It has thus been both easier for the U.S. to import goods and simpler to export capital. The consequence has been to exacerbate America’s problems of balancing its payments and balancing its trade.

Furthermore, as the most powerful capitalist nation in political and military terms, the United States has been obliged to assume a disproportionate share of the costs of policing the world. This has meant that the United States has spent a greater proportion of its total output on arms than has any other capitalist country. Over the period 1960-1980, about 7.3% of the gross domestic product was spent on arms in the U.S., compared to about 4.5% in France, 3.9% in Germany, and only about 1% in Japan.(16)

Arms spending has thus constituted, in both relative and absolute terms, a huge unproductive drain on U.S. resources. Funds which would, in part, have gone to productive investments in new means of production and consumption goods have been siphoned off into waste, further eroding the potential for developing the productive forces and, ultimately, the competitive position of American industry.

It is exceedingly unlikely that the trend toward U.S. industrial decline will be reversed in the foreseeable future.

First of all, while the giant unproductive war industry constitutes an enormous drain on U.S. productive power, it nonetheless offers many of the greatest U.S. corporations the opportunity for giant assured profits. Here is an enormous area from which foreign competitors are excluded, since they are not allowed to bid on government contracts, and in which profits are virtually guaranteed by the state. We can hardly expect U.S. corporations to seek to restrict such a lucrative field for investment, merely because its maintenance and expansion has the effect of undermining U.S. manufacturing competitiveness.

At the same time, since the older, relatively backward industries naturally tend to be much larger and better entrenched than the newer more advanced industries, they naturally have a much better chance of exerting political influence. The leading U.S. corporations threatened by foreign competition have thus been increasingly successful in winning both protection against imports and direct government subsidies.

According to one calculation, government assistance to business in the form of tax preferences, loans, guarantees, research and development and the like amounted to an astonishing 13.9% of the U.S. gross national product.(17) Given the enormous clout of the older declining industries in the U.S., it is not really surprising that the policy of protecting and subsidizing U.S. corporations has had the effect, by and large, of allowing them to persist even longer than expected with their relatively backward equipment.

Perhaps even more crucial than military spending and government policy in preventing a break from the pattern of industrial decline has been the ability of American capitalists to profit from financial as opposed to manufacturing activity. Here returns remain high, especially since U.S. lenders and sellers of financial services increasingly operate on a world scale: they supply funds to the most profitable lines of production wherever they are located, and these of course-lie more and more outside the United States. Once again, the best profits are made from the very programs, policies, and activities which perpetuate industrial decay.

Even were the U.S. economy successfully to transform itself so as to operate more like that of Japan, it could not thereby assure itself of overcoming its competitive disadvantage. This is because the newly-industrializing countries of Southeast Asia — especially Korea and Taiwan — have not only adopted and perfected the Japanese institutional model, but on that basis have developed the capacity to combine many of the most advanced techniques with ultra-low wages.

This is in many ways an unprecedented development. In the past, those (generally Third World) regions which had the lowest wages usually lacked the skilled labor, the technical capacity, the infrastructure, and the capital required to adopt new technologies, and were thus consigned to producing the crudest, least profitable manufactured commodities (as well, of course, as raw materials). In postwar Taiwan and Korea, land reforms destroyed the old feudal classes, thereby establishing the basis for a productive agriculture, while freeing the state from any need to cater to the interests of old entrenched agrarian classes and enabling it to play a dynamic part in furthering the industrializing process. As in Japan, the banks play a huge role in these nations, backed up by the state, and the economies are dominated by huge horizontal conglomerates and/or government-owned industries which undertake most of the innovation and production for export.

In consequence, these economies have developed the capacity to adopt the latest technologies much more quickly than any other nations have ever done, and are combining these technologies with low-cost labor assured by viciously repressive governments. Within less than two decades, the newly-developing economies of Southeast Asia have succeeded in challenging U.S. and even Japanese producers in a wide range of industries, including shipbuilding, steelmaking, electronics manufacturing, construction contracting, and most recently automaking, not to mention textile, garment, and footware production.(18)

The spectacular rise of the so-called Asian Gang of Four (Taiwan, South Korea, Singapore, Hong Kong) has constituted a major source of discouragement to potential investment in American manufacturing and a growing pole of attraction to U.S. financiers, and is one critical reason why the relative position of U.S. industry has only deteriorated since the start of the crisis more than a decade ago.

Given the discouraging competition in international manufacturing and especially given their alternatives-to invest in arms, in finance, and of course in the industries of the U.S.’s competitors — U.S. capitalists would, under any circumstances, be unlikely to take the risk and pay the price of industrial regeneration. What makes such a transformation almost inconceivable in the foreseeable future is the long-term trend of deepening international crisis. While U.S. manufacturing has, for some time, been declining in relative terms, every national economy-including Japan’s and those of the Southeast Asian Gang of Four — has, since the onset of the international economic crisis, been doing worse than previously in absolute terms. A new, serious recession would be particularly disastrous for the export-dependent economies of Southeast Asia.

Given the long-term trend toward declining profits and toward increasingly worse cyclical downturns, prospects are fairly bleak for manufacturing investment for everyone. Under such conditions, U.S. capitalists would be tempting fate to undertake a gigantic program of renovation, requiring huge long-term placements of capital. There is, so far, simply no evidence that they in tend to risk this.

III. Economic Effects of Declining Competitiveness: American Industry from Boom To Crisis

The relative decline of American industry has taken place over the whole of the postwar period, through the period of boom and the subsequent crisis. Schematically speaking, the world economy may be seen to have gone through three phases in the postwar years. By briefly sketching this progression, it is possible to show how declining competitiveness both determined the specific impact of the world crisis on the American economy and shaped the character of the American political response to that crisis.

i) The Postwar Boom and the Export of Capital. For a significant period, through the 1950s and into the early 1960s, the different advanced economies developed rapidly, largely in separation from one another, on the basis of the growth of their domestic markets, largely avoiding competition with the United States. Japan in particular based most of its early postwar development on the rapid expansion of its home market.

Meanwhile, most symptomatic of the overall trend, huge sums of American investment went abroad. Throughout the greater part of the postwar period, U.S. investment abroad grew at the rather spectacular rate of 10% per annum, more than twice as fast as investment in the U.S. has grown. This is an incontrovertible sign that opportunities for profit abroad, especially in Europe where the bulk of the funds went, were significantly greater than those in the U.S.

By the early 1960s, the Europeans were complaining of the so-called “American Challenge,” the invasion of U.S. multinational corporations into the European economies. But this invasion was much more a manifestation of the excellent prospects for investment in Europe than it was of the weakness of European producers.

ii) International Competition and the Descent into Crisis. It did not take long, however, before a large measure of interdependency was restored, and the unprecedentedly rapid growth of international trade is one of the characteristic features of the postwar boom. But as international trade expanded, the problems of U.S. industrial competitiveness began to be exposed.

Especially in the period from about 1964-5, the United States suffered a sharp erosion in its international economic position. This was the period in which Japanese manufacturers, fueled by massive loans from the banks and encouraged by the state, were enormously increasing their investments in heavy industry and, on that basis, posing an initial challenge to what had hitherto been un contested U.S. supremacy in this field. By 1973, Japanese manufacturers had actually overtaken U.S. producers in productivity in such heavy industrial, mass production lines as steel, general machinery, electrical machinery, transport equipment, and precision machinery.(19)

The decline in U.S. competitiveness was manifested first of all in the decreasing U.S. share of world manufacturing exports, which fell from around 24 % to around 18 % in the short period from 1965 to 1973. In the same period, Japan’s share of world manufacturing exports increased from about 8%to about 14%. Above all, there was a huge invasion of products produced abroad into the U.S.: foreign-made steel, autos, machine tools, machinery, consumer electronics, and a wide range of other commodities quickly grabbed a significant share of the U.S. market.(20)

By the end of the 1960s, the U.S. was suffering serious problems in both its balance of payments (the result of the export of capital) and its balance of trade (the result of growing competition in exports and the rise of imports).

The sudden intensification of foreign competition-reflected in the accelerated export of U.S. capital, the rapid growth of imports, and the emerging imbalances of payments and of trade-apparently acted to trigger (it cannot be said to have caused) the international economic crisis, the first casualty of which was the U.S. dollar. As early 1968, there was a massive run on the dollar, threatening the whole international monetary system. In 1971, the U.S. had its first balance of trade deficit in the twentieth century.

In 1970 came the first recession, the first year of negative growth, following the unprecedentedly long boom of the early to late 1960s. Over the years 1971-1973, the dollar had to be devalued and the whole Bretton Woods international monetary structure of dollar convertibility and fixed exchange rates collapsed. Above all, precisely in this period, especially under the impact of the growing international competition and the resulting pressure to keep prices down, there was a precipitate decline in the overall rate of profit in the U.S. from which the economy has yet to recover.

The after-tax rate of return, adjusted for inflation, fell from about 9% in 1965 to about 3.5% in 1970 and 2% in 1974, and languished below 4% during the rest of the decade. Manufacturing was even harder hit, most likely because it was relatively more exposed to international competition than was the rest of the economy. The pretax rate of return on manufacturing assets, adjusted for inflation, fell from around 12 % in 1965 to about 4 % in 1970 and around 3% in 1975, recovering to about 7% in 1976, then falling steadily to hit 2 % in 1981.(21)

iii) The U.S. Counter-Offensive and the Internationalization of the Crisis. Ironically, the same forces which led to the onset of crisis in the U.S. initially helped to prolong prosperity worldwide, as U.S. imports of European and Japanese goods kept European and Japanese profits and economic growth up while those in the United States plummeted. But from 1971, with Nixon’s New Economic Policy, the U.S. government and U.S. employers initiated a counter-offensive against U.S. workers and foreign competitors, more or less consciously directed at restoring the American position.

From the early 1970s onwards, there was a sustained attack on workers’ wages, working conditions, and social services designed to cut costs of production and to redistribute income away from labor in the direction of capital. Over the period between 1972-3 and 1982-3, the spendable hourly earnings (wages minus taxes) of production workers fell by more than 20 % . Hourly wages (before taxes) fell by 10% in the same period. By 1981, workers’ spendable hourly earnings had fallen to what they had been in 1960; hourly wages were what they had been in the late 1960s.

In addition, from the early 1970s, employers launched a series of vicious speedup campaigns-G-MAD at General Motors, the Kokomo Plan in the post office, MTM (minutes times motion) in grocery warehouses, and many others across all industry. Beginning somewhat later, there were big cuts in government spending for the very poor. Meanwhile, continuing a trend begun even earlier, taxation of the corporations was drastically reduced. Back in the 1960s, corporate taxation contributed about a quarter of all federal revenues. By 1983, its contribution had dropped to 6.2 % with loopholes reducing revenues from taxation of the corporations (supposedly paying at the statutory rate of 46%) by $1.67 for every dollar actually collected.(22)

The attack on U.S. workers was accompanied by an at tack on foreign producers. Over the course of the 1970s, the dollar was devalued three times, cutting its value by about 17%. This amounted to a significant cheapening of U.S. goods on the world market, allowing foreign purchasers to buy significantly more U.S. products with their more valuable currencies. The heavy devaluation also, of course, constituted a further attack on U.S. workers, for by forcing up the price of foreign products, it allowed them to buy fewer goods with their wage dollars.

Meanwhile, throughout the 1970s and continuing into the present, there has been a progressive increase in the protection of U.S. manufactures from foreign imports, a creeping protectionism. Today, there are major barriers (formal or “voluntary”) against foreign imports of steel, auto, textiles, consumer electronics and many other goods.

A11 these responses by U.S. corporations and the U.S. government to increasing international competition did help to counteract the forces making for the decline in the competitiveness of U.S. industry. But the long run outcome was less to improve the relative position of U.S. manufacturing than to undermine the entire international economy.

Declining demand from the U.S.-resulting from the attack on wages and social spending, dollar devaluation, and rising protectionism -helped to restrict the growth of world trade, and, in particular, the growth of Japanese and European exports. World trade had grown at an annual average rate of 8.7% per annum in the boom period of 1963-1973, but, between 1973 and 1981, the figure fell by more than half to 3.5% per annum.(23)

As the U.S. market ceased to pull along the world economy, the European and Japanese economies, dependent as they were on exports for really rapid growth, also began to feel the effects of over-accumulation and intensified competition. In 1974-5, there was the first, deep coordinated international recession, and this was repeated in 1979-1982.

The internationalization of the crisis during the 1970s did not, however, decisively reverse the process of relative decline in U.S. industrial competitiveness because it did not decisively increase the relative attractiveness of American manufacturing as a field for investment. During this period, European manufacturing was in fact badly hurt by the crisis, and may have lost some of its attractiveness; but any gain in competitiveness the U.S. may have experienced against Europe was more than offset by its loss with respect to the Third World (as well as Japan).

Third World industrializers now emerged as serious competitors on the world market. In part, industrial investment took place in the Third World merely to take advantage of extremely cheap labor, as in much of Latin America. But in Southeast Asia, as already noted, Japanese-style institutional arrangements offered much greater and longer-lasting advantages. Over the course of the crisis-torn 70s, Korea and Taiwan were actually able to increase the proportion of their national output that they devoted to investment and on this basis were able to maintain truly extraordinary annual rates of growth of manufacturing, which quintupled those in the U.S. for the entire period between 1960 and the early 1980s. By 1980 the Southeast Asian economies collectively surpassed any of the great European nations as exporters into the United States.

In light of the excellent investment opportunities in Southeast Asia and (to a lesser extent) in Latin America, it is understandable that one of the most spectacular new developments of the 1970s was massive flow of capital from the United States to the newly developing countries in the form of loans, as U.S. (and European) banks provided hundreds of billions of dollars to finance the growth of the merging competitors in world manufacturing. By the end of 1984, private banks held over 600 billion dollars in Third World debts.(24)

Naturally, U.S. industries are not simply collapsing overnight. Nor does the general trend toward decline totally lack exceptions. In such lines of manufacture as aircraft and office equipment, U.S. producers long ago secured dominant positions and they continue to maintain them, if not without challenge. Even in the auto industry, the competitive struggle is not over. General Motors is investing billions of dollars in the modernization of its plants, notably in its highly-experimental Saturn project, which is aiming to produce cars more cheaply than do the Japanese.

Nevertheless, there are in fact very few manufacturing lines like aircraft and office supply where the competitiveness of U.S. producers seems to be holding up, and which can therefore easily attract investment funds on the free market. Nor are there very many manufacturing companies with the massive internal sources of funds available to GM. In fact, since the start of the world crisis, Japanese manufacturers have taken advantage of their special institutional arrangements to consolidate their position in the US. auto market and to pose a powerful challenge in the so-called high-tech industries where the United States previously reigned supreme.

For the time being at least, U.S. companies have given up producing small cars in the U.S. and are largely relying on arrangements with overseas subsidiaries or partners in Japan or Korea. This response is perhaps to be expected in view of the fact that Japanese producers can make a small car for an estimated $2,000 less than can the U.S. companies, but is likely to have disastrous results.

By 1988, according to Commerce Department estimates, 17% of the cars sold by Detroit will be produced by the likes of Toyota, Nissan, and Honda. That will mean that imports will control 40% of the U.S. market, even if protection continues, and that another 90,000 jobs in auto will be lost. Meanwhile, U.S. auto producers also are relying increasingly on overseas suppliers of parts. Taking all parts into consideration, 50% of all cars sold in the U.S. already are produced abroad. At the new Toyotta-GM joint venture in California, which does mostly final assembly, 70% of all production in each auto is done abroad.

It is hardly surprising that each of the big three U.S. auto companies, recognizing the relatively greater opportunities in finance, has very recently established big new units specializing in the full range of financial services (not just auto credit, as in the past).(25)

Meanwhile, over the last five years or so, U.S. high technology manufacturing has experienced a truly dramatic decline in its position on the world market. This is largely the result of the Japanese ability to keep investments up through each downturn, when the far smaller U.S. high technology companies have been forced to cut way back, as well as the Japanese government’s success in forging cooperative arrangements among the big Japanese producers in high technology research and development. In the field of semiconductors, Japan is today actually investing in ab solute terms as much as is the U.S.

Over the past five years, in every major electronics market-computing equipment, instruments, communication equipment, office machines, semiconductors and components, and consumer electronics-imports have risen and exports have fallen, with the overall trade balance (exports minus imports) falling from a surplus of close to eight billion dollars in 1980 to a deficit of around seven billion dollars in 1984.

The entire U.S. market in the high technology (now mass production) lines of videocassette recorders and compact disks is controlled from abroad; not one of these products is made in the U.S. Here again, the trend is for the U.S. producers to switch rather than fight, to give up production in the U.S., and either to relocate overseas or simply to import Japanese and Korean products and market them under their own label.

For example, by 1984, G.E. was having virtually all of its consumer electronics products made in Asia, importing $1.4 billion worth of goods to be sold under the G.E. label. Meanwhile, it does not augur well for overall manufacturing in the U.S. that by 1983, Japan had 30,000 robots in operation, as compared to 10,000 in the U.S.-that is, eight times as many per employed worker.(26)

Now it has been argued that despite appearances, the decline of U.S. manufacturing competitiveness reflects no long-term structural problem, but merely the recent rise in the value of the dollar, which grew by some 50% in the period from 1980 to early 1985. But this is wishful thinking. In the first place, the relatively low rate of inflation of the U.S. in this period-the relatively faster growth of prices abroad-substantially counteracted the rising value of the dollar, reducing the effective increase in the dollar’s value by half to only 25%. Even more directly to the point, the dollar’s value simply did not grow that much in relation to the currencies of those nations which are posing the biggest competitive threat.

For example, between the end of 1979 and the middle of 1985, the U.S. trade deficit with Japan quadrupled, but the exchange value of the dollar against the yen increased by only 3.8%. Similarly, Taiwan, Korea, Singapore, and Hong Kong all have more or less pegged their currencies to the dollar, so, even lowering the value of the dollar would not improve the U.S. competitive position with those countries.(27)

A11 evidence therefore points to a continuation, indeed a worsening, of the decline in relative productiveness across U.S. industry and of the declining attractiveness of U.S. manufacturing as a field for investment. Most telling, the crisis of investment has intensified. Since the start of the crisis, the U.S. has seen the proportion of its GNP that it invests in fixed capital actually fall compared to the proportion Japan invests. The U.S. level was about half that of Japan during the boom; it’s been about one-third since 1970.

There has, of course, in formal terms, been a truly gigantic influx of investment funds from abroad into the U.S. But this is not, despite assertions to the contrary, a sign that foreigners believe that prospects are good in U.S. industry, and are therefore investing. Probably 90 % of the foreign investment in the U.S. has been in government bonds, to cover the enormous federal deficit (at high rates of interest). Much of the rest is aimed at getting around U.S. protection, reflecting the fact, or the fear by foreign companies, that rising import restrictions will prevent them from exporting their goods here. Even in this case, the newly-opened foreign-owned outlets are often largely assembly operations, with a large proportion of their parts being brought from abroad-as in auto or certain high-technology plants.(28)

It should not, therefore, be at all surprising that the U.S.’s ability to increase its productivity has fallen even further behind that of its main competitors. Over the period 1977-1985, manufacturing productivity grew at the negligible rate of 0.7% per annum in the U.S., compared to 1.8% in Western Europe and 3.4% in Japan.

Once again the bottom line: profitability in U.S. manufacturing remains in crisis. As the recent report of the President’s Commission on Industrial Competitiveness put it: “American’s industrial base has been unable to produce the kind of financial returns that attract productive investments.” “In the 1960s, the real rates of return earned by manufacturing assets were substantially above those available on financial assets. Today the situation is reversed.” “Over the past twenty years, real rates of return on manufacturing assets have declined. Pretax returns are well below alternative financial investments and make many investors question the wisdom of putting funds in America’s vital manufacturing sector.”(29)

It is today often argued that the decline of U.S. manufacturing reflects an epochal transition from manufacturing to service industries, analogous to that from agriculture to manufacturing, which actually signals an historic advance of the productive forces and a general increase of higher income employment. The U.S. economy is supposed to be shifting toward high-value, highly-skilled, and high-technology service work: the U.S. will provide the computer software, the new techniques, and the industrial design for the world’s manufacturing and reap the benefits from its high-value output in terms of higher wages and generally higher living standards.

Nevertheless, this viewpoint is highly misleading. Above all, very few of the large number of new service sector jobs will be in high technology. According to a U.S. Bureau of Labor Statistics report, the ten job categories which can be expected to grow the most in the next decade will be, for the most part, low-paying and almost entirely outside high technology. Those jobs are, in order of expected amount of growth: cashiers; registered nurses; janitors and cleaners; truck drivers; waiters and waitresses; wholesale trade sales workers; nursing aids, orderlies and attendants; retail salespersons; accountants and auditors; and kindergarten and elementary school teachers. On the other hand, high technology industries, although fast-growing in relative terms, can be expected to generate at most one million jobs over the next decade, i.e. less than half the number of jobs lost in manufacturing over the period 1980-1983.(30)

The shift to services is, in fact, highly problematic. First, as just noted, most of the “production” in the service sector is, and will continue to be, in low-technology, low-skilled, low-waged lines. Second, service industries, historically and in the foreseeable future, do not experience productivity increase as rapidly as does manufacturing; a shift to services therefore means a slowdown in productivity increase for the entire economy. Relatedly, and more importantly, the shift to services will almost certainly bring slower technical progress. The greatest proportion of technical development takes place not in some laboratory, but through the processes of learning and discovery which occur in and around the process of production itself. For example, a huge part of Japan’s recent progress in so-called hightechnology professional electronics has emerged directly out of its experience in manufacturing consumer electronics products. To the extent, therefore, that the U.S. cedes manufacturing production to its leading competitors, it is likely to lose its capacity for technical in&novation, as well as for providing those high-skilled services (e.g. software, manufacturing design) that manufacturing requires.

Finally, today’s service industries do not, by and large, yield products which can be sold on the world market. So the shift to services is likely to further undermine the place of the U.S. in international trade, reducing the ability of the U.S. economy to take advantage of the world division of labor.(31)

In sum, the kind of shift from manufacturing to services that is occurring today is likely to intensify the trend toward declining productiveness and to reduce U.S. wealth and living standards. As the trend toward manufacturing decline continues, manufacturing workers will inevitably be subject-as they have been for more than a decade-to declining wages and working conditions, or lose their jobs and be forced to take jobs in the (relatively) growing service sector.

Over the long period between 1970 and 1984, 23.3 million people were added to the nonagricultural workforce, but only 1 % of these entered manufacturing. Meanwhile, according to a recent Congressional study, 11.5 million workers lost jobs because of plant shutdowns or relocations from 1979 to 1984, but only 60% of those got new jobs in that period. Those who found new jobs (as they almost inevitably had to do) in the service industries had to take significant pay cuts, because wages in the service industries are, over average, some 20% lower than in manufacturing.

Ironically, perhaps, the best prospects of manufacturing expansion today are to be found in border industries and in the re-emerging sweatshops of the cities, where employers can take advantage of the ultra-cheap labor of undocumented and unprotected immigrant workers. This is a far cry from the utopian vision of today’s theorists of “post-industrial society.” But it is entirely in keeping with the overall trend toward U.S. industrial decline.(32)

Notes

- A full account of the causes of the world crisis, which underlies the decline of the U.S. economy is beyond the scope of this essay.

back to text - The Report of the President’s Commission on Industrial Competitiveness, Global Competition. the New Reality (1985). p. 25; Riccardo Parboni, The Dollar and its RivaLs (1981), p. 93.

back to text - Data Resources, Inc., The ORI Report on U.S. Manufacturing Industries (1984), p. 56. Global Competition. the New Reality, p. 9.

back to text - Donald F. Barnett and Louis Schorsch, Steel, Upheaval in a Basic Industry (1983), p. 119 (steel); Ira C. Magaziner and Robert Reich, Minding America’s Business (1982), p. 113 (tv sets); S. Greenhouse, “A Survival Fight in Machine Tools,” New York Times (Henceforth NYT), 8 July 1984 (machine tools); Alan Altshuler et al, The Future of the Automobile. The Report of MITs International Automobile (1984), p. 160 (cars). See also James C. Abegglen and Stalk, Kaisha: Japanese Corporation (1985), pp. 62-65; Bruce R. Scott, “Competitiveness: Concepts, Performance, and Implications,” in U.5. Competitiveness in the World Economy, ed. Bruce R. Scott and George C. Lodge (1985), p. 65.

back to text - D.E. Sanger, “Prospects Appear Bleak for U.S. Chip Makers,” Los Angeles Times (henceforth LAT), 29 October 1985; “Superchips: The New Frontier,” Business Week (henceforth BW), 10 June 1985.

back to text - W.J. Broad, ‘Big Japanese Gain in Computers Seen” NYT, 13 February 1984; H.M. Schmeck, “Report Says Japan Could Lead in Commercial Biotechnology,” NYT, 27 January 1984.

back to text - The DR Report, pp. 1, 5.

back to text - Barnett and Schorsch, Steel, pp. 28, 53-56.

back to text - Y. Miyazaki, “Excessive Competition and the Formation of Keiretsu,” in Industry and Business in Japan, ed. K. Sato (1980); E. Sakakibara, The Janese Financial System in Comparative Perspective (Joint Economic Committee, U.S. Congress, 1982), esp. pp. 26, 54.

back to text - J.C. Abegglen and W.V. Rapp, “Japanese Managerial Behavior and ‘Excessive Competition,’ ” The Developing Econonties, VIII (December 1970), pp. 427-430.

back to text - Sakakibara, Japanese Financial System, pp. 22, 53. Scott, “U.S. Competitiveness,” p. 64.

back to text - l. Nakatani, “The Economic Role of Financial Corporate Grouping,” in The Economic Analysis of the Japanese Firm, ed. M. Aoki (1984), esp. 227, 245.

back to text - Global Competition, p. 22.

back to text - See Abegglen and Stalk, Kaisha, passim.

back to text - Global Competition, p. 21.

back to text - For a very good account of the implications of U.S. hegemony for U.S. economic decline, see Joshua Cohen and Joel Rogers, 011 Democracy (1982).

back to text - R.W. DeGrasse, Military Expansion and Economic Decline (1983), p. 61.

back to text - A. Pine, “Debate Heats Up Again on Industrial Policy,” Wall Street Journal (henceforth WSI) 10 October 1982.

back to text - See, eg., “The Koreans are Coming,” BW, 10 October 1982.

back to text - Scott, “U.S. Competitiveness,” p. 65.

back to text - Scott, “U.S. Competitiveness,” p. 27. Cf. Magaziner and Reich, Minding Arnerica’s Business.

back to text - Scott, “U.S. Competitiveness,” p. 30; Global Competition, p. 12.

back to text - Samuel Bowles et al, Beyond the Wasteland (1983), p. 25. R.S. McIntyre and D.C. Tipps, “Exploring the Investment-incentive Myth,” Challenge (May-June 1985), p. 47.

back to text - Philip Armstrong et al, Capitalism Since World War Il (1984).

back to text - Scott, “U.S. Competitiveness,” pp. 52, 55.

back to text - K. Dreyfach & 0. Port, “Even American Know-How Is Headed Abroad,” BW, 3 March 1986; W.J. Hampton, “Can Detroit Cope This Time?” BW, 22 April 1985; “Chrysler Will Acquire Consumer Credit Unit From BankAmerica,” LAT 9 October 1985; R.W. Bennett, “Expanded Scope for G.M.A.C.,” NYT, 6 August 1985; J. Holusha, “The Disappearing ‘U.S. Car,'” NYT l0August 1985; 0.0. Buss & Paul Ingrassia, “While Trying to Curb imports, Auto Makers Set More Foreign Ties,” WSJ, 28 October 1985.

back to text - “Japan’s Strategy for the ’80s,” BW, 14 December 1981, pp. 6lff.; “Chip Wars,” BW, 23 May 1983; Abegglen, Kaisha, pp. 138-139; J.W. Wilson, “America’s High Tech Crisis,” BW, 11 March 1985; Dreyfach & Port, “Even American Know How.”

back to text - For the explanation of U.S. manufacturing decline in terms of the rise of the dollar’s value, see Robert Z. Lawrence, Can America Compete? (1984). For the data in the text, see G. Shilling, “Trade Blues Aren’t Just a Matter of Green,” WSJ, 11 July 1985; M. Karczmar, “A Weaker Dollar Won’t Slow Imports,” NYT, 20 October 1985.

back to text - B.M. Friedman, “Saving, Investment, and Government Deficits in the 1980s,” in U.S. Competitiveness in the World Economy, p. 400; P.T. Kilborn, “Japan Investing Enormous Sums of Cash Abroad,” NYT, 11 March 1985.

back to text - Shilling, ‘Trade Blues,” Global Competition, p. 12.)

back to text - J. Burger, “The False Paradise of a Service Economy,” BW, 3 March 1986; “America Rushes to High Tech for Growth,” BW, 28 March 1983.

back to text - See especially “Japan’s Strategy for the ’80’s,” BW, 14 December 1981, pp. 53ff.

back to text - K.B. Noble, “Study Finds 60 Percent of 11 Million Who Lost Jobs Got New Ones,” NYT 7 January 1986.

back to text

March-April 1986, ATC 2